Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes

Exam 1: Business Combinations: New Rules for a Long-Standing Business Practice48 Questions

Exam 2: Consolidated Statements: Date of Acquisition44 Questions

Exam 3: Consolidated Statements: Subsequent to Acquisition37 Questions

Exam 4: Intercompany Transactions: Merchandise, Plant Assets, and Notes43 Questions

Exam 5: Intercompany Transactions: Bonds and Leases54 Questions

Exam 6: Cash Flow, Eps, and Taxation48 Questions

Exam 7: Special Issues in Accounting for an Investment in a Subsidiary42 Questions

Exam 8: Subsidiary Equity Transactions, Indirect Subsidiary Ownership, and Subsidiary Ownership of Parent Shares41 Questions

Exam 9: The International Accounting Environment17 Questions

Exam 10: Foreign Currency Transactions75 Questions

Exam 11: Translation of Foreign Financial Statements79 Questions

Exam 12: Interim Reporting and Disclosures About Segments of an Enterprise63 Questions

Exam 13: Partnerships: Characteristics, Formation, and Accounting for Activities36 Questions

Exam 14: Partnerships: Ownership Changes and Liquidations47 Questions

Exam 15: Government and Not for Profit Accounting44 Questions

Exam 16: Governmental Accounting: Other Governmental Funds, Proprietary Funds, and Fiduciary Funds60 Questions

Exam 17: Financial Reporting Issues37 Questions

Exam 18: Accounting for Private Not-For-Profit Organizations61 Questions

Exam 19: Accounting for Not-For-Profit Colleges and Universities and Health Care Organizations83 Questions

Exam 20: Estates and Trusts: Their Nature and the Accountants Role56 Questions

Exam 21: Debt Restructuring, Corporate Reorganizations, and Liquidations49 Questions

Exam 22: Derivatives and Related Accounting Issues60 Questions

Exam 23: Equity Method for Unconsolidated Investments25 Questions

Exam 24: Variable Interest Entities10 Questions

Select questions type

On January 1, 2016, Poe Corp.sold a machine for $900,000 to Saxe Corp., its wholly-owned subsidiary.Poe paid $1,100,000 for this machine.On the sale date, accumulated depreciation was $250,000.Poe estimated a $100,000 salvage value and depreciated the machine on the straight-line method over 20 years, a policy that Saxe continued.In Poe's December 31, 2016, consolidated balance sheet, this machine should be included in cost and accumulated depreciation as

Cost Accumulated Depreciation

(Multiple Choice)

4.7/5  (43)

(43)

This year, Rose Company acquired all of the common stock of Hayley Company.At the end of the current year, balances of selected accounts and other information for each of the companies were as follows: At the end of the year, 50% of the inventory that Rose sold to Hayley remained in Hayley's inventory, and $30,000 of the amount of the sales was unpaid.Rose still owes half of the amount of its purchases to Hayley, but had sold all of the inventory it had acquired from Hayley by the end of the year.

Rose Hayley Sales \ 2,582,000 \ 1,734,000 Accounts receivable 580,000 235,000 Sales to Hayley during year 80,000 Sales to Rose during year 20,000 Gross profit on all sales 25\% 30\%

What is the amount of consolidated sales at the end of the year?

(Multiple Choice)

5.0/5 (32)

Perry, Inc.owns a 90% interest in Brown Corp.During 2016, Brown sold $100,000 in merchandise to Perry at a 30% gross profit.Ten percent of the goods are unsold by Perry at year end.The non-controlling interest will receive what gross profit as a result of these sales?

(Multiple Choice)

4.8/5 (38)

On January 1, 2016, Parent Company acquired 100% of the common stock of Subsidiary Company for $750,000.On this date Subsidiary had total owners' equity of $540,000.

Any excess of cost over book value is attributable to land, undervalued $10,000, and to goodwill.

During 2016 and 2017, Parent has appropriately accounted for its investment in Subsidiary using the simple equity method.

