Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice48 Questions

Exam 2: Consolidated Statements: Date of Acquisition44 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition37 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes43 Questions

Exam 5: Intercompany Transactions: Bonds and Leases54 Questions

Exam 6: Cash Flow, Eps, and Taxation48 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary42 Questions

Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares41 Questions

Exam 9: The International Accounting Environment17 Questions

Exam 10: Foreign Currency Transactions75 Questions

Exam 11: Translation of Foreign Financial Statements79 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise63 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities36 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations47 Questions

Exam 15: Government and Not for Profit Accounting44 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds60 Questions

Exam 17: Financial Reporting Issues37 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations61 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations83 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role56 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations49 Questions

Exam 22: Derivatives and Related Accounting Issues60 Questions

Exam 23: Equity Method for Unconsolidated Investments25 Questions

Exam 24: Variable Interest Entities10 Questions

Select questions type

Two types of intercompany stock purchases significantly complicate the consolidation process.The first occurs when the subsidiary issues added shares of stock in a public issue and the parent buys a portion of the shares.The second occurs when the subsidiary purchases outstanding shares of the parent company.

?

Required:

?

a.Discuss the current theoretical consolidation procedure for situations in which the parent buys a portion of the newly issued subsidiary shares that is (1) equal to its existing ownership percentage, (2) greater than its existing ownership percentage, and (3) less than its existing ownership percentage.?

?

b.Discuss the most widely supported, current theoretical consolidation procedures used when the subsidiary purchases outstanding common stock shares of the parent.?

(Essay)

4.8/5  (28)

(28)

When a subsidiary purchases shares of the parent, on a consolidated basis:

(Multiple Choice)

4.8/5 (33)

On January 1, 2016, Parent Company purchased 9,000 shares of the common stock of Subsidiary Company for $405,000.On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares issued and outstanding.Other paid-in capital and retained earnings were $150,000 and $200,000 respectively.On January 1, 2016, any excess of cost over book value is due to a patent, to be amortized over 10 years.

?

Subsidiary's net income and dividends for two years were:

?

?

2016 2017 Netincome \ 50,000 \ 80,000 Dividends 10,000 20,000 On January 1, 2017, Subsidiary Company sold an additional 2,000 shares of common stock for $50 per share.Parent purchased 1,200 shares of the new issue, and non-controlling shareholders purchased the other 800.

?

For both 2016 and 2017, Parent Company has applied the simple equity method.

?

Required:

?

a.Prepare a schedule that measures Parent's change in interest ownership effective with Sub's issuance of the 2,000 shares and Parent's acquisition of 1,200 of those shares.?

b.Prepare Parent's journal entry to record its purchase of the 1,200 shares on 1/1/17

?

c.Prepare a schedule showing the 12/31/17 balance of Parent's Investment in Sub account

(Essay)

4.9/5 (36)

Plum Inc.acquired 90% of the capital stock of Sterling Co.on 1/1/16 at a cost of $540,000.On this date Sterling had equipment (10-year life) carried at $200,000 under market and total equity amounting to $350,000.

On 1/1/16 Sterling acquired 5% (10,000 shares) of Plum's outstanding common stock for $3 per share.Internally generated net income was $50,000 for Plum and $40,000 for Sterling.

Consolidated net income for 2017 is

(Multiple Choice)

4.9/5 (40)

Company P owns 80% of the 10,000 outstanding common stock of Company S.If Company S issues 2,500 added shares of common stock, and Company P purchases some of the newly issued shares, which of the following statements is true?

(Multiple Choice)

4.9/5 (38)

On January 1, 2016, Paul, Inc.acquired a 90% interest in Stephan Company.The $45,000 excess of purchase price (parent's share only) was attributable to goodwill.On January 1, 2018, Stephan Company had the following stockholders' equity: ?

Common stock, \ 10 par \ 100,000 Other paid-in capital 200,000 Retained earnings 300,000

On January 2, 2018, Stephan sold 2,000 additional shares in a private offering.Stephan issued the new shares for $80 per share; Paul, Inc.purchased all the shares.What is the journal entry that Paul will prepare to record this investment?

?

a.

Investment in Stephan 160,000 Cash 160,000

b. Investment in Stephan 156,692 Paid-in Capital in Excess of Par-Paul 3,308 Cash 160,000

c.

Investment in Stephan 157,527 Paid-in Capital in Excess of Par-Paul 2,473 Cash 160,000

d.

