Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information107 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition122 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership116 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes115 Questions

Exam 8: Segment and Interim Reporting116 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations83 Questions

Exam 14: Partnerships: Formation and Operation88 Questions

Exam 15: Partnerships: Termination and Liquidation73 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments49 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

The accounting problems encountered in consolidated intra-entity debt transactions when the debt is acquired by an affiliate from an outside party include all of the following except:

Free

(Multiple Choice)

4.9/5  (37)

(37)

Correct Answer: Verified

Verified

C

Knight Co. owned 80% of the common stock of Stoop Co. Stoop had 50,000 shares of $5 par value common stock and 2,000 shares of preferred stock outstanding. Each preferred share received an annual per share dividend of $10 and is convertible into four shares of common stock. Knight did not own any of Stoop's preferred stock. Stoop also had 600 bonds outstanding, each of which is convertible into ten shares of common stock. Stoop's annual after-tax interest expense for the bonds was $22,000. Knight did not own any of Stoop's bonds. Stoop reported income of $300,000 for 2013.

Stoop's diluted earnings per share (rounded) is calculated to be

Free

(Multiple Choice)

4.9/5 (42)

Correct Answer:Verified

D

Which of the following characteristics is not indicative of an enterprise qualifying as a primary beneficiary with a controlling financial interest in a variable interest entity?

Free

(Multiple Choice)

4.8/5 (32)

Correct Answer:Verified

D

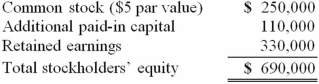

Panton, Inc. acquired 18,000 shares of Glotfelty Corp. several years ago. At the present time, Glotfelty is reporting the following stockholders' equity:  Glotfelty issues 5,000 shares of previously unissued stock to the public for $40 per share. None of this stock is purchased by Panton.

Prepare Panton's journal entry to recognize the impact of this transaction.

Glotfelty issues 5,000 shares of previously unissued stock to the public for $40 per share. None of this stock is purchased by Panton.

Prepare Panton's journal entry to recognize the impact of this transaction.

(Essay)

4.9/5 (46)

A parent company owns a 70 percent interest in a subsidiary whose stock has a book value of $27 per share. The last day of the year, the subsidiary issues new shares for $27 per share, and the parent buys its 70 percent interest in the new shares. Which of the following statements is true?

(Multiple Choice)

4.8/5 (32)

How do subsidiary stock warrants outstanding affect consolidated earnings per share?

(Multiple Choice)

4.8/5 (39)

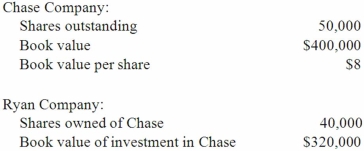

Ryan Company owns 80% of Chase Company. The original balances presented for Ryan and Chase as of January 1, 2013, are as follows:  Assume Chase issues 30,000 additional shares common stock solely to Ryan for $12 per share.

What is the adjusted book value of Chase Company after the issuance of the shares?

Assume Chase issues 30,000 additional shares common stock solely to Ryan for $12 per share.

What is the adjusted book value of Chase Company after the issuance of the shares?

(Multiple Choice)

4.9/5 (36)

Which of the following statements is false regarding the assignment of a gain or loss on intercompany bond transfer?

(Multiple Choice)

4.8/5 (37)

The following information has been taken from the consolidation worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1)) Graham reports a loss on sale of land of $5,000. The land cost Graham $20,000.

(2)) Non-controlling interest in Stage's net income was $30,000.

(3)) Graham paid dividends of $15,000.

(4)) Stage paid dividends of $10,000.

(5)) Excess acquisition-date fair value over book value was expensed by $6,000.

(6)) Consolidated accounts receivable decreased by $8,000.

(7)) Consolidated accounts payable decreased by $7,000.

How will dividends be reported in consolidated statement of cash flows?

(Multiple Choice)

4.9/5 (28)

Goehring, Inc. owns 70 percent of Harry Corp. The consolidated income statement for a year reports $40,000 Non-controlling Interest in Harry Corp.'s Income. Harry paid dividends in the amount of $100,000 for the year. What are the effects of these transactions in the consolidated statement of cash flows for the year?