On January 1, 2017, Parent held merchandise acquired from Subsidiary for $10,000.During 2017, Subsidiary sold merchandise to Parent for $100,000, of which $20,000 is held by Parent on December 31, 2017.Subsidiary's usual gross profit on affiliated sales is 40%.

On December 31, 2017, Parent still owes Subsidiary $20,000 for merchandise acquired in December.

On January 1, 2017, Parent sold to Subsidiary some equipment with a cost of $50,000 and a book value of $20,000.The sales price was $40,000.Subsidiary is depreciating the equipment over a five-year life, assuming no salvage value and using the straight-line method.

Required:

Prepare the worksheet eliminations that would be made on the 2017 consolidated worksheet as a result of:

1) the intercompany sale of inventory

2) the intercompany sale of equipment

(Essay)

4.7/5 (30)

On January 1, 2016 Bullock, Inc.sells land to its 80%-owned subsidiary, Humphrey Corporation, at a $20,000 gain.The land is sold by Humphrey to an outside party in 2018.What is the effect of the intercompany sale of land on 2016 consolidated net income?

(Multiple Choice)

4.9/5 (34)

Stroud Corporation is an 80%-owned subsidiary of Pennie, Inc., acquired by Pennie several years ago.On January 1, 2017, Pennie sold land with a book value of $60,000 to Stroud for $90,000.Stroud resold the land to an unrelated party for $100,000 on September 26, 2018.The gain from sale of land that will appear in the consolidated income statements for 2017 and 2018, respectively, is ____.

(Multiple Choice)

4.9/5 (43)

Which of the following intercompany transactions would not require a worksheet elimination in the consolidation process?

(Multiple Choice)

4.9/5 (37)

This year, Rose Company acquired all of the common stock of Hayley Company.At the end of the current year, balances of selected accounts and other information for each of the companies were as follows: At the end of the year, 50% of the inventory that Rose sold to Hayley remained in Hayley's inventory, and $30,000 of the amount of the sales was unpaid.Rose still owes half of the amount of its purchases to Hayley, but had sold all of the inventory it had acquired from Hayley by the end of the year.

Rose Hayley Sales \ 2,582,000 \ 1,734,000 Accounts receivable 580,000 235,000 Sales to Hayley during year 80,000 Sales to Rose during year 20,000 Gross profit on all sales 25\% 30\%

What is the amount of consolidated cost of goods sold at the end of the year?

(Multiple Choice)

4.8/5 (31)

