Exam 9: Inventory Costing and Capacity Analysis

Exam 1: The Manager and Management Accounting195 Questions

Exam 2: An Introduction to Cost Terms and Purposes224 Questions

Exam 3: Cost-Volume-Profit Analysis209 Questions

Exam 4: Job Costing203 Questions

Exam 5: Activity-Based Costing and Activity-Based Management176 Questions

Exam 6: Master Budget and Responsibility Accounting226 Questions

Exam 7: Flexible Budgets,direct-Cost Variances,and Management Control181 Questions

Exam 8: Flexible Budgets, overhead Cost Variances, and Management Control171 Questions

Exam 9: Inventory Costing and Capacity Analysis207 Questions

Exam 10: Determining How Costs Behave192 Questions

Exam 11: Decision Making and Relevant Information218 Questions

Exam 12: Strategy,balanced Scorecard,and Strategic Profitability Analysis172 Questions

Exam 13: Pricing Decisions and Cost Management209 Questions

Exam 14: Cost Allocation, customer-Profitability Analysis, and Sales-Variance Analysis167 Questions

Exam 15: Allocation of Support-Department Costs, common Costs, and Revenues150 Questions

Exam 16: Cost Allocation: Joint Products and Byproducts150 Questions

Exam 17: Process Costing149 Questions

Exam 18: Spoilage, rework, and Scrap153 Questions

Exam 19: Balanced Scorecard: Quality and Time150 Questions

Exam 20: Inventory Management, just-In-Time, and Simplified Costing Methods150 Questions

Exam 21: Capital Budgeting and Cost Analysis151 Questions

Exam 22: Management Control Systems, transfer Pricing, and Multinational Considerations150 Questions

Exam 23: Performance Measurement, compensation, and Multinational Considerations150 Questions

Select questions type

Patota Manufacturing incurred the following expenses during 2017:

Fixed manufacturing costs \ 120,000 Fixed nonmanufacturing costs \ 83,000 Unit selling price \ 340 Total unit cost \ 120 Variable manufacturing cost rate \ 60 Units produced 1,390 units

What is the breakeven point in units using absorption costing if the units produced are actually 2,220? (Round your final answer up to the next whole unit. )

(Multiple Choice)

4.8/5  (31)

(31)

The only real challenge in planning and controlling capacity costs is with the denominator as the numerator of a budgeted fixed manufacturing cost allocation rate is rarely the issue.

(True/False)

4.9/5 (32)

Explain how using master-budget capacity utilization for setting prices can lead to a downward demand spiral.

(Essay)

4.8/5 (36)

Ireland Corporation planned to be in operation for three years.

Required:

a.Prepare an income statement for each year using absorption costing.

b.Prepare an income statement for each year using variable costing.

Required:

a.Prepare an income statement for each year using absorption costing.

b.Prepare an income statement for each year using variable costing.

(Essay)

4.8/5 (40)

Which of the following statements is true of contribution-margin format of the income statement?

(Multiple Choice)

4.9/5 (37)

For benchmarking purposes for long-range planning,it is best to use master-budget capacity because all competitors use about the same about of capacity for production.

(True/False)

4.9/5 (44)

Swan Textiles Inc.produces and sells a decorative pillow for $98.00 per unit.In the first month of operation,2,300 units were produced and 1,800 units were sold.Actual fixed costs are the same as the amount budgeted for the month.Other information for the month includes:

Variable manufacturing costs \ 23.00 per unit Variable marketing costs \ 6.00 per unit Fixed manufacturing costs \ 15 per unit Administrative expenses, all fixed \ 21.00 per unit Ending inventories: Direct materials -0- WIP -0- Finished goods 500 units

What is the contribution margin using variable costing?

(Multiple Choice)

4.8/5 (44)

What is throughput costing? What advantages does it have over variable and absorption costing?

(Essay)

4.9/5 (42)

Hyland Resources Inc.uses practical capacity as the denominator to set the cost of supplying capacity and for the current period the budgeted cost per unit of supplying capacity was $44.Practical capacity was set at 14,000 units with theoretical capacity at 20,000 units.During the period,only 11,000 units were produced while the master budget assumed that the company would produce 13,000 units.What is value of the manufacturing resources not used during the period?

(Multiple Choice)

4.9/5 (38)

To reduce the undesirable incentives to build up inventories that absorption costing can create,a number of companies use variable costing for internal reporting.

(True/False)

4.8/5 (33)

Which of the following capacity levels should a company choose,from a long-run product costing perspective,to allocate budgeted fixed manufacturing costs to products?

(Multiple Choice)

4.7/5 (32)

In ________,fixed manufacturing costs are included as inventoriable costs.

(Multiple Choice)

4.8/5 (48)

Kaiser Company just hired its fourth production manager in three years.All three previous managers had quit because they could not get the company above the break-even point,even though sales had increased somewhat each year.The company was operating at about 60 % of plant capacity.The flatware industry was growing,so increased sales were not out of the question.

I.R.Thinking took the job as manager of the production division with a very attractive salary package.After interviewing for the position,he proposed a salary and bonus package that would give him a very small salary but a large bonus if he took the operating income (using absorption costing)above the breakeven point during his very first year.

Required:

What do you think Mr.Thinking had in mind for increasing the company's operating income?

(Essay)

4.8/5 (48)

In planning and control of capacity costs,managers must consider possible capacity measures.Which of the following measures the available supply of capacity in a factory?

(Multiple Choice)

4.8/5 (43)

The use of theoretical capacity results in an unrealistically low fixed manufacturing cost per unit because it is based on ________.

(Multiple Choice)

4.9/5 (22)

Jenkins Corporation sells one product.The following information is available for the current month:

Selling price per unit \ 110 Standard fixed manufacturing costs per unit \ 49 Variable selling and administrative costs per unit \ B Standard variable manufacturing costs per unit \ 3 Fixed selling and administrative costs \ 44,000 Wnits produced 14,800 units Units sold 9,600 units

What is the variable costing breakeven point in units? (Round your final answer up to the next whole unit. )

(Multiple Choice)

4.8/5 (30)

Yellow Mountain Manufacturing factors practical capacity as a denominator to calculate budgeted fixed overhead.Theoretical capacity is 12,000 units per year with practical capacity of 9,000 units per year.Budgeted fixed overhead costs were $690,000 and actual overhead costs were $730,000 with actual output of 8,000 units.Which of the following statements is true?

(Multiple Choice)

4.8/5 (36)

Absorption costing is also referred to as super-variable costing.

(True/False)

4.9/5 (41)

The production-volume variance,which relates only to fixed manufacturing overhead,exists under absorption costing but not under variable costing.

(True/False)

4.8/5 (30)

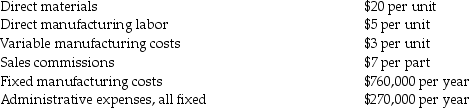

Fast Track Auto produces and sells an auto part for $60 per unit.In 2017,120,000 parts were produced and 75,000 units were sold.Other information for the year includes:

What is the inventoriable cost per unit using variable costing?

What is the inventoriable cost per unit using variable costing?

(Multiple Choice)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)