Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information107 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition122 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership116 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes115 Questions

Exam 8: Segment and Interim Reporting116 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations83 Questions

Exam 14: Partnerships: Formation and Operation88 Questions

Exam 15: Partnerships: Termination and Liquidation73 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments49 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

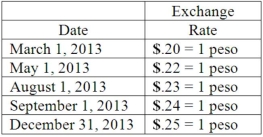

Coyote Corp. (a U.S. company in Texas) had the following series of transactions in a foreign country during 2013:  The appropriate exchange rates during 2013 were as follows:

The appropriate exchange rates during 2013 were as follows:  What amount will Coyote Corp. report in its 2013 balance sheet for Accounts payable?

What amount will Coyote Corp. report in its 2013 balance sheet for Accounts payable?

Free

(Essay)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

Accounts payable ((60,000 - 36,000 pesos) × $.25): $6,000

What happens when a U.S. company sells goods denominated in a foreign currency and the foreign currency appreciates?

Free

(Essay)

4.9/5 (37)

Correct Answer:Verified

The event results in a foreign exchange gain.

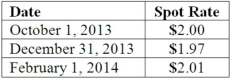

On October 1, 2013, Eagle Company forecasts the purchase of inventory from a British supplier on February 1, 2014, at a price of 100,000 British pounds. On October 1, 2013, Eagle pays $1,800 for a three-month call option on 100,000 pounds with a strike price of $2.00 per pound. The option is considered to be a cash flow hedge of a forecasted foreign currency transaction. On December 31, 2013, the option has a fair value of $1,600. The following spot exchange rates apply:  What is the amount of Cost of Goods Sold for 2014 as a result of these transactions?

What is the amount of Cost of Goods Sold for 2014 as a result of these transactions?

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

C

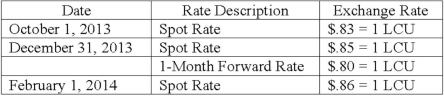

On October 1, 2013, Jarvis Co. sold inventory to a customer in a foreign country, denominated in 100,000 local currency units (LCU). Collection is expected in four months. On October 1, 2013, a forward exchange contract was acquired whereby Jarvis Co. was to pay 100,000 LCU in four months (on February 1, 2014) and receive $78,000 in U.S. dollars. The spot and forward rates for the LCU were as follows:  The company's borrowing rate is 12%. The present value factor for one month is .9901.

Any discount or premium on the contract is amortized using the straight-line method.

Assuming this is a fair value hedge; prepare journal entries for this sales transaction and forward contract.

The company's borrowing rate is 12%. The present value factor for one month is .9901.

Any discount or premium on the contract is amortized using the straight-line method.

Assuming this is a fair value hedge; prepare journal entries for this sales transaction and forward contract.

(Essay)

4.8/5 (37)

All of the following hedges are used for future purchase/sale transactions except

(Multiple Choice)

4.8/5 (34)

Which statement is true regarding a foreign currency option?

(Multiple Choice)

4.8/5 (28)

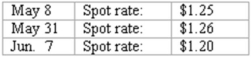

Brisco Bricks purchases raw material from its foreign supplier, Bolivian Clay, on May 8. Payment of 2,000,000 foreign currency units (FC) is due in 30 days. May 31 is Brisco's fiscal year-end. The pertinent exchange rates were as follows:  How much Foreign Exchange Gain or Loss should Brisco record on May 31?

How much Foreign Exchange Gain or Loss should Brisco record on May 31?

(Multiple Choice)

4.8/5 (36)

Primo Inc., a U.S. company, ordered parts costing 100,000 rupee from a foreign supplier on July 7 when the spot rate was $.025 per rupee. A one-month forward contract was signed on that date to purchase 100,000 rupee at a rate of $.027. The forward contract is properly designated as a fair value hedge of the 100,000 rupee firm commitment. On August 7, when the parts are received, the spot rate is $.028. At what amount should the parts inventory be carried on Primo's books?

