Exam 20: Accounting Changes and Error Corrections

Exam 1: Financial Reporting89 Questions

Exam 2: A Review of the Accounting Cycle100 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements74 Questions

Exam 4: The Income Statement86 Questions

Exam 5: Statement of Cash Flows and Articulation83 Questions

Exam 6: Earnings Management47 Questions

Exam 7: The Revenuereceivablescash Cycle87 Questions

Exam 8: Revenue Recognition89 Questions

Exam 9: Inventory and Cost of Goods Sold134 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing111 Questions

Exam 13: Equity Financing97 Questions

Exam 14: Investments in Debt and Equity Securities88 Questions

Exam 15: Leases83 Questions

Exam 16: Income Taxes87 Questions

Exam 17: Employee Compensation-Payroll,pensions, Other Compissues83 Questions

Exam 18: Earnings Per Share86 Questions

Exam 19: Derivatives, contingencies, business Segments, and Interim Reports82 Questions

Exam 20: Accounting Changes and Error Corrections86 Questions

Exam 21: Statement of Cash Flows Revisited68 Questions

Exam 22: Accounting in a Global Market62 Questions

Exam 23: Analysis of Financial Statements65 Questions

Select questions type

On December 27,2014,Admission Company ordered merchandise for resale from Eviction,Inc.,that cost $7,000 (terms cash within 10 days).Eviction shipped the merchandise F.o.b. shipping point on December 28, 2014, and the goods arrived on January 2, 2015. The invoice was received on December 30, 2014. Admission Company did not record the purchase in 2014 and did not include the goods in ending inventory. The effects on Admission Company's 2014 financial statements were

(Multiple Choice)

4.8/5  (44)

(44)

Which of the following is the proper time period in which to record a change in accounting estimate?

(Multiple Choice)

4.8/5 (36)

Which of the following is characteristic of a change in accounting principle?

(Multiple Choice)

4.8/5 (38)

When a company acquires an asset that will provide benefits for several years,the cost of the asset is allocated over the asset's useful life.The allocation process is operationalized through the choice of one of the generally accepted depreciation methods.In choosing a depreciation method to apply,company management is required to make several estimates as part of this allocation process such as the following:

1.Over what period of time will benefits from using the asset accrue?

2.What will be the value of the asset when its use is discontinued?

3.Will the benefits be realized evenly of the life of the asset or will they be higher in some years than in others?

Required:

1.What factors should management consider in making a change in depreciation methods?

2.Explain how a change in depreciation methods is reported in the financial statements and why the Financial Accounting Standards Board chose this approach.

(Essay)

4.7/5 (40)

Ending inventory for 2012 is overstated by $5,500 due to a faulty count and costing.The tax rate is 39%.Assume the same accounting methods for both financial reporting and taxes.The error is discovered late in 2014.The 2014 annual report shows the financial statements for 2012,2013,2014 on a comparative basis.

Which of the following is correct regarding the reporting of this error in the 2014 annual report?

(Multiple Choice)

4.8/5 (38)

Effective January 2,2014,Moldaur Co.adopted the accounting principle of expensing advertising and promotion costs as they are incurred.Previously,advertising and promotion costs applicable to future periods were recorded in prepaid expenses.Moldaur can justify the change,which was made for both financial statement and income tax reporting purposes.Moldaur's prepaid advertising and promotion costs totaled $250,000 at December 31,2013.Assume that the income tax rate is 40 percent for 2013 and 2014.The adjustment for the effect of the change in accounting principle should result in a net charge against income in the income statement for 2014 of

(Multiple Choice)

4.8/5 (34)

Which of the following should NOT be reported retroactively?

(Multiple Choice)

4.8/5 (31)

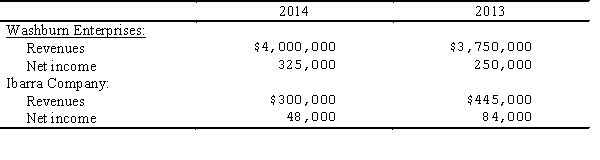

Washburn Enterprises acquired Ibarra Company for $850,000 December 31,2014.This amount exceeded the recorded value of Ibarra Company's net assets by $250,000 on the acquisition date.The entire excess of cost over the book value of the net assets related to a piece of equipment owned by Ibarra that had a remaining life of five years as of the acquisition date.The companies reported the following amounts for the 2013 and 2014:

Prepare the pro forma information for this acquisition required by ASC Topic 850.

Prepare the pro forma information for this acquisition required by ASC Topic 850.

