Exam 15: Alternative Minimum Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law195 Questions

Exam 2: Working With the Tax Law86 Questions

Exam 3: Computing the Tax187 Questions

Exam 4: Gross Income: Concepts and Inclusions124 Questions

Exam 5: Gross Income: Exclusions113 Questions

Exam 6: Deductions and Losses: in General146 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses95 Questions

Exam 8: Depreciation, cost Recovery, amortization, and Depletion103 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses181 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions105 Questions

Exam 11: Investor Losses111 Questions

Exam 12: Tax Credits and Payments118 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, basis Considerations, and Nontaxable Exchanges280 Questions

Exam 14: Property Transactions, capital Gains and Losses, sec1231, and Recapture Provisions145 Questions

Exam 15: Alternative Minimum Tax132 Questions

Exam 16: Accounting Periods and Methods91 Questions

Exam 17: Corporations: Introduction and Operating Rules112 Questions

Exam 18: Corporations: Organization and Capital Structure93 Questions

Exam 19: Corporations: Distributions Not in Complete Liquidation192 Questions

Exam 20: Corporations: Distributions in Complete Liquidation and an Overview of Reorganization72 Questions

Exam 21: Partnerships163 Questions

Exam 22: S Corporations145 Questions

Exam 23: Exempt Entities141 Questions

Exam 24: Multistate Corporate Taxation196 Questions

Exam 25: Taxation of International Transactions164 Questions

Exam 26: Tax Practice and Ethics183 Questions

Exam 27: The Federal Gift and Estate Taxes167 Questions

Exam 28: Income Taxation of Trusts and Estates167 Questions

Select questions type

Benita expensed mining exploration and development costs of $500,000 incurred in the current tax year.She will be required to make negative AMT adjustments for each of the next ten years and a positive AMT adjustment in the current tax year.

Free

(True/False)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

False

How can the positive AMT adjustment for research and experimental expenditures be avoided?

Free

(Essay)

4.8/5 (37)

Correct Answer:Verified

For regular income tax purposes,research and experimental expenses can be deducted in the year incurred.For AMT purposes,such expenses must be amortized over a 10-year period.So there will be a positive AMT adjustment in year 1 and negative AMT adjustments in years 2 through 10.

If the taxpayer elects to amortize the research and experimental expenses over a 10-year period for regular income tax purposes,the deductions for regular income tax and AMT will be the same and no AMT adjustments are necessary.

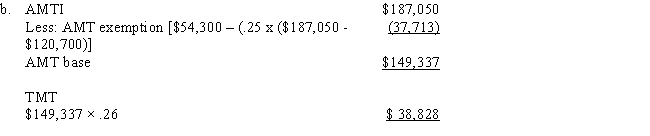

Abigail,who is single,reported taxable income of $115,000 for 2017.She incurred positive AMT adjustments of $30,000,negative AMT adjustments of $12,000,and tax preference items of $50,000.Abigail itemizes deductions.

a.Compute Abigail's AMTI.

a. Compute Abigail's tentative minimum tax (TMT).

b.Assume the same facts as in part

Free

(Essay)

4.7/5 (41)

Correct Answer:Verified

Factors that can cause the adjusted basis for AMT purposes to be different from the adjusted basis for regular income tax purposes include:

(Multiple Choice)

4.8/5 (43)

Keosha acquires used 10-year personal property to use in her business in 2017 and uses MACRS depreciation for regular income tax purposes.As a result,Keosha will incur a positive AMT adjustment in 2017,because AMT depreciation is slower.

(True/False)

4.7/5 (35)

Celia and Christian,who are married filing jointly,have one dependent and do not itemize deductions.They report taxable income of $192,000 and tax preferences of $53,000 in 2017.What is their AMT base for 2017?

(Multiple Choice)

4.8/5 (30)

In 2017,Zachary incurs no AMT adjustments,and his only AMT preference (which is also his only itemized deduction) is $42,000 of state and local and real property taxes.