(Multiple Choice)

4.8/5 (39)

All of the following data may be needed to determine the fair value of a forward contract at any point in time except

(Multiple Choice)

4.8/5 (41)

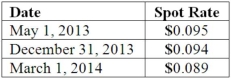

On May 1, 2013, Mosby Company received an order to sell a machine to a customer in Canada at a price of 2,000,000 Mexican pesos. The machine was shipped and payment was received on March 1, 2014. On May 1, 2013, Mosby purchased a put option giving it the right to sell 2,000,000 pesos on March 1, 2014 at a price of $190,000. Mosby properly designates the option as a fair value hedge of the peso firm commitment. The option cost $3,000 and had a fair value of $3,200 on December 31, 2013. The following spot exchange rates apply:  Mosby's incremental borrowing rate is 12 percent, and the present value factor for two months at a 12 percent annual rate is .9803.

What was the impact on Mosby's 2013 net income as a result of this fair value hedge of a firm commitment?

Mosby's incremental borrowing rate is 12 percent, and the present value factor for two months at a 12 percent annual rate is .9803.

What was the impact on Mosby's 2013 net income as a result of this fair value hedge of a firm commitment?

(Multiple Choice)

4.9/5 (37)

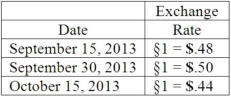

Old Colonial Corp. (a U.S. company) made a sale to a foreign customer on September 15, 2013, for 100,000 stickles. Payment was received on October 15, 2013. The following exchange rates applied:  Required:

Prepare all journal entries for Old Colonial Corp. in connection with this sale assuming that the company closes its books on September 30 to prepare interim financial statements.

Required:

Prepare all journal entries for Old Colonial Corp. in connection with this sale assuming that the company closes its books on September 30 to prepare interim financial statements.

(Essay)

4.9/5 (33)

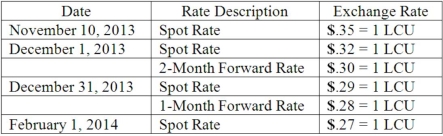

On November 10, 2013, King Co. sold inventory to a customer in a foreign country. King agreed to accept 96,000 local currency units (LCU) in full payment for this inventory. Payment was to be made on February 1, 2014. On December 1, 2013, King entered into a forward exchange contract wherein 96,000 LCU would be delivered to a currency broker in two months. The two month forward exchange rate on that date was 1 LCU = $.30. Any contract discount or premium is amortized using the straight-line method. The spot rates and forward rates on various dates were as follows:  The company's borrowing rate is 12%. The present value factor for one month is .9901.

(A.) Assume this hedge is designated as a fair value hedge. Prepare the journal entries relating to the transaction and the forward contract.

(B.) Compute the effect on 2013 net income.

(C.) Compute the effect on 2014 net income.

The company's borrowing rate is 12%. The present value factor for one month is .9901.

(A.) Assume this hedge is designated as a fair value hedge. Prepare the journal entries relating to the transaction and the forward contract.

(B.) Compute the effect on 2013 net income.

(C.) Compute the effect on 2014 net income.

(Essay)

4.8/5 (33)

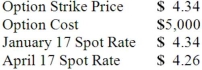

Atherton Inc., a U.S. company, expects to order goods from a foreign supplier at a price of 100,000 lira, with delivery and payment to be made on April 17. On January 17, Atherton purchased a three-month call option on 100,000 lira and designated this option as a cash flow hedge of a forecasted foreign currency transaction. The following exchange rates apply:  What amount will Atherton include as an option expense in net income for the period January 17 to April 17?

What amount will Atherton include as an option expense in net income for the period January 17 to April 17?

(Multiple Choice)

4.7/5 (43)

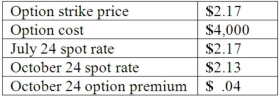

Woolsey Corporation, a U.S. company, expects to sell goods to a British customer at a price of 250,000 pounds, with delivery and payment to be made on October 24. On July 24, Woolsey purchased a three-month put option for 250,000 British pounds and designated this option as a cash flow hedge of a forecasted foreign currency transaction expected to be completed in late October. The following exchange rates apply:  What amount will Woolsey include as an option expense in net income for the period July 24 to October 24?

