Exam 18: Portfolio Performance Evaluation

Exam 1: Investments: Background and Issues75 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets90 Questions

Exam 4: Mutual Funds and Other Investment Companies85 Questions

Exam 5: Risk and Return: Past and Prologue83 Questions

Exam 6: Efficient Diversification84 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory85 Questions

Exam 8: The Efficient Market Hypothesis86 Questions

Exam 9: Behavioral Finance and Technical Analysis87 Questions

Exam 10: Bond Prices and Yields93 Questions

Exam 11: Managing Bond Portfolios85 Questions

Exam 12: Macroeconomic and Industry Analysis89 Questions

Exam 13: Equity Valuation88 Questions

Exam 14: Financial Statement Analysis84 Questions

Exam 15: Options Markets88 Questions

Exam 16: Option Valuation85 Questions

Exam 17: Futures Markets and Risk Management87 Questions

Exam 18: Portfolio Performance Evaluation87 Questions

Exam 19: Globalization and International Investing70 Questions

Exam 20: Hedge Funds60 Questions

Exam 21: Taxes,inflation,and Investment Strategy73 Questions

Exam 22: Investors and the Investment Process81 Questions

Select questions type

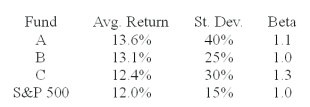

The average returns, standard deviations and betas for three funds are given below along with data for the S&P 500 index. The risk free return during the sample period is 6%.  -You wish to evaluate the three mutual funds using the Sharpe measure for performance evaluation.The fund with the highest Sharpe measure of performance is __________.

-You wish to evaluate the three mutual funds using the Sharpe measure for performance evaluation.The fund with the highest Sharpe measure of performance is __________.

(Multiple Choice)

4.9/5  (36)

(36)

Suppose that over the same time period two portfolios have the same average return and the same standard deviation of return,but portfolio A has a higher beta than portfolio B. According to the Sharpe measure, the performance of portfolio A __________.

(Multiple Choice)

4.8/5 (29)

A portfolio generates an annual return of 17%,a beta of 1.2 and a standard deviation of 19%.The market index return is 12% and has a standard deviation of 16%.What is the M2 measure of the portfolio if the risk free rate is 4%?

(Multiple Choice)

5.0/5 (40)

A fund has excess performance of 1.5%.In looking at the fund's investment breakdown you see that the fund overweighed equities relative to the benchmark and the average return on the fund's equity portfolio was slightly lower than the equity benchmark return.The excess performance for this fund is probably due to _______________.

(Multiple Choice)

4.7/5 (34)

Morningstar's RAR produce results which are similar but not identical to ________.

(Multiple Choice)

4.8/5 (34)

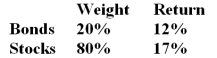

In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the following investments in asset classes:  The return on a bogey portfolio was 12% calculated as follows:

The return on a bogey portfolio was 12% calculated as follows:  -The total excess return on the managed portfolio was __________.

-The total excess return on the managed portfolio was __________.

(Multiple Choice)

4.9/5 (32)

Consider the Sharpe and Treynor performance measures.When a pension fund is large and well diversified in total and it has many managers,the __________ measure is better for evaluating individual managers while the __________ measure is better for evaluating the manager of a small fund with only one manager responsible for all investments that may not be fully diversified.

(Multiple Choice)

4.8/5 (37)

Which one of the following performance measures is the Sharpe measure?

(Multiple Choice)

4.8/5 (33)

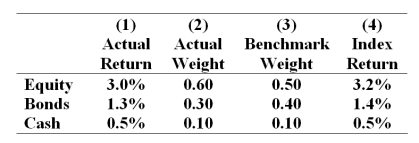

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3), and the returns of sector indexes in column 4.  -What was the manager's return in the month?

-What was the manager's return in the month?

(Multiple Choice)

4.9/5 (46)

Henriksson found that,on average,betas of funds __________ during market advances.

(Multiple Choice)

4.8/5 (38)

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3), and the returns of sector indexes in column 4.

-What is the contribution of security selection to relative performance?

(Multiple Choice)

4.8/5 (43)

If all ___ are ___ in the Treynor-Black model,there would be no reason to depart from the passive portfolio.

(Multiple Choice)

4.9/5 (30)

The Treynor-Black model combines an actively managed portfolio with an efficiently diversified portfolio in order to _______________________.

I.improve the diversification of the overall portfolio

II.improve the overall portfolio's Sharpe ratio

III.reach a higher CAL than otherwise would be possible

(Multiple Choice)

4.8/5 (49)

A mutual fund invests in large-capitalization stocks.Its performance should be measured against which one of the following?

(Multiple Choice)

5.0/5 (24)

Recent analysis indicates that the style of investing is a critical component of fund performance.In fact on average about _____ of fund performance is attributable to the asset allocation decision.

(Multiple Choice)

4.9/5 (32)

The table presents the actual return of each sector of the manager's portfolio in column (1), the fraction of the portfolio allocated to each sector in column (2), the benchmark or neutral sector allocations in column (3), and the returns of sector indexes in column 4.

-What was the bogey's return in the month?

(Multiple Choice)

4.8/5 (44)

The market timing form of active portfolio management relies on __________ forecasting and the security selection form of active portfolio management relies on __________ forecasting.

(Multiple Choice)

4.8/5 (30)

In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the following investments in asset classes: The return on a bogey portfolio was 12% calculated as follows:

-The contribution of security selection within asset classes to the total excess return was __________.

(Multiple Choice)

4.7/5 (33)

In a particular year, Salmon Arm Mutual Fund earned a return of 16% by making the following investments in asset classes: The return on a bogey portfolio was 12% calculated as follows:

-The contribution of asset allocation across markets to the total excess return was __________.

(Multiple Choice)

4.9/5 (39)

A portfolio generates an annual return of 13%,a beta of 0.7 and a standard deviation of 17%.The market index return is 14% and has a standard deviation of 21%.What is the Treynor measure of the portfolio if the risk free rate is 5%?

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)