Exam 2: A Review of the Accounting Cycle

Exam 1: Financial Reporting89 Questions

Exam 2: A Review of the Accounting Cycle100 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements74 Questions

Exam 4: The Income Statement86 Questions

Exam 5: Statement of Cash Flows and Articulation83 Questions

Exam 6: Earnings Management47 Questions

Exam 7: The Revenuereceivablescash Cycle87 Questions

Exam 8: Revenue Recognition89 Questions

Exam 9: Inventory and Cost of Goods Sold134 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing111 Questions

Exam 13: Equity Financing97 Questions

Exam 14: Investments in Debt and Equity Securities88 Questions

Exam 15: Leases83 Questions

Exam 16: Income Taxes87 Questions

Exam 17: Employee Compensation-Payroll,pensions, Other Compissues83 Questions

Exam 18: Earnings Per Share86 Questions

Exam 19: Derivatives, contingencies, business Segments, and Interim Reports82 Questions

Exam 20: Accounting Changes and Error Corrections86 Questions

Exam 21: Statement of Cash Flows Revisited68 Questions

Exam 22: Accounting in a Global Market62 Questions

Exam 23: Analysis of Financial Statements65 Questions

Select questions type

For a given year,beginning and ending total liabilities were $8,400 and $10,000,respectively.At year-end,owners' equity was $26,000 and total assets were $2,000 larger than at the beginning of the year.If new capital stock issued exceeded dividends by $2,400,net income (loss)for the year was apparently

(Multiple Choice)

4.8/5  (34)

(34)

The following balances have been excerpted from Edwards' balance sheets:

Edwards Company paid or collected during 2013 the following items:

Edwards Company paid or collected during 2013 the following items:

The insurance expense on the income statement for 2013 was

The insurance expense on the income statement for 2013 was

(Multiple Choice)

4.9/5 (38)

On June 30,a company paid $3,600 for insurance premiums for the current year and debited the amount to Prepaid Insurance.At December 31,the bookkeeper forgot to record the amount expired.The omission has the following effect on the financial statements prepared December 31:

(Multiple Choice)

4.7/5 (42)

On August 1,a company received cash of $9,324 for one year's rent in advance and recorded the transaction on that day as a credit to rent revenue.The December 31 adjusting entry would include

(Multiple Choice)

4.9/5 (40)

On September 1,2012,Star Corp.issued a note payable to Federal Bank in the amount of $450,000.The note had an interest rate of 12 percent and called for three equal annual principal payments of $150,000.The first payment for interest and principal was made on September 1,2013.At December 31,2013,Star should record accrued interest payable of

(Multiple Choice)

4.8/5 (37)

How would proceeds received in advance from the sale of nonrefundable tickets for the Super Bowl be reported in the seller's financial statements published before the Super Bowl?

(Multiple Choice)

4.9/5 (46)

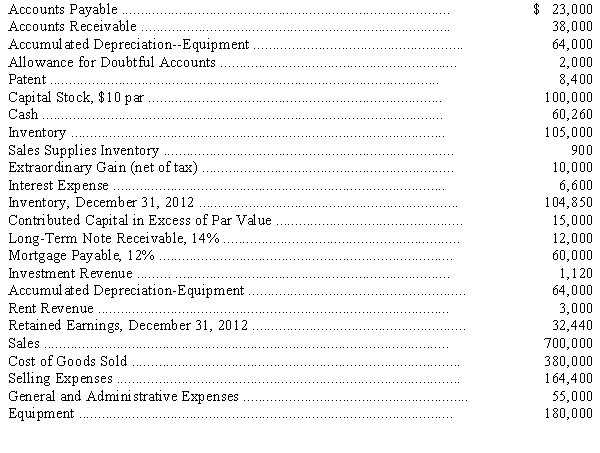

Account balances taken from the ledger of Owens Company on December 31,2013,are as follows:

Adjustments on December 31,2013,are required as follows:

(a)Estimated bad debt loss rate is 1/4 percent of credit sales.Credit sales for the year amounted to $200,000.Classify bad debt expense as a selling expense.

(b)Interest on the long-term note receivable was last collected August 31,2013.

(c)Estimated life of the equipment is 10 years,with a residual value of $20,000.Allocate 10 percent of depreciation expense to general and administrative expense and the remainder to selling expenses.Use straight-line depreciation.

(d)Estimated economic life of the patent is 14 years (from January 1,2013)with no residual value.Straight-line amortization is used.Depreciation expense is classified as selling expense.