(Multiple Choice)

4.9/5 (30)

Wolff Corporation owns 70 percent of the outstanding stock of Donald, Inc. During the current year, Donald made $75,000 in sales to Wolff. How does this transfer affect the consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (33)

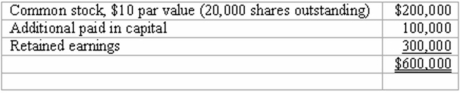

On January 1, 2013, Riney Co. owned 80% of the common stock of Garvin Co. On that date, Garvin's stockholders' equity accounts had the following balances:  The balance in Riney's Investment in Garvin Co. account was $552,000, and the non-controlling interest was $138,000. On January 1, 2013, Garvin Co. sold 10,000 shares of previously unissued common stock for $15 per share. Riney did not acquire any of these shares.

What is the balance in Non-controlling Interest in Garvin Co. after the sale of the 10,000 shares of common stock?

The balance in Riney's Investment in Garvin Co. account was $552,000, and the non-controlling interest was $138,000. On January 1, 2013, Garvin Co. sold 10,000 shares of previously unissued common stock for $15 per share. Riney did not acquire any of these shares.

What is the balance in Non-controlling Interest in Garvin Co. after the sale of the 10,000 shares of common stock?

(Multiple Choice)

4.7/5 (40)

When a company has preferred stock in its capital structure, what amount should be used to calculate non-controlling interest in the preferred stock of the subsidiary when the company is acquired as a subsidiary of another company?

(Essay)

4.8/5 (31)

Panton, Inc. acquired 18,000 shares of Glotfelty Corp. several years ago. At the present time, Glotfelty is reporting the following stockholders' equity:  Glotfelty issues 5,000 shares of previously unissued stock to the public for $27 per share. None of this stock is purchased by Panton.

Describe how this transaction would affect Panton's books.

Glotfelty issues 5,000 shares of previously unissued stock to the public for $27 per share. None of this stock is purchased by Panton.

Describe how this transaction would affect Panton's books.

(Essay)

4.7/5 (39)

How are intra-entity inventory transfers treated on the consolidation worksheet and how are they reflected in a consolidated statement of cash flows?

(Essay)

5.0/5 (30)

Where do dividends paid to the non-controlling interest of a subsidiary appear on a consolidated statement of cash flows?

(Multiple Choice)

4.9/5 (40)

Parent Corporation acquired some of its subsidiary's bonds on the open bond market, paying a price $40,000 higher than the bonds' carrying value. How should the difference between the purchase price and the carrying value be accounted for?

(Essay)

4.7/5 (42)

Panton, Inc. acquired 18,000 shares of Glotfelty Corp. several years ago. At the present time, Glotfelty is reporting the following stockholders' equity:  Glotfelty issues 5,000 shares of previously unissued stock to Panton for $35 per share.

Required: Describe how this transaction would affect Panton's books.

The investment price is above the book value of the subsidiary. In this case, however, the additional amount has been paid by the parent company, not by an outside party. Because the payment is made by Panton, the investment account will need an adjustment after recording the cost of the new shares. A change in ownership is accounted for as an equity transaction when controlling interest is retained.

Glotfelty issues 5,000 shares of previously unissued stock to Panton for $35 per share.

Required: Describe how this transaction would affect Panton's books.

The investment price is above the book value of the subsidiary. In this case, however, the additional amount has been paid by the parent company, not by an outside party. Because the payment is made by Panton, the investment account will need an adjustment after recording the cost of the new shares. A change in ownership is accounted for as an equity transaction when controlling interest is retained.

(Essay)

4.9/5 (44)

Where do dividends paid by a subsidiary to the parent company appear in a consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (43)

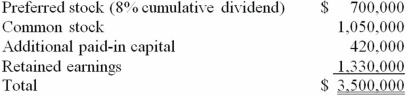

Skipen Corp. had the following stockholders' equity accounts:  The preferred stock was participating and is therefore considered to be equity. Vestin Corp. acquired 90% of this common stock for $2,250,000 and 70% of the preferred stock for $1,120,000. All of the subsidiary's assets and liabilities were determined to have fair values equal to their book values except for land which is undervalued by $130,000.

Required:

What amount was attributed to goodwill on the date of acquisition?

The preferred stock was participating and is therefore considered to be equity. Vestin Corp. acquired 90% of this common stock for $2,250,000 and 70% of the preferred stock for $1,120,000. All of the subsidiary's assets and liabilities were determined to have fair values equal to their book values except for land which is undervalued by $130,000.

Required:

What amount was attributed to goodwill on the date of acquisition?

(Essay)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)