Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information107 Questions

Exam 3: Consolidations - Subsequent to the Date of Acquisition122 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership116 Questions

Exam 5: Consolidated Financial Statements Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income Taxes115 Questions

Exam 8: Segment and Interim Reporting116 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Accounting Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations83 Questions

Exam 14: Partnerships: Formation and Operation88 Questions

Exam 15: Partnerships: Termination and Liquidation73 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments49 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

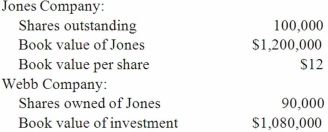

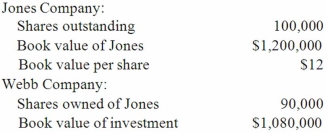

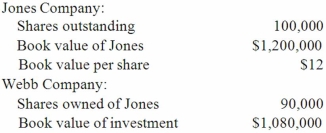

Webb Company owns 90% of Jones Company. The original balances presented for Jones and Webb as of January 1, 2013, are as follows:  Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.

What adjustment is needed for Webb's investment in Jones account?

Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.

What adjustment is needed for Webb's investment in Jones account?

(Multiple Choice)

4.7/5  (45)

(45)

Parent Corporation loaned money to its subsidiary with a five-year note at the market interest rate. How would the note be accounted for in the consolidation process?

(Essay)

4.8/5 (41)

Which of the following statements is true concerning variable interest entities (VIEs)?

1) The role of the VIE equity investors can be fairly minor.

2) A VIE may be created specifically to benefit its sponsoring firm with low-cost financing.

3) VIE governing agreements often limit activities and decision making.

4) VIEs usually have a well-defined and limited business activity.

(Multiple Choice)

4.8/5 (44)

The following information has been taken from the consolidation worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1)) Graham reports a loss on sale of land of $5,000. The land cost Graham $20,000.

(2)) Non-controlling interest in Stage's net income was $30,000.

(3)) Graham paid dividends of $15,000.

(4)) Stage paid dividends of $10,000.

(5)) Excess acquisition-date fair value over book value was expensed by $6,000.

(6)) Consolidated accounts receivable decreased by $8,000.

(7)) Consolidated accounts payable decreased by $7,000.

Using the indirect method, where does the decrease in accounts receivable appear in a consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (38)

Danbers Co. owned seventy-five percent of the common stock of Renz Corp. How does the issuance of a five percent stock dividend by Renz affect Danbers and the consolidation process?

(Essay)

4.8/5 (26)

Webb Company owns 90% of Jones Company. The original balances presented for Jones and Webb as of January 1, 2013, are as follows:  Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.

What is the adjusted book value of Jones after the sale of the shares?

Jones sells 20,000 shares of previously unissued shares of its common stock to outside parties for $10 per share.

What is the adjusted book value of Jones after the sale of the shares?

(Multiple Choice)

4.8/5 (43)

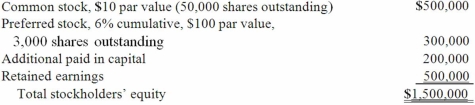

A company had common stock with a total par value of $18,000,000 and fair value of $62,000,000; and 7% preferred stock with a total par value of $6,000,000 and a fair value of $8,000,000. The book value of the company was $85,000,000. If 90% of this company's total equity was acquired by another, what portion of the value would be assigned to the non-controlling interest?

(Multiple Choice)

4.9/5 (37)

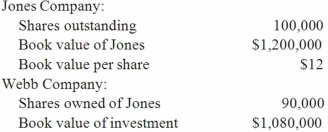

Ryan Company owns 80% of Chase Company. The original balances presented for Ryan and Chase as of January 1, 2013 are as follows:  Assume Chase reacquired 8,000 shares of its common stock from outsiders at $10 per share.

What is Ryan's percent ownership in Chase after the acquisition of the treasury shares (rounded)?

Assume Chase reacquired 8,000 shares of its common stock from outsiders at $10 per share.

What is Ryan's percent ownership in Chase after the acquisition of the treasury shares (rounded)?

(Multiple Choice)

4.9/5 (46)

A parent acquires 70% of a subsidiary's common stock and 60 percent of its preferred stock. The preferred stock is noncumulative. The current year's dividend was paid. How is the non-controlling interest in the subsidiary's net income assigned?

(Multiple Choice)

4.7/5 (31)

On January 1, 2013, Nichols Company acquired 80% of Smith Company's common stock and 40% of its non-voting, cumulative preferred stock. The consideration transferred by Nichols was $1,200,000 for the common and $124,000 for the preferred. Any excess acquisition-date fair value over book value is considered goodwill. The capital structure of Smith immediately prior to the acquisition is:  Compute the goodwill recognized in consolidation.

Compute the goodwill recognized in consolidation.