Investment in Stephan 160,000 Paid-in Capital in Excess of Par-Paul 2,829 Cash 157,171

(Short Answer)

4.9/5 (42)

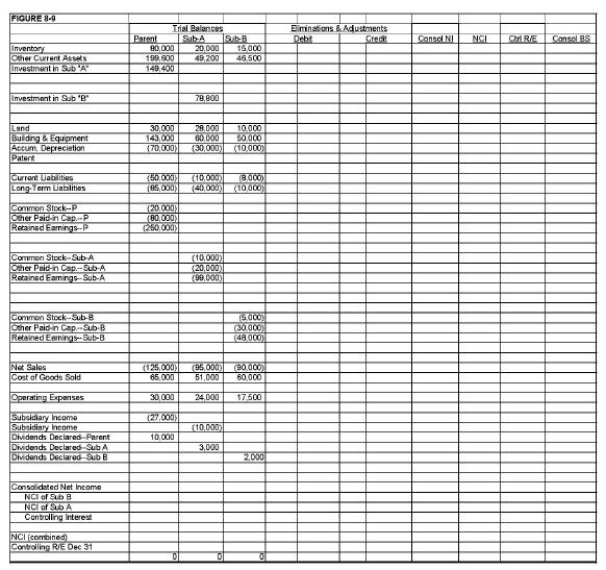

On January 1, 2016, Parent Company purchased 90% of the common stock of Sub-A Company for $90,000.On this date, Sub-A had common stock, other paid-in capital, and retained earnings of $10,000, $20,000, and $60,000 respectively.

On January 1, 2017, Sub-A Company purchased 80% of the common stock of Sub-B Company for $64,000.On this date, Sub-B Company had common stock, other paid-in capital, and retained earnings of $5,000, $30,000, and $40,000 respectively.

Any excess of cost over book value on either purchase is due to a patent, to be amortized over ten years.

Both Parent and Sub-A have accounted for their investments using the simple equity method.

During 2017, Sub-B sold merchandise to Sub-A for $20,000, of which one-fourth is still held by Sub-B on December 31, 2017.Sub-B's usual gross profit is 40%.During 2018, Sub-B sold more goods to Sub-A for $30,000, of which $10,000 is still on hand on December 31, 2018.

Required:

Complete the Figure 8-9 worksheet for consolidated financial statements for 2018.

(Essay)

4.9/5 (42)

A owns 80% of B and 20% of C.B owns 32% of C, and C owns 10% of A.Which interest will be considered NCI in the consolidated balance sheet?

(Multiple Choice)

4.9/5 (37)

Apple Inc.owns a 90% interest in Banana Company.Banana Company, in turn, owns a 80% interest in Carrot Company.During 2019, Carrot Company sold $50,000 of merchandise to Apple Inc.at a gross profit of 20%.Of this merchandise, $10,000 was still unsold by Apple Inc.at year end.The adjustment to the controlling interest in consolidated net income for 2019 is ____.

(Multiple Choice)

4.7/5 (34)

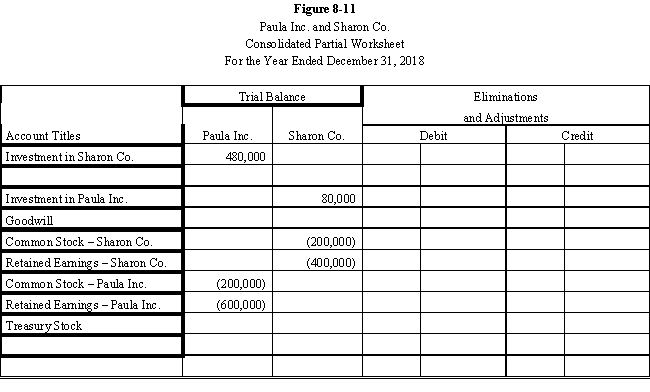

Paula Inc.purchased an 80% interest in the Sharon Co.for $480,000 on January 1, 2016, when Sharon Co.had the following stockholders' equity:

?

?

Common stock, \ 10 par \ 200,000 Retained earnings Total equity \

Any excess is attributable to goodwill.

?

On January 1, 2018, Sharon Co.purchased a 10% interest in the Paula Inc.at a price equal to book value.Both firms maintain investments under the cost method.

?

Required:

?

a.Complete the Figure 8-11 partial worksheet for December 31, 2018, assuming the use of the treasury stock method.?