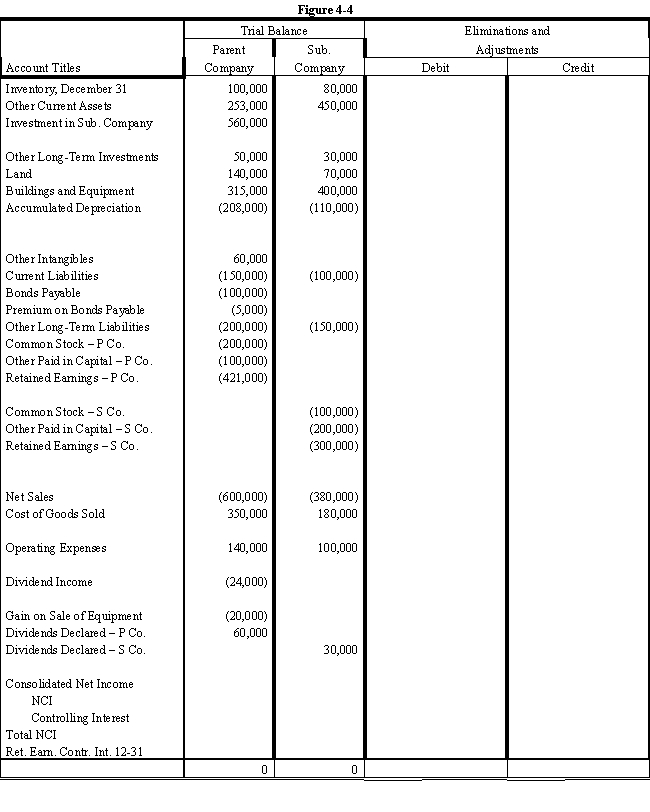

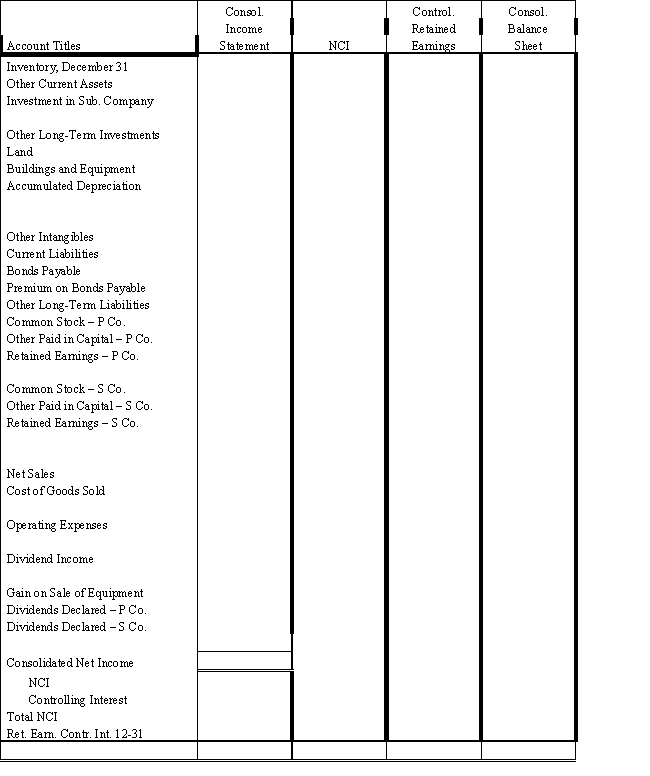

On January 1, 2016, Parent Company acquired 80% of the common stock of Subsidiary Company for $560,000.On this date Subsidiary had total owners' equity of $540,000, including retained earnings of $240,000.During 2016, Subsidiary had net income of $60,000 and paid no dividends.

?

Any excess of cost over book value is attributable to land, undervalued $10,000, and to goodwill.

?

During 2016 and 2017, Parent has appropriately accounted for its investment in Subsidiary using the cost method.

?

On January 1, 2017, Parent held merchandise acquired from Subsidiary for $10,000.During 2017, Subsidiary sold merchandise to Parent for $100,000, of which $20,000 is held by Parent on December 31, 2017.Subsidiary's usual gross profit on affiliated sales is 40%.

?

On December 31, 2017, Parent still owes Subsidiary $20,000 for merchandise acquired in December.

?

On January 1, 2017, Parent sold to Subsidiary some equipment with a cost of $50,000 and a book value of $20,000.The sales price was $40,000.Subsidiary is depreciating the equipment over a five-year life, assuming no salvage value and using the straight-line method.

?

Required:

?

Complete the Figure 4-4 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

(Essay)

5.0/5 (39)