(Essay)

4.8/5 (34)

On December 31,2014,Ohio Corporation appropriately changed its inventory valuation method to FIFO cost from LIFO cost for both financial statement and income tax purposes.The change will result in a $140,000 increase in the beginning inventory at January 1,2014.Assume a 30 percent income tax rate.The cumulative effect of this accounting change Ohio for the year ended December 31,2014,is

(Multiple Choice)

4.8/5 (35)

On January 1,2011,Always There Services Inc.purchased a new machine for $900,000.The machine had an estimated useful life of 10 years and a salvage value of $250,000.Always There elected to depreciate the machine using the double-declining-balance method.On January 1,2014,the company decided to change to straight-line depreciation.

Ignoring income tax considerations,prepare the entries to record

(1)Always There's 2013 depreciation expense.

(2)Always There's 2014 depreciation expense.

(Essay)

4.8/5 (51)

At the time Hollywood Corporation became a subsidiary of Vine Corporation,Hollywood switched depreciation of its plant assets from the straight-line method to the sum-of-the-years'-digits method used by Vine.With respect to Hollywood,this change was a

(Multiple Choice)

4.9/5 (40)

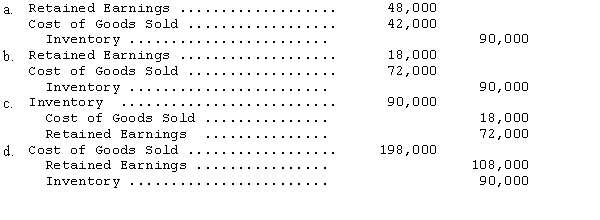

Cornwall Co.made the following errors in counting its year-end physical inventories:

The entry to correct the accounts at the end of 2014 is

The entry to correct the accounts at the end of 2014 is

(Short Answer)

4.7/5 (46)

Basilia Corporation purchased a machine for $180,000 on January 1,2013.Basilia will depreciate the machine using the straight-line method using a five-year period with no residual value.As a result of an error in its purchasing records,Basilia did not recognize any depreciation for the machine in its 2013 financial statements.Basilia discovered the problem during the preparation of its 2014 financial statements.What amount should Basilia record for depreciation expense on this machine for 2014?

(Multiple Choice)

4.8/5 (38)

Which of the following is characteristic of a change in accounting estimate?

(Multiple Choice)

4.7/5 (45)

An example of an item that should be reported as a prior period adjustment is the

(Multiple Choice)

4.8/5 (37)

On January 2,2012,Lynch Company acquired machinery at a cost of $800,000.This machinery was being depreciated by the double-declining-balance method over an estimated useful life of eight years,with no residual value.At the beginning of 2014,Lynch decided to change to the straight-line method of depreciation.Ignoring income tax considerations,the cumulative effect of this accounting change is

(Multiple Choice)

4.8/5 (37)

Diamond Company changed from the completed-contract method of accounting for long-term contracts to the percentage-of-completion method,during 2014.Reported earnings in 2013 were $50,000,and the beginning 2013 retained earnings balance was $150,000.Net income for 2014 under the competed-contract method would have been $140,000.No dividends were declared during 2013 and 2014.

Required:

Prepare the 2013 and 2014 comparative retained earnings statements.

Required:

Prepare the 2013 and 2014 comparative retained earnings statements.

(Essay)

4.8/5 (33)

Which of the following should be reported as a change in accounting estimate?

(Multiple Choice)

4.8/5 (50)

In reviewing the books of Unger Retailers Inc.,the auditor discovered certain errors that had occurred during 2013 and 2014.No errors were corrected during 2013.The errors are summarized below:

(a)Beginning merchandise inventory (January 1,2013)was understated by $8,640.

(b)Merchandise costing $2,400 was sold for $4,000 to B.J.Taylor on December 29,2013,but the sale was recorded in 2014.The merchandise was shipped F.O.B.shipping point and was not included in ending inventory.Unger uses a periodic inventory system.

(c)A two-year fire insurance policy was purchased on May 1,2013,for $5,760.The entire amount was debited to Prepaid Insurance.No adjusting entry was made in 2013 or 2014.

(d)A one-year note receivable of $9,600 was held by Unger beginning October 1,2013.Payment of the 10 percent note and accrued interest was received upon maturity.No adjusting entry was made on December 31,2013.

(e)Equipment with a ten-year life was purchased on January 1,2013,for $39,200.No depreciation expense was recorded during 2013 or 2014.Assume that the equipment has no salvage value and that Unger uses the straight-line method for recording depreciation.

Prepare journal entries to correct each of these independent situations.Assume that the nominal accounts for 2014 have not yet been closed into the income summary account.

(Essay)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)