Exam 15: Cost Allocation: Joint Products and Byproducts

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-The incremental benefit or (loss) of processing Kharton into Kraxton is:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-The incremental benefit or (loss) of processing Kharton into Kraxton is:

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

C

Scrap frequently has a zero sales value.

Free

(True/False)

4.9/5 (35)

Correct Answer:Verified

True

Explain the difference between a joint product and a byproduct. Can a byproduct ever become a joint product?

Free

(Essay)

4.9/5 (39)

Correct Answer:Verified

The differentiating factor between a joint product and a byproduct is the sales value at the splitoff point. Joint products have high total sales value at the splitoff point. A byproduct has a low total sales value at the splitoff point. Products can change from byproducts to joint products when their total sales values increase significantly.

Use the information below to answer the following question(s).

Troy Company processes 15,000 litres of direct materials to produce two products, Product X and Product Y. Product X, a byproduct, sells for $4 per litre, and Product Y, the main product, sells for $50 per litre. The following information is for August:

The manufacturing costs totalled $15,000.

-How much is the ending inventory reduction for the byproduct if byproducts are recognized in the general ledger at the point of sale?

The manufacturing costs totalled $15,000.

-How much is the ending inventory reduction for the byproduct if byproducts are recognized in the general ledger at the point of sale?

(Multiple Choice)

4.8/5 (36)

The net realizable value method can be used for products for which there may not be any market price available at split off.

(True/False)

4.9/5 (37)

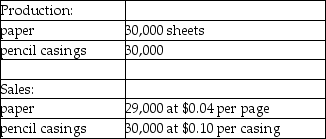

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the split off point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the split off point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the split off point?

Cost of purchasing 50 trees and processing them up to the split off point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What is the paper's sales value at the split off point?

(Multiple Choice)

4.9/5 (47)

What method is used when joint costs are allocated according to each item's relative proportion of weight at the split off point?

(Multiple Choice)

4.8/5 (41)

Use the information below to answer the following question(s).

Chem Manufacturing Company processes direct materials up to the split off point, where two products (X and Y) are obtained and sold. The following information was collected for the month of November.

Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the split off point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

The cost of purchasing 10,000 litres of direct materials and processing it up to the split off point to yield a total of 9,500 litres of good products was $975,000.

The beginning inventories totalled 50 litres for X and 25 litres for Y. Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y. October costs were per unit were the same as November.

-What is the approximate portion of the joint costs that should be allocated to products X and Y, respectively, using a physical volume measure?

(Multiple Choice)

4.9/5 (39)

The sales value at split off method allocates joint costs according to each product's value, at the split off point, of the total production in the accounting period of each product.

(True/False)

4.9/5 (34)

AllCanada Wire Products processes copper into wire. It makes 12 gauge and 14 gauge wire. During April the joint costs of processing the aluminium were $365,000. There were no beginning or ending inventories for the month. Production and sales value information for the month were as follows:

Required:

Determine the amount of joint costs allocated to each product if the constant gross-margin percentage method is used.

Required:

Determine the amount of joint costs allocated to each product if the constant gross-margin percentage method is used.

(Essay)

4.8/5 (37)

Explain the difference between a joint product and a byproduct. Can a byproduct ever become a joint product?

(Essay)

4.9/5 (32)

CSI Chemical, Inc. processes pine rosin into three products; turpentine, paint thinner, and spot remover. During May the joint costs of processing were $240,000. Production and sales value information for the month were as follows:

Required:

Determine the amount of joint cost allocated to each product if the sales value at split off method is used.

Required:

Determine the amount of joint cost allocated to each product if the sales value at split off method is used.

(Essay)

4.9/5 (31)

Use the information below to answer the following question(s).

Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the split off point, where two products (paper and pencil casings) are obtained. The products are then sold to an independent company that markets and distributes them to retail outlets. The following information was collected for the month of October.

Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the split off point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.

Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-What are the approximate joint costs assigned to the paper ending inventory if joint costs are allocated using the sales value at split off method?

(Multiple Choice)

4.9/5 (46)

Costs which are assignable beyond the split off point at which individual products emerge are called

(Multiple Choice)

4.7/5 (38)

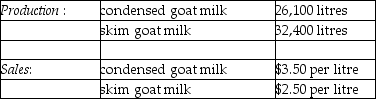

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using estimated net realizable value, what amount of the $72,240 of joint costs would be allocated Xyla and the skim goat ice cream?

(Multiple Choice)

4.9/5 (40)

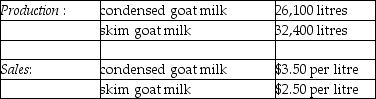

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Assuming Cranbrook uses the sales value at split off method and 2,000 containers of Jarlon and 75 containers of Kharton are unsold at the end of the period, Cranbrook would report ending inventory of:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Assuming Cranbrook uses the sales value at split off method and 2,000 containers of Jarlon and 75 containers of Kharton are unsold at the end of the period, Cranbrook would report ending inventory of:

(Multiple Choice)

4.9/5 (31)

Lumber Company prepares lumber for companies who manufacture furniture. The main product is finished lumber with a byproduct of wood shavings. The byproduct is sold to plywood manufacturers. For July the manufacturing process incurred $166,000 in total costs. Eighty thousand board metres of lumber were produced and sold along with 6,800 kilograms of shavings. The finished lumber sold for $3.00 per boardmetre and the shavings sold for $0.30 a kilogram. There were no beginning or ending inventories.

Required:

Prepare an income statement showing the byproduct (1) as a cost reduction during production and (2) as a revenue item when sold.

(Essay)

4.9/5 (43)

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of the skim goat ice cream at the splitoff point?

(Multiple Choice)

4.9/5 (47)

The constant gross-margin percentage NRV method allocates joint costs to joint products in such a way that the gross margin on each joint product is the same as it was in the previous year.

(True/False)

4.8/5 (32)

The constant gross-margin percentage method differs from market-based joint-cost allocation method (sales value at splitoff and estimated net realizable value) since no account is taken of profits earned before or after the splitoff point when allocating joint costs.

(True/False)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)