What amount will Woolsey include as an option expense in net income for the period July 24 to October 24?

(Multiple Choice)

4.8/5 (37)

Larson Company, a U.S. company, has an India rupee account receivable resulting from an export sale on September 7 to a customer in India. Larson signed a forward contract on September 7 to sell rupees and designated it as a cash flow hedge of a recognized receivable. The spot rate was $.023, and the forward rate was $.021. Which of the following did the U.S. exporter report in net income?

(Multiple Choice)

4.7/5 (41)

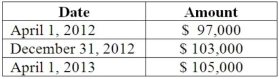

On April 1, 2012, Shannon Company, a U.S. company, borrowed 100,000 euros from a foreign bank by signing an interest-bearing note due April 1, 2013. The dollar value of the loan was as follows:  How much foreign exchange gain or loss should be included in Shannon's 2013 income statement?

How much foreign exchange gain or loss should be included in Shannon's 2013 income statement?

(Multiple Choice)

4.8/5 (40)

On October 1, 2013, Jarvis Co. sold inventory to a customer in a foreign country, denominated in 100,000 local currency units (LCU). Collection is expected in four months. On October 1, 2013, a forward exchange contract was acquired whereby Jarvis Co. was to pay 100,000 LCU in four months (on February 1, 2014) and receive $78,000 in U.S. dollars. The spot and forward rates for the LCU were as follows: ![On October 1, 2013, Jarvis Co. sold inventory to a customer in a foreign country, denominated in 100,000 local currency units (LCU). Collection is expected in four months. On October 1, 2013, a forward exchange contract was acquired whereby Jarvis Co. was to pay 100,000 LCU in four months (on February 1, 2014) and receive $78,000 in U.S. dollars. The spot and forward rates for the LCU were as follows: The company's borrowing rate is 12%. The present value factor for one month is .9901. Any discount or premium on the contract is amortized using the straight-line method. Assuming this is a cash flow hedge; prepare journal entries for this sales transaction and forward contract. <sup>1</sup> [(.80 - .78) 100,000] × .9901 = 1,980 <sup>2</sup> [(.78 - .86) 100,000] - 1,980 = 6,020](https://storage.examlex.com/TB2311/11ea8e0c_b123_da95_b636_dba095e4ec25_TB2311_00_TB2311_00.jpg) The company's borrowing rate is 12%. The present value factor for one month is .9901.

Any discount or premium on the contract is amortized using the straight-line method.

Assuming this is a cash flow hedge; prepare journal entries for this sales transaction and forward contract.

The company's borrowing rate is 12%. The present value factor for one month is .9901.

Any discount or premium on the contract is amortized using the straight-line method.

Assuming this is a cash flow hedge; prepare journal entries for this sales transaction and forward contract. ![On October 1, 2013, Jarvis Co. sold inventory to a customer in a foreign country, denominated in 100,000 local currency units (LCU). Collection is expected in four months. On October 1, 2013, a forward exchange contract was acquired whereby Jarvis Co. was to pay 100,000 LCU in four months (on February 1, 2014) and receive $78,000 in U.S. dollars. The spot and forward rates for the LCU were as follows: The company's borrowing rate is 12%. The present value factor for one month is .9901. Any discount or premium on the contract is amortized using the straight-line method. Assuming this is a cash flow hedge; prepare journal entries for this sales transaction and forward contract. <sup>1</sup> [(.80 - .78) 100,000] × .9901 = 1,980 <sup>2</sup> [(.78 - .86) 100,000] - 1,980 = 6,020](https://storage.examlex.com/TB2311/11ea8e0c_b123_da96_b636_17536aa2c56b_TB2311_00_TB2311_00.jpg) 1 [(.80 - .78) 100,000] × .9901 = 1,980

2 [(.78 - .86) 100,000] - 1,980 = 6,020

1 [(.80 - .78) 100,000] × .9901 = 1,980

2 [(.78 - .86) 100,000] - 1,980 = 6,020

(Essay)

4.9/5 (29)

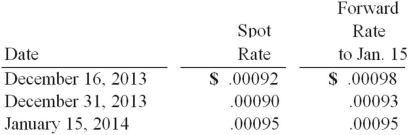

Car Corp. (a U.S.-based company) sold parts to a Korean customer on December 16, 2013, with payment of 10 million Korean won to be received on January 15, 2014. The following exchange rates applied:  Assuming a forward contract was not entered into, what would be the net impact on Car Corp.'s 2013 income statement related to this transaction?

