Exam 15: Cost Allocation: Joint Products and Byproducts

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

Byproducts are recognized in the general ledger either at the time of production or at the time of sale.

(True/False)

4.9/5  (37)

(37)

CSI Chemical, Inc. processes pine rosin into three products; turpentine, paint thinner, and spot remover. During May the joint costs of processing were $240,000. Production and sales value information for the month were as follows:

Required:

Determine the amount of joint cost allocated to each product if the physical measure method is used.

Required:

Determine the amount of joint cost allocated to each product if the physical measure method is used.

(Essay)

4.8/5 (36)

Trundle Ltd. produces 2 main products, J and K, and a by-product, L. There were no beginning inventories. During April, it incurred $275,000 of joint costs, which are allocated to main products using the physical output method. Additional information follows:

Required:

Assuming Trundle recognizes byproduct revenue at the time of sale, what is the total value of ending inventory?

Required:

Assuming Trundle recognizes byproduct revenue at the time of sale, what is the total value of ending inventory?

(Essay)

4.9/5 (37)

In rate regulation settings, which method is usually preferred over the sales value method?

(Multiple Choice)

4.9/5 (45)

Which of the following methods allocates joint costs according to the appraised final sales value in the ordinary course of business less the appraised separable costs of production and marketing?

(Multiple Choice)

4.7/5 (30)

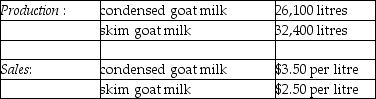

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using the sales value at splitoff method, what is the gross-margin percentage for skim goat milk at the splitoff point?

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using the sales value at splitoff method, what is the gross-margin percentage for skim goat milk at the splitoff point?

(Multiple Choice)

4.8/5 (34)

The estimated net realizable value method allocates joint costs on the basis of the expected final sales value in the ordinary course of business, less the expected separable costs of production and marketing of the total production for the period.

(True/False)

4.9/5 (38)

Identify each item on the following list as a joint cost or a separable cost.

a. Cost of processing crude oil in a gasoline refinery.

b. Cost of processing timber (trees) at a sawmill.

c. Cost of processing lumber into different lengths and sizes at a sawmill.

d. Cost of raw tomato processing, tomatoes are to be used for different soups in a soup plant.

e. Cost of canning soup in a soup plant.

f. Cost of moulding plastic for use in making different toys on an assembly line.

h. Cost of processing water for human consumption.

i. Cost of processing pulp into paper.

j. Cost of processing pulp into cardboard.

h. Cost of processing water for human consumption.

i. Cost of processing pulp into paper.

j. Cost of processing pulp into cardboard.

(Essay)

4.9/5 (29)

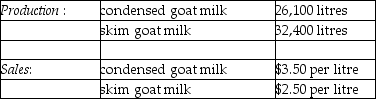

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of Xyla at the splitoff point?

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-What is the estimated net realizable value of Xyla at the splitoff point?

(Multiple Choice)

4.7/5 (34)

Which of the following methods calculates expected profits before any costs are allocated?

(Multiple Choice)

4.8/5 (39)

Proper joint cost allocations for inventory costing and cost-of-goods-sold computations are important because

(Multiple Choice)

4.9/5 (39)

A sound reason for reporting revenue from byproducts as an income statement item at the time of sale is to lessen the chance of managers managing reported earnings.

(True/False)

4.9/5 (37)

Product X is sold for $8 a unit and Product Y is sold for $12 a unit. Each product can also be sold at the splitoff point. Product X can be sold for $5 and Product Y for $4. Joint costs for the two products totaled $4,000 for January for 600 units of X and 500 units of Y. What are the respective joint costs assigned each unit of products X and Y if the sales value at splitoff method is used?

(Multiple Choice)

4.8/5 (33)

Which of the following statements is true regarding main products, byproducts, and scrap?

(Multiple Choice)

4.8/5 (31)

Golden Company uses one raw material, gold ore, for all its products. It spends considerable time getting the gold from the ore before it starts the actual processing of the finished products, rings, lockets, etc. Traditionally, the company made one product at a time and charged the product with all costs of production, from ore to final inspection. However, in recent months the cost accounting reports have been somewhat disturbing to management. It seems that some of the finished products are costing more than they should, even to the point of approaching their retail value. It has been noted by the accounting manager that this problem began when the company started buying ore from different parts of the world, some of which requires difficult extraction methods.

Required:

Can you explain how the company might change its accounting system to better reflect the reporting problems? Are there other problems with the purchasing area?

(Essay)

4.8/5 (34)

The sales value at split off method can be used to value inventory as well as determining cost of goods sold.

(True/False)

4.9/5 (40)

Land and Sea Corporation processes frozen chicken. The company has not been pleased with its profit margin per product because it appears that the high value items have too few costs assigned to them while the low value items have too many costs assigned to them. The processing results in several products, the primary one of which is frozen small hens. Other products include frozen parts such as wings and legs, byproducts such as skin and bones, and unused scrap items.

Required:

What may be the cost assignment problem if a key consideration is the value of the products being sold?

(Essay)

4.9/5 (43)

Answer the following question(s) using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result. The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240. There were no inventory balances of either product.

Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage) of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre. Xyla can be sold for $18 per litre.

Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50. The product can be sold for $9 per litre.

There are no beginning and ending inventory balances.

-Using the NRV method, the amount of joint costs allocated to Kraxton is:

(Multiple Choice)

4.8/5 (31)

Which of the following statements is true in regard to the cause-and-effect relationship between allocated joint costs and individual products?

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)