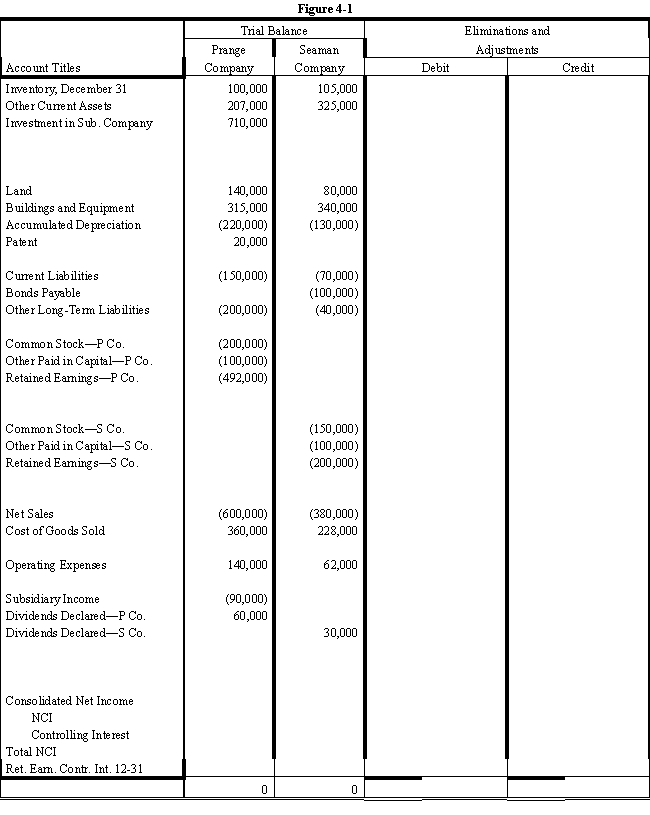

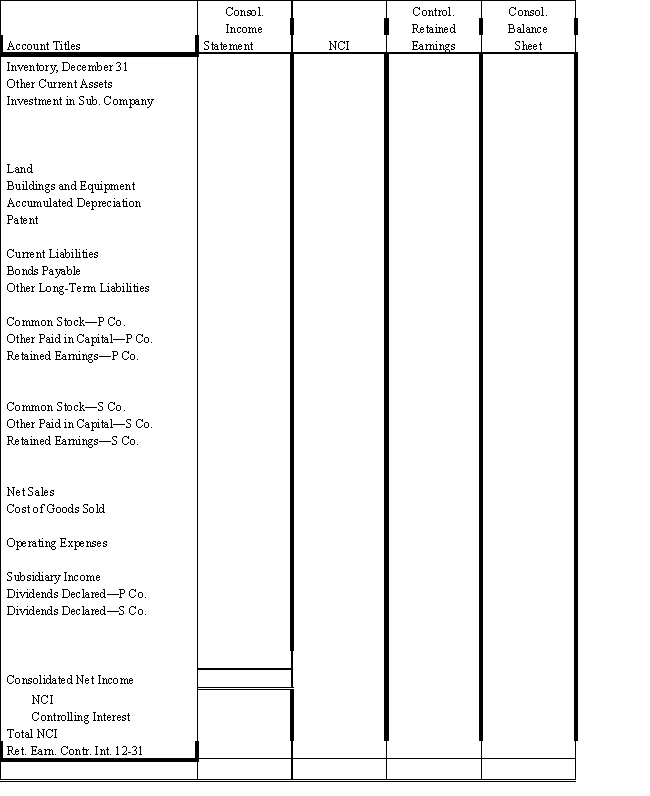

On January 1, 2016, Prange Company acquired 100% of the common stock of Seaman Company for $600,000.On this date Seaman had total owners' equity of $400,000.Any excess of cost over book value is attributable to a patent, which is to be amortized over 10 years.

?

During 2016 and 2017, Prange has appropriately accounted for its investment in Seaman using the simple equity method.

?

On January 1, 2017, Prange held merchandise acquired from Seaman for $30,000.During 2017, Seaman sold merchandise to Prange for $100,000, of which $20,000 is held by Prange on December 31, 2017.Seaman's gross profit on all sales is 40%.

?

On December 31, 2017, Prange still owes Seaman $20,000 for merchandise acquired in December.

?

Required:

?

Complete the Figure 4-1 worksheet for consolidated financial statements for the year ended December 31, 2017.

?

?

?

?

(Essay)

4.9/5 (38)

On 1/1/16 Peck sells a machine with a $20,000 book value to its subsidiary Shea for $30,000.Shea intends to use the machine for 4 years, which was the remaining life that Peck had at the time of the sale.Neither company had assigned a salvage value to the machine.On 12/31/17 Shea sells the machine to an outside party for $14,000.What amount of gain or (loss) for the sale of assets is reported on the consolidated financial statements in 2017?

(Multiple Choice)

4.8/5 (27)

Account balances are as of December 31, 2018 except where noted.

?

?

Additional Information:

?

