Exam 11: Partnerships: Distributions, Transfer of Interests, and Terminations

Exam 1: Understanding and Working With the Federal Tax Law74 Questions

Exam 2: Corporations: Introduction and Operating Rules113 Questions

Exam 3: Corporations: Special Situations109 Questions

Exam 4: Corporations: Organization and Capital Structure92 Questions

Exam 5: Corporations: Earnings Profits and Dividend Distributions130 Questions

Exam 6: Corporations: Redemptions and Liquidations115 Questions

Exam 7: Corporations: Reorganizations140 Questions

Exam 8: Consolidated Tax Returns175 Questions

Exam 9: Taxation of International Transactions177 Questions

Exam 10: Partnerships: Formation, Operation, and Basis135 Questions

Exam 11: Partnerships: Distributions, Transfer of Interests, and Terminations144 Questions

Exam 12: S: Corporations158 Questions

Exam 13: Comparative Forms of Doing Business170 Questions

Exam 14: Taxes on the Financial Statements87 Questions

Exam 15: Exempt Entities185 Questions

Exam 16: Multistate Corporate Taxation187 Questions

Exam 17: Tax Practice and Ethics174 Questions

Exam 18: The Federal Gift and Estate Taxes222 Questions

Exam 19: Family Tax Planning188 Questions

Exam 20: Income Taxation of Trusts and Estates183 Questions

Select questions type

Match the following statements with the best match from the choices below. Note: Choice L may be used more than once.

a. Cash basis accounts receivable, for example.

b. Fair market value exceeds 120% of basis.

c. Inside basis of partnership property can be adjusted to reflect the purchase price paid.

d. Terminates the partner's interest in the partnership.

e. Ordinary income-producing items.

f. Cash, then inventory and unrealized receivables, then other assets.

g. Does not eliminate the partner's interest in the partnership.

h. Liquidation of the partner's interest in hot assets.

i. Changes the partner's or the partnership's ordinary income potential.

j. Any partnership assets other than cash, capital, or § 1231 assets.

k. Sometimes treated as an unrealized receivable.

l. No correct match provided.

-Nonliquidating distribution

(Short Answer)

4.9/5  (29)

(29)

Several years ago, the Jaymo Partnership purchased 2,000 shares of ABCO stock (publicly traded) for $40,000; the stock now has a fair market value of $90,000. If this stock is distributed to Jason in liquidation of his 30% partnership interest, it is treated as a cash distribution of $75,000 and a property distribution of $15,000. Assume Jaymo owns no other securities.

(True/False)

4.7/5 (32)

Which of the following statements, if any, about a multi-member LLC is false?

(Multiple Choice)

4.9/5 (34)

Carlos receives a proportionate liquidating distribution consisting of $8,000 cash and inventory with a basis to the partnership of $5,000 and a fair market value of $6,000. His basis in his partnership interest was $15,000 immediately before the distribution. Carlos assigns a basis of $7,000 to the inventory, and recognizes no gain or loss.

(True/False)

4.7/5 (42)

Matt, a partner in the MB Partnership, receives a proportionate, nonliquidating distribution of property having a fair market value of $16,000 and a partnership basis of $23,000. Matt's basis in the partnership is $10,000 before the distribution. In this situation, Matt will recognize no gain or loss. He will take a $10,000 basis in the property, and his basis in the partnership interest is reduced to zero.

(True/False)

4.8/5 (36)

Generally, a distribution of property does not result in gain to a partner on either a current or liquidating distribution. A situation where a gain may arise, however, is when a partner contributed appreciated property to the partnership and that property is distributed back to the contributing partner within seven years of the contribution.

(True/False)

5.0/5 (46)

Cindy, a 20% general partner in the CDE Partnership, wants to retire and has approached the other partners about having the partnership buy her out. The partnership is a cash basis, service oriented partnership in which Cindy is an active partner. The partnership's assets consist primarily of unrealized receivables and cash. The partnership also has substantial going concern value (goodwill) which is probably its most valuable asset. The other partners in the partnership are also active in the business and are not related to Cindy.

Discuss from Cindy's viewpoint how you would structure the liquidation of her interest under § 736. Answer as if you are her advocate. Do you think the other partners will agree with this structure? If not, what structure would they prefer?

(Essay)

4.9/5 (37)

Last year, Darby contributed land (basis of $60,000, fair market value of $80,000) to the Seagull LLC in exchange for a 25% interest in the LLC. In the current year, the LLC distributes the land (now worth $82,000) to Shelby, who is also a 25% owner. Immediately prior to the distribution, Darby's basis in the LLC was $70,000, while Shelby's basis in the LLC was $110,000. How much gain or loss must be recognized and by whom? What is Shelby's basis in the property she receives and Darby's basis in her partnership interest following the distribution?