Assuming a forward contract was not entered into, what would be the net impact on Car Corp.'s 2013 income statement related to this transaction?

(Multiple Choice)

4.7/5 (29)

On November 10, 2013, King Co. sold inventory to a customer in a foreign country. King agreed to accept 96,000 local currency units (LCU) in full payment for this inventory. Payment was to be made on February 1, 2014. On December 1, 2013, King entered into a forward exchange contract wherein 96,000 LCU would be delivered to a currency broker in two months. The two month forward exchange rate on that date was 1 LCU = $.30. Any contract discount or premium is amortized using the straight-line method. The spot rates and forward rates on various dates were as follows: ![On November 10, 2013, King Co. sold inventory to a customer in a foreign country. King agreed to accept 96,000 local currency units (LCU) in full payment for this inventory. Payment was to be made on February 1, 2014. On December 1, 2013, King entered into a forward exchange contract wherein 96,000 LCU would be delivered to a currency broker in two months. The two month forward exchange rate on that date was 1 LCU = $.30. Any contract discount or premium is amortized using the straight-line method. The spot rates and forward rates on various dates were as follows: The company's borrowing rate is 12%. The present value factor for one month is .9901. (A.) Assume this hedge is designated as a cash flow hedge. Prepare the journal entries relating to the transaction and the forward contract. (B.) Compute the effect on 2013 net income. (C.) Compute the effect on 2014 net income. <sup>1</sup> [(.30 - .28) 96,000] × .9901 = 1,901 <sup>2</sup> [(.30 - .27) 96,000] = 2,880 - 1,901 = 979](https://storage.examlex.com/TB2311/11ea8e0c_b123_8c6e_b636_77a555881567_TB2311_00_TB2311_00.jpg) The company's borrowing rate is 12%. The present value factor for one month is .9901.

(A.) Assume this hedge is designated as a cash flow hedge. Prepare the journal entries relating to the transaction and the forward contract.

(B.) Compute the effect on 2013 net income.

(C.) Compute the effect on 2014 net income.

The company's borrowing rate is 12%. The present value factor for one month is .9901.

(A.) Assume this hedge is designated as a cash flow hedge. Prepare the journal entries relating to the transaction and the forward contract.

(B.) Compute the effect on 2013 net income.

(C.) Compute the effect on 2014 net income. ![On November 10, 2013, King Co. sold inventory to a customer in a foreign country. King agreed to accept 96,000 local currency units (LCU) in full payment for this inventory. Payment was to be made on February 1, 2014. On December 1, 2013, King entered into a forward exchange contract wherein 96,000 LCU would be delivered to a currency broker in two months. The two month forward exchange rate on that date was 1 LCU = $.30. Any contract discount or premium is amortized using the straight-line method. The spot rates and forward rates on various dates were as follows: The company's borrowing rate is 12%. The present value factor for one month is .9901. (A.) Assume this hedge is designated as a cash flow hedge. Prepare the journal entries relating to the transaction and the forward contract. (B.) Compute the effect on 2013 net income. (C.) Compute the effect on 2014 net income. <sup>1</sup> [(.30 - .28) 96,000] × .9901 = 1,901 <sup>2</sup> [(.30 - .27) 96,000] = 2,880 - 1,901 = 979](https://storage.examlex.com/TB2311/11ea8e0c_b123_8c6f_b636_c528b1edbb03_TB2311_00_TB2311_00.jpg) 1 [(.30 - .28) 96,000] × .9901 = 1,901

2 [(.30 - .27) 96,000] = 2,880 - 1,901 = 979

1 [(.30 - .28) 96,000] × .9901 = 1,901

2 [(.30 - .27) 96,000] = 2,880 - 1,901 = 979

(Essay)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)