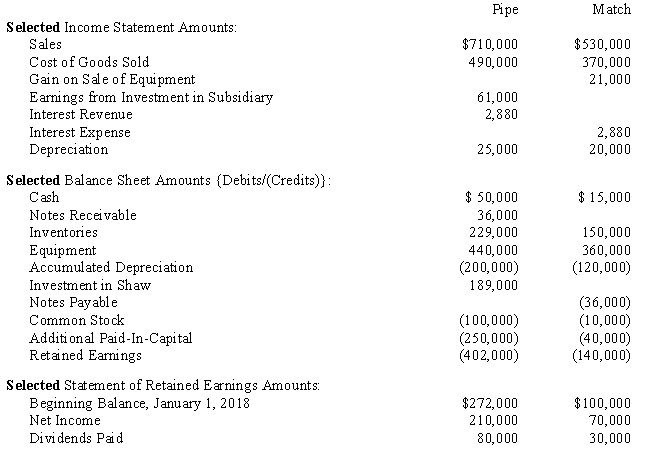

On January 2, 2018 Pipe purchased 90% of Match for $155,000.On that date Match's shareholders' equity equaled $150,000 and the fair values of Match's assets and liabilities equaled their carrying amounts.Excess, if any, is attributed to patents and is amortized over 10 years.

?

On September 4, 2018 Match paid cash dividends of $30,000.

?

On January 3, 2018 Match sold equipment with an original cost of $30,000 and a carrying value of $15,000 to Pipe for $36,000.The equipment had a remaining useful life of 3 years.Straight-line depreciation is used.

?

On January 4, 2018 Match signed an 8% Note Payable.All interest payments were made as of December 31, 2018.

?

During the year Match sold merchandise to Pipe for $60,000, which included a profit of $20,000.At year end 50% of the merchandise remained in Pipe's inventory.

?

Required:

?1.Which method is Pipe using to account for the investment in Match? How do you know?

2.What elimination entry(ies) are associated with the elimination of intercompany profits due to the sale of merchandise?

3.What elimination entry(ies) are necessary with the sale of equipment by Match to Pipe?

4.What elimination entry(ies) are associated with the note to Match? Why are the entry(ies) made?

Additional Information:

?

On January 2, 2018 Pipe purchased 90% of Match for $155,000.On that date Match's shareholders' equity equaled $150,000 and the fair values of Match's assets and liabilities equaled their carrying amounts.Excess, if any, is attributed to patents and is amortized over 10 years.

?

On September 4, 2018 Match paid cash dividends of $30,000.

?

On January 3, 2018 Match sold equipment with an original cost of $30,000 and a carrying value of $15,000 to Pipe for $36,000.The equipment had a remaining useful life of 3 years.Straight-line depreciation is used.

?

On January 4, 2018 Match signed an 8% Note Payable.All interest payments were made as of December 31, 2018.

?

During the year Match sold merchandise to Pipe for $60,000, which included a profit of $20,000.At year end 50% of the merchandise remained in Pipe's inventory.

?

Required:

?1.Which method is Pipe using to account for the investment in Match? How do you know?

2.What elimination entry(ies) are associated with the elimination of intercompany profits due to the sale of merchandise?

3.What elimination entry(ies) are necessary with the sale of equipment by Match to Pipe?

4.What elimination entry(ies) are associated with the note to Match? Why are the entry(ies) made?

(Essay)

4.8/5 (33)

Phelps Co.uses the sophisticated equity method to account for the 80% investment in its subsidiary Shore Corp.At the time of the acquisition, the fair values of the net asset required approximated their book values.Based upon the following information, what amount of income is attributable to the non-controlling interest? Phelps internally generated income: \ 250,000 Shore internally generated income: \ 50,000 Intercompany profit on Shore beginning inventory: \ 10,000 Intercompany profit on Shore ending inventory: \ 15,000

(Multiple Choice)

4.8/5 (49)

On January 1, 2016, Pinto Company purchased an 80% interest in Sands Inc.for $1,000,000.The equity balances of Sands at the time of the purchase were as follows:

?

