Exam 4: Security Analysis and Portfolio Theory

Exam 1: Introduction12 Questions

Exam 2: Portfolio Analysis36 Questions

Exam 3: Models of Equilibrium in the Capital Markets46 Questions

Exam 4: Security Analysis and Portfolio Theory125 Questions

Exam 5: Evaluating the Investment Process12 Questions

Select questions type

Discuss whether the following statement is true or false:

The use of a dividend-discount model to value common stocks is inconsistent with strong-form efficiency but is consistent with weak-form efficiency.

(True/False)

4.9/5  (38)

(38)

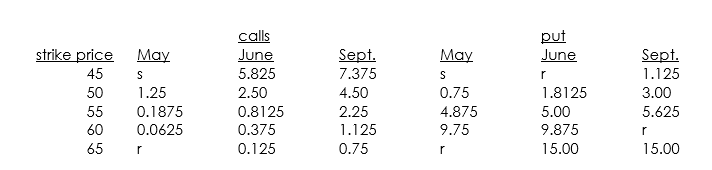

You have just learned through the grapevine that Pfizer (currently at $50.625 per share)may be a takeover candidate at $65 per share.You would like to speculate on the rumor,but you are worried that the stock will drop significantly if the rumor is false.Therefore,you have decided to use options to exploit this information.You are given the following option data for today,May 15th:

calls puts

a. Set up an option position that will best exploit the information you have, assuming that the takeover will happen by September 16 (the expiration day of the September options).

b. Assume now that the annualized standard deviation of Pfizer's stock price is 0.40 and that the six-month T-bill rate is 6%. Furthermore, assume that Pfizer pays a quarterly dividend of 50 cents and that the dividends are paid in April, July, October and January. What would your Black-Scholes estimates be for the options in the position that you have described in part a?

c. If the beta of Pfizer stock is 1.0, what is the beta of the position that you have set up in part a?

d. What are the deltas of the options that you have chosen for your position?

a. Set up an option position that will best exploit the information you have, assuming that the takeover will happen by September 16 (the expiration day of the September options).

b. Assume now that the annualized standard deviation of Pfizer's stock price is 0.40 and that the six-month T-bill rate is 6%. Furthermore, assume that Pfizer pays a quarterly dividend of 50 cents and that the dividends are paid in April, July, October and January. What would your Black-Scholes estimates be for the options in the position that you have described in part a?

c. If the beta of Pfizer stock is 1.0, what is the beta of the position that you have set up in part a?

d. What are the deltas of the options that you have chosen for your position?

(Essay)

4.8/5 (35)

It is now time 0.You are a bond portfolio manager using a barbell strategy to immunize.Your portfolio will consist of two bonds: bond A,which is a $100 par zero coupon bond maturing in five years; bond B,which is a $100 par zero-coupon bond maturing in ten years.You are trying to immunize a $1 million liability that is due in six years.The yield curve is flat at 10%,so you need a present value of $1 million/(1.10)6 = $564,474.

a. Of the $564,474, how much will you put in bond A and how much will you put in bond B? How many of the A and B bonds will you buy?

b. One minute after you set up the portfolio, the yield curve shifts up to 15% (staying flat). How much is your portfolio worth?

c. After the shift in part b, is your liability immunized? If not, what should you do to immunize it? Be specific, and give numbers if you can.

d. Now assume that the shift in part b never happened. You leave the firm and nobody bothers to look at the portfolio again until the end of year 4. Interest rates are still at 10%; there have been no further changes. At the end of year 4, a new bond portfolio manager takes over, goes through the files, and finds the records of the portfolio. What, if anything, will she have to do to keep the liability immunized? Be specific, and give numbers if you can.

(Essay)

4.8/5 (47)

Consider the purchase of a put option with an exercise price of $40 and a cost of $5 and the purchase of a call option with the same expiration date and on the same stock with an exercise price of $45 and a cost of $6.Graph the profit of this combination.Be sure to label all points.

(Essay)

4.7/5 (27)

You have just completed a study of small and large stocks and have obtained the following results:

s small stocks large stocks excess returns 5\% 0\% transactions cost 10\% 2\%

Given the difference in transactions costs,how long would your investment horizon have to be for small stocks to be a better investment than large stocks?

(Essay)

4.9/5 (40)

Herbert Avocado has just come up with an idea for a new type of financial intermediary,which is designed to take advantage of the opportunity presented by an inverted yield cure,such as the one that existed in 1981 when one-year bonds were yielding 16% and 30-year bonds were at 14%.When the yield curve becomes inverted,Avocado's firm will issue long-term bonds and use the proceeds to buy one-year instruments that have higher yields and are less risky.Avocado is now just waiting for the yield curve to become downward sloping again so that he can get his firm off the ground and make his fortune.What do you think of his plan?

(Essay)

4.8/5 (40)

What is the phenomenon of the size effect in stock performance? How does it relate to the "turn-of-the-year" ("year-end")effect? Can you suggest any good reason why the returns of small stocks,after adjusting for beta,still do better than those for large stocks? What strategy would you follow to exploit this anomaly? What factors do you have to keep in mind?

(Essay)

4.9/5 (40)

You have been hired as an analyst by a noted security analysis firm and asked to value two stocks.You have been given the following data on the two firms:

required return 20\% dividend payout ratio 20\% current EPS \ 1 return on investment 25\% stage of growth high

You estimate that firm 1 will become a stable firm after five years have passed,after which it will have a constant growth rate of 6%,and that firm 1's return on investment will remain unchanged.Value each firm.