(e)Interest on the mortgage payable was last paid on November 30,2013.

(f)On June 1,2013,the company rented some office space to a tenant for one year and collected $3,000 rent in advance for the year; the entire amount was credited to rent revenue on this date.

(g)On December 31,2013,the company received a statement for calendar year 2013 property taxes amounting to $1,300.The payment is due February 15,2014.Assume that the payment will be made on February 15,2014,and classify expense as selling expense.

(h)Sales supplies on hand at December 31,2013,amounted to $300; classify as selling expense.

(i)Assume an average income tax rate of 40 percent corporate tax rate on all items including the extraordinary gain..

(1)Prepare an eight-column work sheet.

(2)Prepare adjusting and closing entries.

Adjustments on December 31,2013,are required as follows:

(a)Estimated bad debt loss rate is 1/4 percent of credit sales.Credit sales for the year amounted to $200,000.Classify bad debt expense as a selling expense.

(b)Interest on the long-term note receivable was last collected August 31,2013.

(c)Estimated life of the equipment is 10 years,with a residual value of $20,000.Allocate 10 percent of depreciation expense to general and administrative expense and the remainder to selling expenses.Use straight-line depreciation.

(d)Estimated economic life of the patent is 14 years (from January 1,2013)with no residual value.Straight-line amortization is used.Depreciation expense is classified as selling expense.

(e)Interest on the mortgage payable was last paid on November 30,2013.

(f)On June 1,2013,the company rented some office space to a tenant for one year and collected $3,000 rent in advance for the year; the entire amount was credited to rent revenue on this date.

(g)On December 31,2013,the company received a statement for calendar year 2013 property taxes amounting to $1,300.The payment is due February 15,2014.Assume that the payment will be made on February 15,2014,and classify expense as selling expense.

(h)Sales supplies on hand at December 31,2013,amounted to $300; classify as selling expense.

(i)Assume an average income tax rate of 40 percent corporate tax rate on all items including the extraordinary gain..

(1)Prepare an eight-column work sheet.

(2)Prepare adjusting and closing entries.

(Essay)

5.0/5 (36)

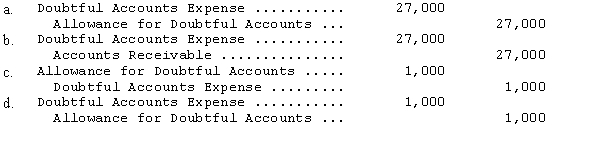

Scott Co.reported an allowance for doubtful accounts of $28,000 (credit)at December 31,2013,before performing an aging of accounts receivable.As a result of the aging,Scott determined that an estimated $27,000 of the December 31,2013,accounts receivable would prove uncollectible.The adjusting entry required at December 31,2013,would be

(Short Answer)

4.9/5 (42)

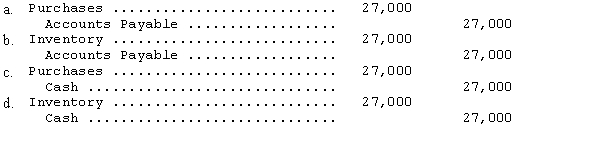

Iowa Cattle Company uses a periodic inventory system.Iowa purchased cattle from Big D Ranch at a cost of $27,000 on credit.The entry to record the receipt of the cattle would be

(Short Answer)

5.0/5 (38)

Failure to record depreciation expense at the end of an accounting period results in

(Multiple Choice)

4.9/5 (35)

At the end of the current fiscal year,an analysis of the payroll records of Bev Company showed accrued salaries of $22,200.The Accrued Salaries Payable account had a balance of $32,000 at the end of the current fiscal year,which was unchanged from its balance at the end of the prior fiscal year.The books of the company have not yet been closed.The entry needed in this situation would include a

(Multiple Choice)

4.7/5 (40)

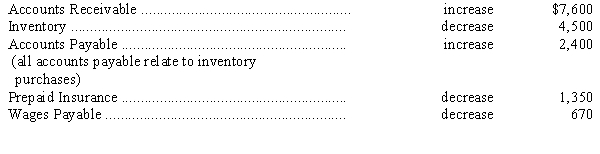

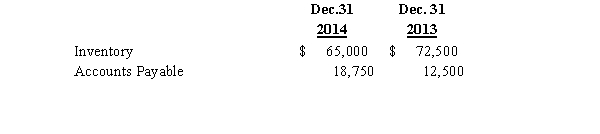

The following data are from a comparison of the balance sheets of Brassie Company as of December 31,2013,and December 31,2012:

The following data are from Brassie's 2011 income statement:

The following data are from Brassie's 2011 income statement:

During 2013:

(a)How much cash was collected from customers?