?

b.Calculate the distribution of income for 2018, assuming that internally generated net income is $50,000 for Paula and $20,000 for Sharon.?

?

(Essay)

4.8/5 (44)

On January 1, 2016, Paris Ltd.paid $600,000 for its 75% interest in the Scott Company when Scott had total equity of $550,000.Any excess of cost over book value was attributed to equipment with a 10-year life.On January 1, 2018, Scott Company had the following stockholders' equity: ?

Common stock, \ 10 par \ 100,000 Other paid-in capital 200,000 Retained earnings 350,000

On January 2, 2018, Scott Company sold 2,500 additional shares of stock for $90 each in a private offering to non-controlling shareholders.As a result of this sale, which of the following changes would appear in the 2018 consolidated statements?

(Multiple Choice)

4.9/5 (39)

Which of the following situations is viewed as the parent having treasury stock?

(Multiple Choice)

4.8/5 (37)

Able Company owns an 80% interest in Barns Company and a 20% interest in Carns Company.Barns owns a 40% interest in Carns Company.The reported income of Carns is $20,000 for 2019.Which of the following shows how it will be distributed? ?

Barns Carns Controlling Non- Non- Interest Controlling Controlling

A) \ 10,400 \ 1,600 \ 8,000

B) \ 2,000 \ 8,000 \ 8,000

C) \ 12,000 \ 0 \ 8,000

D) \ 10,400 \ 9,600 \ 0

(Short Answer)

4.9/5 (36)

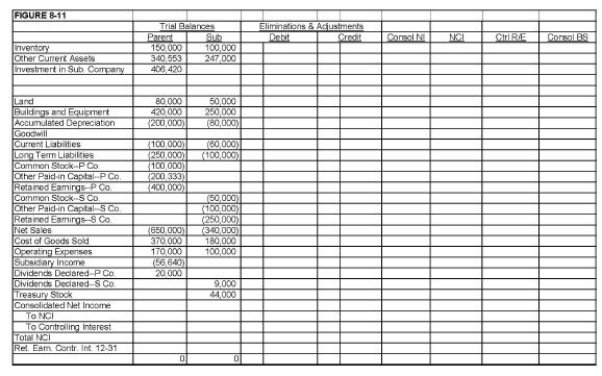

On January 1, 2016, Parent Company purchased 85% of the common stock, 8,500 shares, of Subsidiary Company for $317,500.On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of $50,000, $100,000, and $200,000 respectively.Any excess of cost over book value is due to goodwill.

?

On January 1, 2017, Subsidiary purchased, from its non-controlling shareholders, 1,000 shares of its common stock, 10% of the stock outstanding on that date.The price paid was $44,000.

?

Required (round all amounts to whole dollars; round percentages to one decimal: XX.X%)

a.Prepare an analysis to determine Parent's revised ownership interest following Sub's treasury stock transaction.

b.Complete the Figure 8-11 worksheet for consolidated financial statements for 2017

?

(Essay)

4.7/5 (30)