?

Common stock ( \ 10) \ 100,000 Paid-in capital in excess of par 400,000 Retained earnings 500,000 Any excess of cost over book value is attributable to goodwill.

?

No dividends were paid by either firm during 2016.The following trial balances were prepared for Pinto Company and its subsidiary, Sands Inc., on December 31, 2016:

?

?

Pinto Sands Cash 120,000 70,000 Accounts receivable 240,000 197,000 Inventory 200,000 176,000 Land 600,000 180,000 Buildings and equipment 1,100,000 800,000 Accumulated depreciation (180,000) (120,000) Investment in Sands 1,000,000 Accounts payable (110,000) (50,000) Common stock, \1 0 par (800,000) (100,000) Paid-in capital in excess of par (660,000) (400,000) Retained earnings (1,340,000) (650,000) Sales (600,000) (300,000) Other income (40,000) (15,000) Cost of goods sold 320,000 180,000 Other expenses 150,000 32,000 Total - - Sands sold a machine to Pinto Company for $40,000 on January 1, 2016.The machine cost Sands $50,000, and $25,000 of accumulated depreciation had been recorded as of the sale date.The machine had a 5-year remaining life and no salvage value.Pinto Company is using straight-line depreciation.

?

Since the purchase date, Pinto has sold merchandise for resale to Sands, Inc.at a mark-up on cost of 25%.Sales during 2016 were $150,000.The inventory of these goods held by Sands was $15,000 on January 1, 2016, and $18,000 on December 31, 2016.

?

Required:

?

Prepare a consolidated income statement for 2016, including income distribution schedules to support your distribution of income to the non-controlling and controlling interest interests.

(Essay)

4.8/5 (43)

Patti Corp.has several subsidiaries (Aeta, Beta, and Gaeta) that are included in its consolidated financial statements.In its 12/31/16 separate balance sheet, Patti had the following intercompany balances before eliminations:

Debit Credit Current Receivable due from Aeta \ 40,000 Noncurrent Receivable due from Beta 100,000 Cash Advance to Beta 26,000 Cash Advance from Gaeta \ 75,000 Intercompany Payable to Gaeta 40,000 In its 12/31/16 consolidated balance sheet, what amount should Patti report as intercompany receivables?

(Multiple Choice)

4.9/5 (43)

On January 1, 2016, a parent loaned $30,000 to its 100%-owned subsidiary on a 5-year, 8% note.The note requires a principal payment at the end of each year of $6,000 plus payment of interest accrued to date.The following accounts require adjustment in the consolidation process: ?

Controlling Assets Debt Retained Earnings

A) Yes Yes Yes

B) No No Yes

C) Yes Yes No

D) No No No

(Short Answer)

4.7/5 (36)

For each of the following intercompany transactions, state the principle to be used in accounting for intercompany gains on current and future consolidated income statements:

?

a.Gains on merchandise sales

?

?

b.Gains on the sale of land

?

?

c.Gains on the sale of depreciable fixed assets

?

?

d.Interest on intercompany notes

?

(Essay)

4.9/5 (41)

To consolidate affiliated companies, intercompany sales must be eliminated.Assume that Company P sold merchandise costing $5,000 to a subsidiary Company S, for $5,200.Company S then sells the merchandise to an outside company for $5,600.If the affiliated companies do not eliminate the intercompany sale, the following would occur:

(Multiple Choice)

4.9/5 (36)

The sale of inventory items by a parent company to an affiliated company

(Multiple Choice)

4.8/5 (35)

Company P owns 100% of the common stock of Company S.Company P is constructing an asset for Company S that will be used in Company S's manufacturing operations over a 5-year period.The asset was 50% complete at the end of 2016 and was completed on December 31, 2017.Company P is recording the construction under the percentage of completion method.The asset was put into use by Company S on January 1, 2018.The profit on the asset was estimated to be $50,000.Actual results complied with the estimate.On the consolidated statements, the profit recognized will be ?

?

2016 2017 2018 2019 - 2017

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)