Exam 22: Accounting Corrections and Error Analysis

Exam 1: The Financial Reporting Environment63 Questions

Exam 2: Financial Reporting Theory178 Questions

Exam 3: Judgment and Applied Financial Accounting Research127 Questions

Exam 4: Review of the Accounting Cycle154 Questions

Exam 5: Statements of Net Income and Comprehensive Net Income125 Questions

Exam 6: Statements of Financial Position and Cash Flows and the Annual Report158 Questions

Exam 7: Accounting and the Time Value of Money120 Questions

Exam 8: Revenue Recognition159 Questions

Exam 9: OL: Revenue Recognition110 Questions

Exam 10: Short-Term Operating Assets: Cash and Receivables125 Questions

Exam 11: Short-Term Operating Assets: Inventory134 Questions

Exam 12: Long-Term Operating Assets: Acquisition, cost Allocation, and Derecognition156 Questions

Exam 13: Long-Term Operating Assets: Departures From Historical Cost126 Questions

Exam 14: Operating Liabilities and Contingencies95 Questions

Exam 15: OL: Operating Liabilities and Contingencies12 Questions

Exam 16: Financing Liabilities167 Questions

Exam 17: Accounting for Stockholders Equity114 Questions

Exam 18: Investing Assets189 Questions

Exam 19: Accounting for Income Taxes121 Questions

Exam 20: Accounting for Employee Compensation and Benefits106 Questions

Exam 21: Earnings Per Share99 Questions

Exam 22: Accounting Corrections and Error Analysis394 Questions

Select questions type

Under the indirect method,which of the following would be subtracted from net income when determining net cash flows from operations?

A)gain on the sale or a used truck

B)amortization expense

C)decrease in prepaid rent

D)increase in salaries payable

(Essay)

4.8/5  (38)

(38)

Make the journal entry to correct the errors using the proper date.

(Not Answered)

This question doesn't have any answer yet

Which one of the following would not be a required disclosure for a change in accounting principle?

(Multiple Choice)

4.8/5 (39)

Compare and contrast the differences between accounting for leases under GAAP and IFRS.

(True/False)

4.8/5 (32)

At the end of 2015,the payroll supervisor for Claro,Inc.failed to accrue $24,790 in commissions for the outside salespersons.The cost was recorded in 2016 when the commissions were paid and Commissions Expenses was debited and Cash credited for the full amount.The error was not discovered until late in 2016 while reconciling year-end expenses for 2016.What is the proper treatment to correct the error? (Ignore income taxes.)

(Multiple Choice)

4.9/5 (42)

Initial direct costs are expensed at the inception of the lease in ________.

A)an operating lease

B)a direct financing lease

C)a sales-type lease

D)a capital lease

(Essay)

4.8/5 (38)

Companies account for guaranteed residual values in the same way they account for bargain purchase options.

(True/False)

4.9/5 (33)

An increase in a deferred tax liability is deducted from the accrual-basis tax expense to arrive at cash paid for income taxes.

(True/False)

4.9/5 (35)

Both U.S.GAAP and IFRS require a reconciliation of net income to net cash provided by operations.

(True/False)

4.8/5 (36)

The "bottom line" of the cash flow statement is Net Increase (Decrease)in Cash and Cash Equivalents.

(True/False)

4.9/5 (41)

Refer to Superbyte Corporation.

What is the net book value of the lease liability in Laguna Madre's balance sheet on June 30 of the current year?

A)$13,222,518

B)$13,883,146

C)$14,900,749

D)$14,301,177

(Essay)

4.8/5 (34)

When a large corporation purchases a new business which is included in consolidated statements for the year,it is not a change in a reporting entity,and it is handled prospectively.

(True/False)

4.9/5 (40)

What types of accounts are typically affected by investing cash flows?

(True/False)

4.9/5 (44)

The three classifications of cash flows are reporting,investing,and financing.

(True/False)

4.9/5 (35)

Changes in non-current liabilities relate to financing activities.

(True/False)

4.9/5 (36)

Swanson Corporation is leasing a machine from Gray,Inc.Swanson's incremental borrowing rate is 13%.The prime rate of interest is currently 7%.Gray's implicit rate in the lease is 9%; Swanson does not know this rate.At what interest rate should the minimum lease payments be computed?

(Multiple Choice)

4.8/5 (32)

Highland Corporation has always used declining-balance depreciation for its equipment.Beginning in 2016,the company has decided to use straight-line depreciation for all new equipment purchases.How should the company report this decision? Describe any journal entries and disclosures that need to be made for this change.

(Essay)

4.8/5 (40)

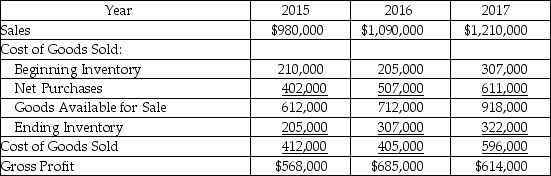

Vieta,Inc.'s CFO discovered a program error in its inventory program in early 2018,when she was making year-end adjustments to the financial statements for 2017.The errors began in 2015.Below is a summary of the sales and cost of goods sold on income statement items for the three years:

Upon further analysis,the CFO determined that each of the years had ending inventory errors.The correct amounts for the years were: 2015,$231,000; 2016,$350,000; and 2017,$474,000.The amounts for 2015 beginning inventory and all purchases are correct as stated.

Required:

Upon further analysis,the CFO determined that each of the years had ending inventory errors.The correct amounts for the years were: 2015,$231,000; 2016,$350,000; and 2017,$474,000.The amounts for 2015 beginning inventory and all purchases are correct as stated.

Required:

(Not Answered)

This question doesn't have any answer yet

Retrospective changes require all but which of the following?

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)