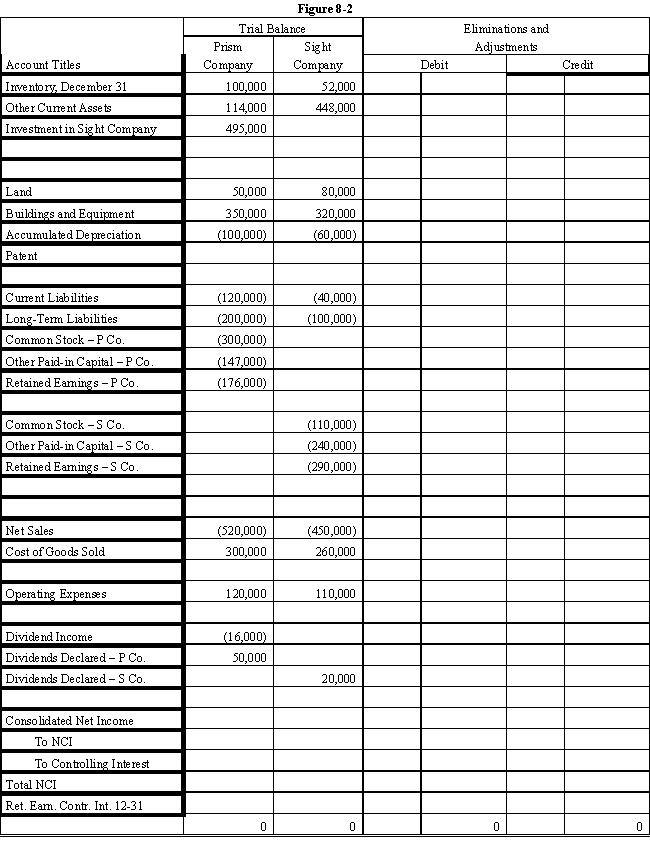

On January 1, 2016, Prism Company purchased 7,500 shares of the common stock of Sight Company for $495,000.On this date, Sight had 20,000 shares of $10 par common stock authorized, 10,000 shares issued and outstanding.Other paid-in capital and retained earnings were $200,000 and $300,000 respectively.On January 1, 2016, any excess of cost over book value is due to a patent, to be amortized over 15 years.

?

Sight's net income and dividends for two years were:

?

?

2016 2017 Net income \ 50,000 \ 80,000 Dividends 10,000 20,000 In November 2016, Sight Company declared a 10% stock dividend at a time when the market price of its common stock was $50 per share.The stock dividend was distributed on December 31, 2016.

?

For both 2016 and 2017, Prism Company has accounted for its investment in Sight using the cost method.

?

During 2016, Sight Company sold goods to Prism Company for $40,000, of which $10,000 was on hand on December 31, 2016.During 2017, Sight sold goods to Prism for $60,000 of which $15,000 was on hand on December 31, 2017.Sight's gross profit on intercompany sales is 40%.

?

Required:

?

Complete the Figure 8-2 worksheet for consolidated financial statements for 2017.

?

?

?

?

(Essay)

4.8/5 (40)