(b)How much cash was paid for inventory purchases?

(c)How much cash was paid for insurance?

(d)How much cash was paid for wages?

During 2013:

(a)How much cash was collected from customers?

(b)How much cash was paid for inventory purchases?

(c)How much cash was paid for insurance?

(d)How much cash was paid for wages?

(Essay)

4.9/5 (36)

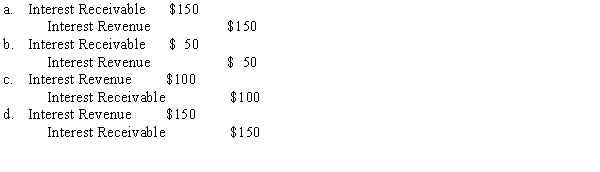

Five percent bonds with a total face value of $12,000 were purchased at par during the year.The last interest payment for the year was received on July 31.The bonds pay interest semiannually.The adjusting entry at December 31 would include a

(Multiple Choice)

4.8/5 (37)

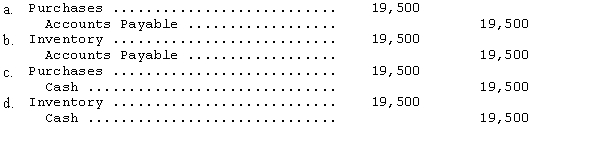

Iowa Cattle Company uses a perpetual inventory system.Iowa purchased cattle from Big D Ranch at a cost of $19,500,payable at time of delivery.The entry to record the delivery would be

(Short Answer)

4.8/5 (40)

If an expense has been incurred but not yet recorded,then the end-of-period adjusting entry would involve

(Multiple Choice)

4.8/5 (36)

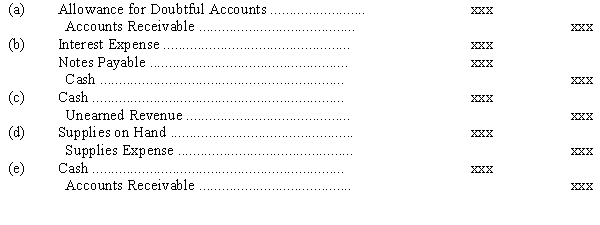

For each of the journal entries below,write a description of the underlying event.Assume that for prepaid expenses original debits are made to an expense account.

(Essay)

4.9/5 (37)

A company loaned $6,000 to another corporation on December 1,Year 1,and received a 90-day,10 percent,interest-bearing note with a face value of $6,000.The lender's December 31,Year 1,adjusting entry is

(Short Answer)

4.8/5 (36)

The information listed below was obtained from the accounting records of Williams Company as of December 31,2013,the end of the company's fiscal year.

(a)On August 1,2013,the company borrowed $120,000 from the Bank of

Wistful Vista.The loan was for 12 months at 9 percent interest payable at the maturity date.

(b)Finished goods inventory on January 1,2013,was $200,000,and on December 31,2013,it was $260,000.Cost of goods sold was $2,400,000.The company uses a perpetual inventory system.

(c)The company owned some property (land)that was rented to J.McArthur on April 1,2013,for 12 months for $8,400.On April 1,the entire annual rental of $8,400 was credited to rent collected in advance,and cash was debited.

(d).On September 1,2013,the company loaned $60,000 to an outside party.The loan was at 10 percent per annum and was due in six months; interest is payable at maturity.Cash was credited for $60,000,and notes receivable was debited on September 1 for the entire amount.

(e)Accrued salaries and wages are $18,000 at December 31,2013.

(f)On January 1,2013,factory supplies on hand equaled $200.During 2013,factory supplies costing $4,000 were purchased and debited to factory supplies inventory.At the end of 2013,a physical inventory count showed that factory supplies on hand equaled $800..

Prepare journal entries to adjust the books of Williams Company at December 31,2013.

(Essay)

4.9/5 (40)

Melville Company manufactures electronic components.The company is a calendar-year company.The records of the company show the following information:

Melville paid suppliers $122,500 during 2013.What is Melville's cost of goods sold?

Melville paid suppliers $122,500 during 2013.What is Melville's cost of goods sold?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)