If Zachary were a single taxpayer who itemized deductions and had taxable income of $95,000,his regular tax liability would be $19,582 and his AMT liability would be $22,555.

Assume instead that Zachary is a married taxpayer filing jointly in 2017.The couple's taxable income amount is changed only by the additional personal exemption.In comparison to the tax liability amounts presented above,the couple's regular and AMT tax liabilities would be:

(Multiple Choice)

4.8/5 (41)

Kay claimed percentage depletion of $119,000 for the current year for regular income tax purposes.Cost depletion would have been $60,000.Her basis in the property was $90,000 at the beginning of the current year.Kay must treat the percentage depletion deducted in excess of cost depletion,or $59,000,as a preference in computing AMTI.

(True/False)

4.7/5 (39)

Wallace owns a construction company that builds both commercial and residential buildings.He contracts to build a residential building for $800,000,and for which he is eligible to use the completed contract method of accounting.In the current year for regular income tax purposes,Wallace does not recognize any gross income on the contract.Under the percentage of completion method,the income recognized under the contract would have been $60,000.Wallace's AMT effect is:

(Multiple Choice)

4.8/5 (37)

Melinda is in the 35% marginal regular tax bracket.She reports a net capital gain of $150,000 on the sale of land which is eligible for the lower tax on net capital gain in calculating the regular income tax.Discuss the tax rate that applies to the $150,000 net capital gain in calculating the tentative minimum tax (TMT) for Melinda.

(Essay)

4.9/5 (38)

Lilly is single and reports zero taxable income for 2017.She incurs positive AMT timing adjustments of $600,000 and AMT exclusions of $200,000.

a.Calculate Lilly's tentative minimum tax (TMT).

b.Calculate Lilly's AMT credit carryover to 2018.

(Essay)

4.9/5 (40)

Negative AMT adjustments for the current year caused by timing differences are offset by the positive AMT adjustments in prior tax years also caused by timing differences.

(True/False)

4.9/5 (37)

Nell records a personal casualty loss deduction of $14,500 for regular income tax purposes.The loss was computed as $26,600,but it was reduced by $100 and by $12,000 (10% × $120,000 AGI).For AMT purposes,the casualty loss deduction also is $14,500.

(True/False)

4.9/5 (38)

Which of the following itemized deductions are allowed in full for AMT purposes?

(Multiple Choice)

4.9/5 (41)

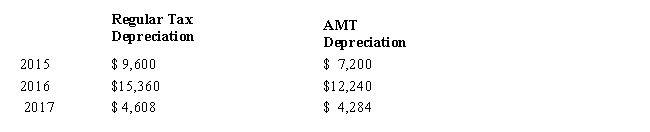

Jesse placed equipment that cost $48,000 in service in 2015 (neither § 179 expensing nor bonus depreciation was elected).On July 1,2017,Jesse sold the equipment for $22,000.

Regular tax and AMT depreciation amounts for the equipment are computed as follows.

What AMT adjustments will be required for the equipment for 2017?

What AMT adjustments will be required for the equipment for 2017?

(Multiple Choice)

5.0/5 (43)

The AMT calculated using the indirect method will produce a different amount than the AMT calculated using the direct method.

(True/False)

4.9/5 (39)

Which of the following statements regarding differences in the corporate and the individual AMT calculation is most correct?

(Multiple Choice)

4.8/5 (41)

Because passive losses are not deductible in computing either taxable income or AMTI,no AMT adjustment for passive losses is required.

(True/False)

4.8/5 (39)

All of a C corporation's AMT is available for carryover as a minimum tax credit,regardless of whether the adjustments and preferences originate from timing differences or AMT preferences.

(True/False)

4.9/5 (38)

Paul incurred circulation expenditures of $180,000 in 2017 and deducted that amount for regular income tax purposes.Paul has a $60,000 negative AMT adjustment for each of 2018,2019,and for 2020.

(True/False)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)