(Multiple Choice)

4.9/5 (39)

Match the following statements with the best match from the choices below. Note: Choice N may be used more than once.

a. Includes the partner's share of partnership liabilities.

b. Could result from sale of a partnership interest for more than the partner's share of the inside basis of assets.

c. Liquidation payments from this type of partnership are always § 736(b) payments.

d. Could arise if a distribution results in loss to the distributee partner.

e. May be a § 736(a) payment.

f. May receive § 736(a) payments.

g. Probably treated as a general partner for § 736 purposes

h. Sale of more than 50% in less than 12 months.

i. Liquidation payments from this type of partnership may include § 736(a) payments.

j. A § 736(b) payment.

k. Adjustment designed to bring inside and outside bases into balance.

l. Partnership asset basis is at least $250,000 > FMV.

m. Would result if the partner contributes appreciated property to the partnership.

n. No correct match is provided.

-Step down

(Short Answer)

4.9/5 (41)

Suzy owns a 30% interest in the JSD LLC. In liquidation of the entity, Suzy receives a proportionate distribution of $30,000 cash, inventory (basis of $16,000, fair market value of $18,000), and land (basis of $25,000, fair market value of $30,000). Suzy's basis in the entity immediately before the distribution was $80,000. As a result of the distribution, what is Suzy's basis in the inventory and land, and how much gain or loss does she recognize?

(Multiple Choice)

4.8/5 (40)

The RST Partnership makes a proportionate distribution of its assets to Ryan, in complete liquidation of his partnership interest. The distribution consists of $40,000 in cash and capital assets with a basis to the partnership of $30,000 and a fair market value of $48,000. None of the payment is for partnership goodwill. At the time of the distribution, Ryan's partnership basis is $45,000 and the partnership has no liabilities and no "hot assets." If the partnership makes an optional basis adjustment election on a timely filed return, it recognizes:

(Multiple Choice)

4.7/5 (39)

Landis received $90,000 cash and a capital asset (basis of $50,000, fair market value of $60,000) in a proportionate liquidating distribution. His basis in his partnership interest was $120,000 prior to the distribution. How much gain or loss does Landis recognize and what is his basis in the asset received?

(Multiple Choice)

4.8/5 (38)

A § 754 election is made for a tax year in which the partner recognizes gain or loss on a distribution from the partnership or the distributee partner's basis in distributed property is increased or decreased from the inside basis the partnership held in those assets. The election is made by the partnership each year in which it is necessary to adjust a partner's share of the inside basis of partnership assets. In a year in which an unfavorable result would arise, the partnership can forego making the election.

(True/False)

5.0/5 (32)

In a proportionate nonliquidating distribution of cash and a capital asset, the partner recognizes gain to the extent the amount of cash plus the fair market value of property distributed exceeds the partner's basis in the partnership interest.

(True/False)

4.8/5 (35)

Marcie is a 40% member of the M&A LLC. Her basis is $10,000 immediately before the LLC distributes to her $30,000 of cash and land (basis to the LLC of $20,000 and fair market value of $25,000). As a result of the proportionate, nonliquidating distribution, Marcie recognizes a gain of $20,000 and her basis in the land is $0.

(True/False)

4.8/5 (37)

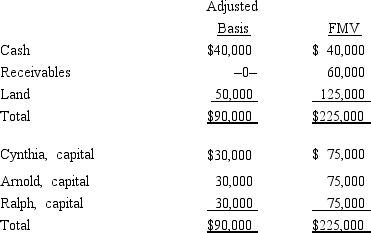

Cynthia sells her 1/3 interest in the CAR Partnership to Brandon for $95,000 cash. On the date of sale, the partnership balance sheet and agreed-upon fair market values were as follows:  If the partnership has a § 754 election in effect, the total "stepup" in basis of partnership assets that will be allocated to Brandon is:

If the partnership has a § 754 election in effect, the total "stepup" in basis of partnership assets that will be allocated to Brandon is:

(Multiple Choice)

4.8/5 (43)

A distribution can be "proportionate" (as defined for purposes of Subchapter K) even if only one partner receives assets from the partnership.

(True/False)

4.8/5 (46)

Match the following independent descriptions as "hot" (i.e., ordinary income) or nonhot assets with the statements below.

a. Hot assets for purposes of distributions, liquidation of a partnership interest under § 736, and sale of a

partnership interest.

b. May be a hot asset for some but not all the purposes stated in (a).

c. Not a hot asset.

-Cash basis accounts receivable.

(Short Answer)

4.8/5 (45)

Beth sells her 25% partnership interest to Katie for $50,000 cash on July 1 of the current tax year. Katie also assumed Beth's share of the partnership's liabilities. Beth's basis in her partnership interest at the beginning of the year was $40,000, including a $15,000 share of partnership liabilities. The partnership's income for the entire year was $100,000, and Beth's share of partnership debt was $10,000 as of the date she sold the partnership interest. Assume the partnership has no hot assets and that its income is earned evenly throughout the year. Beth recognizes a gain of $12,500 on the sale.

(True/False)

4.9/5 (40)

Catherine's basis was $50,000 in the CAR Partnership just before she received a proportionate nonliquidating distribution consisting of land held for investment with a basis to CAR of $40,000 (value of $60,000), and inventory with a basis of $40,000 (value of $40,000). After the distribution, Catherine's bases in the land and inventory are:

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)