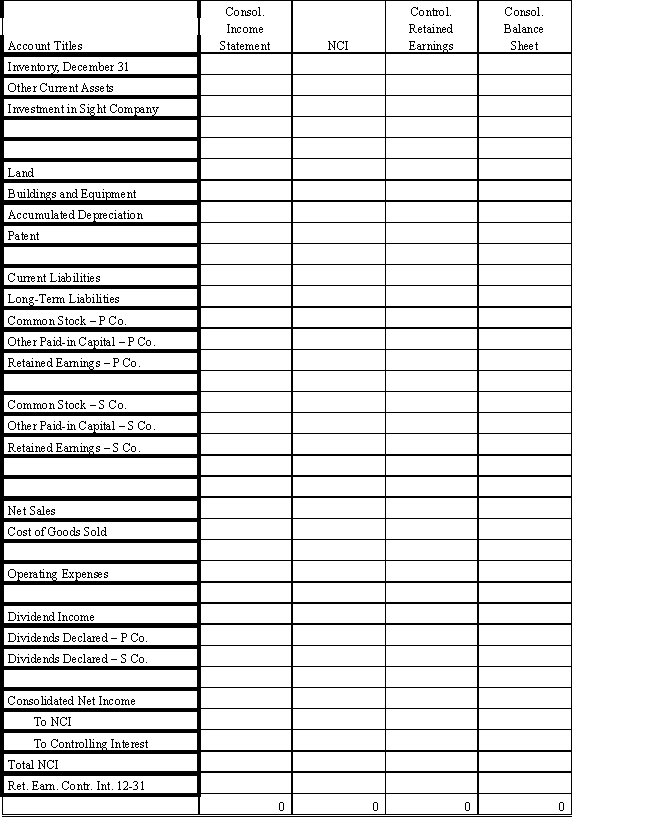

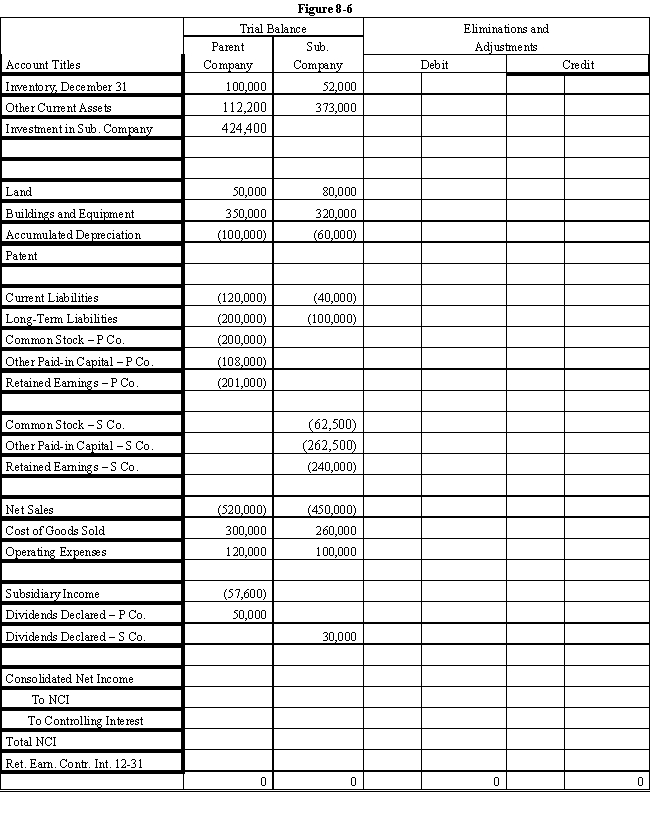

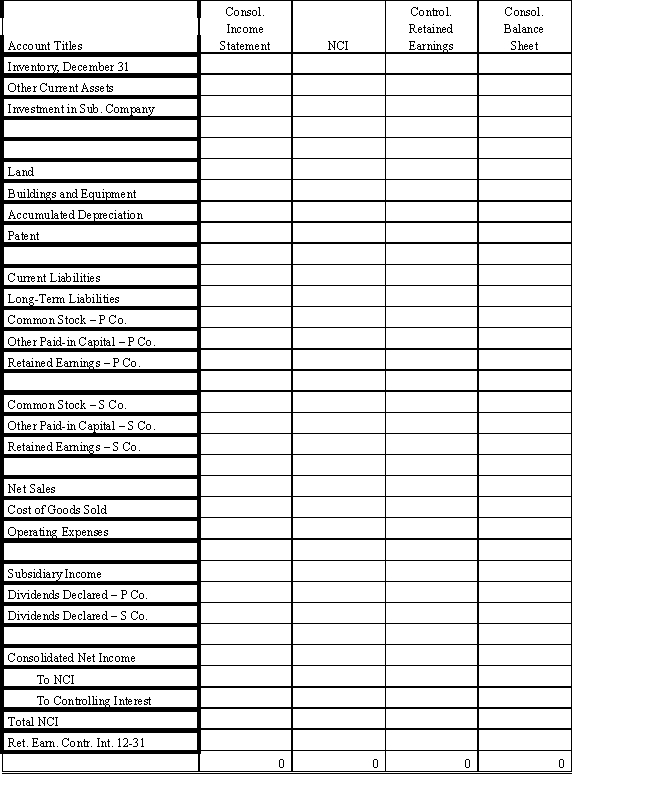

On January 1, 2016, Parent Company purchased 8,000 shares of the common stock of Subsidiary Company for $350,000.On this date, Subsidiary had 20,000 shares of $5 par common stock authorized, 10,000 shares issued and outstanding.Other paid-in capital and retained earnings were $150,000 and $200,000 respectively.On January 1, 2016, any excess of cost over book value is due to a patent, to be amortized over 15 years.Parent Company uses the simple equity method to account for its investment in Sub.

?

Subsidiary's net income and dividends for two years were:

?

?

2016 2017 Net income \ 50,000 \ 90,000 Dividends 10,000 30,000 On January 1, 2017, Subsidiary Company sold an additional 2,500 shares of common stock to non-controlling shareholders for $50 per share.

?

In the last quarter of 2017, Subsidiary Company sold goods to Parent Company for $40,000.Subsidiary's usual gross profit on intercompany sales is 40%.On December 31, $7,500 of these goods are still in Parent's ending inventory.

?

Required:

?

Complete the Figure 8-6 worksheet for consolidated financial statements for 2017.

?

?

(Essay)

4.9/5 (38)

When the parent purchases some newly issued shares of a subsidiary, any adjustments resulting from the subsidiary stock sales should be made

(Multiple Choice)

4.7/5 (40)

A parent company owns a 100% interest in a subsidiary.Recently, the subsidiary paid a 10% stock dividend.The dividend should be recorded on the books of the parent

(Multiple Choice)

4.9/5 (39)

Able Company owns an 80% interest in Barns Company and a 20% interest in Carns Company.Barns owns a 40% interest in Carns Company.

(Multiple Choice)

4.7/5 (46)

When a parent purchases a portion of the newly issued stock of its subsidiary and the parent's percentage of ownership interest remains the same,

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)