(Essay)

4.7/5 (32)

One explanation of the "year-end" ("turn-of-the-year" or "January")effect has to do with sales and purchases related to the tax year.

a. Present the "tax-effect" hypothesis.

b. Studies have shown that the January effect occurs internationally, even in countries where the tax year does not start in January. Speculate on a good reason for this.

(Essay)

4.9/5 (46)

Suppose the U.S.Treasury issues $50 billion of 10-year notes over the next month to finance the budget deficit.Describe what should happen to the term structure of interest rates according to each of the following theories:

a. segmented markets

b. pure expectations

c. preferred habitat

d. liquidity preference

What do you think would actually happen?

(Essay)

4.8/5 (32)

a.Define the duration of a bond.Why is duration often thought of as a measure of risk for a bond?

b.What is the duration of a two-year zero-coupon bond? How about a two year 10% coupon bond (one coupon per year)?

c.How does a given bond's duration change when interest rates in the market rise?

d.Explain how duration is used in setting up an immunization strategy.

a. Define the duration of a bond. Why is duration often thought of as a measure of risk for a bond?

b. What is the duration of a two-year zero-coupon bond? How about a two year 10% coupon bond (one coupon per year)?

c. How does a given bond's duration change when interest rates in the market rise?

d. Explain how duration is used in setting up an immunization strategy.

(Essay)

4.8/5 (44)

Assume that one can purchase gold bars or 6-month futures on gold bars.

a. Using the law of one price, derive the relationship between the spot price of gold and the futures contract price.

b. Assume that the futures are underpriced relative to the contract price just derived. What action should an investor take?

(Essay)

5.0/5 (41)

a.Explain why futures trading is a zero-sum game.Are options also a zero-sum game? What about buying warrants?

b.Suppose you are long 100 shares of XYZ stock at 50 and you have written a December 50 call option against your long position.Do you want the stock price to go up or down tomorrow? Explain.

c.Answer part b if you have written a December 50 put option instead of the call option.

(Essay)

4.9/5 (35)

You have been asked to determine the theoretical bounds on a futures contract on gold.You are supplied with the following information: spot price of gold = $400/troy oz.; time to expiration on futures contract = 6 months; riskless rate = 10%; borrowing rate for marginal investor = 12%; lending rate for marginal investor = 8%; storage costs for gold = $20/troy oz.per year.Short sellers can hope to recover only half of the storage costs that they save by short selling.

a. What is the upper bound on the theoretical futures price?

b. (Recalculate the new bounds.)

b. What is the lower bound on the theoretical futures price?

c. Assume that investors are required to put up a 10% margin on all futures transactions and that only cash (no T-bills) can be used to meet margin requirements. Evaluate the effect this would have on the upper and lower bounds you estimated in part a and part

(Essay)

4.9/5 (31)

Discuss whether the following statement is true or false:

Two portfolios with matching cash flows are always immunized.

(True/False)

4.9/5 (29)

In November 1978,the Fed announced a stringent new program to combat inflation,which had gotten out of hand.The response in the financial markets was the Treasury bill yields increased while long-term yields dropped.Can you explain why?

(Essay)

4.8/5 (34)

Discuss whether the following statement is true or false:

A certain retailing firm has a strong seasonal pattern to its sales.Therefore,we would expect to find a seasonal pattern to its stock price as well.

(True/False)

4.8/5 (39)

Consider the following securities: a fully taxable coupon bond paying 12 in one year,112 in two years,selling at 103; a fully taxable coupon bond paying 5 in one year,105 in two years,selling at 92; a municipal bond paying 8 in one year,108 in two years,selling at 98; a bank account paying 10%.

a. Which of the above securities is most attractive to an investor in the 40% effective tax bracket? (Ignore capital gains tax)

b. Which one is most attractive to a tax-exempt investor?

(Essay)

4.9/5 (37)

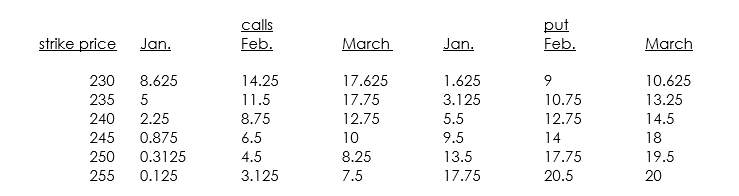

The trade deficit numbers are expected out on February 19,and you think that market will move a lot,either up or down.You want to take advantage of this using options.You are given the following stock-index option data for today,January 14 (the current level of the index is 236.99,and the annualized T-bill rate is 6%):

a. Find at least two options in the above listing that violate arbitrage

conditions.

b. How would you set up a position using February options to take advantage

of the volatility from the trade deficit numbers? (The February options expire

on the evening of February 19.)

c. What are the breakeven points for the position in part b? (You can draw a

payoff diagram if you want to.)

d. Assume no dividends are paid and that the variance in the stock index is

0.09, and use the Black-Scholes model to value the February 235 call and

the February 235 put.

a. Find at least two options in the above listing that violate arbitrage

conditions.

b. How would you set up a position using February options to take advantage

of the volatility from the trade deficit numbers? (The February options expire

on the evening of February 19.)

c. What are the breakeven points for the position in part b? (You can draw a

payoff diagram if you want to.)

d. Assume no dividends are paid and that the variance in the stock index is

0.09, and use the Black-Scholes model to value the February 235 call and

the February 235 put.

(Essay)

4.7/5 (35)

Which of the following is not a general conclusion of studies of stock prices?

(Multiple Choice)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)