(Multiple Choice)

4.7/5 (42)

On January 1, 2013, Harrison Corporation spent $2,600,000 to acquire control over Involved, Inc. This price was based on paying $750,000 for 30 percent of Involved's preferred stock, and $1,850,000 for 80 percent of its outstanding common stock. As of the date of the acquisition, Involved's stockholders' equity accounts were as follows:  Assuming Involved's accounts are correctly valued within the company's financial statements, what amount of goodwill should be recognized for the Investment in Involved?

Assuming Involved's accounts are correctly valued within the company's financial statements, what amount of goodwill should be recognized for the Investment in Involved?

(Multiple Choice)

4.9/5 (31)

Webb Company owns 90% of Jones Company. The original balances presented for Jones and Webb as of January 1, 2013 are as follows:  Assume Jones issues 20,000 new shares of its common stock for $15 per share. Of this total, Webb acquires 18,000 shares to maintain its 90% interest in Jones.

What is the adjusted book value of Jones after the stock issuance?

Assume Jones issues 20,000 new shares of its common stock for $15 per share. Of this total, Webb acquires 18,000 shares to maintain its 90% interest in Jones.

What is the adjusted book value of Jones after the stock issuance?

(Multiple Choice)

4.9/5 (37)

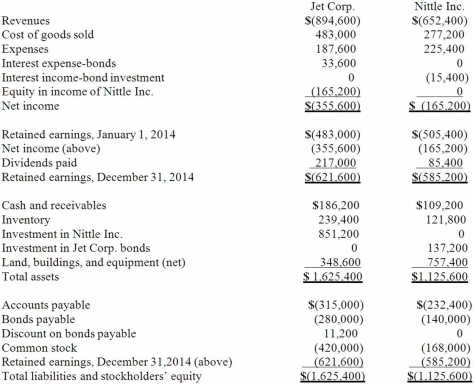

Jet Corp. acquired all of the outstanding shares of Nittle Inc. on January 1, 2011, for $644,000 in cash. Of this price, $42,000 was attributed to equipment with a ten-year remaining useful life. Goodwill of $56,000 had also been identified. Jet applied the partial equity method so that income would be accrued each period based solely on the earnings reported by the subsidiary.

On January 1, 2014, Jet reported $280,000 in bonds outstanding with a book value of $263,200. Nittle purchased half of these bonds on the open market for $135,800.

During 2014, Jet began to sell merchandise to Nittle. During that year, inventory costing $112,000 was transferred at a price of $140,000. All but $14,000 (at Jet's selling price) of these goods were resold to outside parties by year's end. Nittle still owed $50,400 for inventory shipped from Jet during December.

The following financial figures were for the two companies for the year ended December 31, 2014.  Required:

Prepare a consolidation worksheet for the year ended December 31, 2014.

Required:

Prepare a consolidation worksheet for the year ended December 31, 2014.

(Essay)

4.9/5 (36)

The following information has been taken from the consolidation worksheet of Graham Company and its 80% owned subsidiary, Stage Company.

(1)) Graham reports a loss on sale of land of $5,000. The land cost Graham $20,000.

(2)) Non-controlling interest in Stage's net income was $30,000.

(3)) Graham paid dividends of $15,000.

(4)) Stage paid dividends of $10,000.

(5)) Excess acquisition-date fair value over book value was expensed by $6,000.

(6)) Consolidated accounts receivable decreased by $8,000.

(7)) Consolidated accounts payable decreased by $7,000.

Using the indirect method, where does the decrease in accounts payable appear in a consolidated statement of cash flows?

(Multiple Choice)

4.8/5 (38)

How does the existence of a non-controlling interest affect the preparation of a consolidated statement of cash flows?

(Essay)

4.8/5 (36)

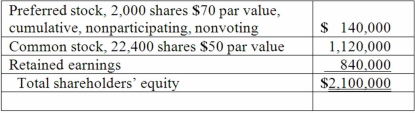

Thomas Inc. had the following stockholders' equity accounts as of January 1, 2013:  Kuried Co. acquired all of the voting common stock of Thomas on January 1, 2013, for $20,656,000. The preferred stock remained in the hands of outside parties and had a fair value of $3,060,000. A database valued at $656,000 was recognized and amortized over five years.

During 2013, Thomas reported earning $630,000 in net income and paid $504,000 in total cash dividends. Kuried used the equity method to account for this investment.

What is the amount of goodwill resulting from this acquisition?

Kuried Co. acquired all of the voting common stock of Thomas on January 1, 2013, for $20,656,000. The preferred stock remained in the hands of outside parties and had a fair value of $3,060,000. A database valued at $656,000 was recognized and amortized over five years.

During 2013, Thomas reported earning $630,000 in net income and paid $504,000 in total cash dividends. Kuried used the equity method to account for this investment.

What is the amount of goodwill resulting from this acquisition?

(Essay)

4.9/5 (35)

Knight Co. owned 80% of the common stock of Stoop Co. Stoop had 50,000 shares of $5 par value common stock and 2,000 shares of preferred stock outstanding. Each preferred share received an annual per share dividend of $10 and is convertible into four shares of common stock. Knight did not own any of Stoop's preferred stock. Stoop also had 600 bonds outstanding, each of which is convertible into ten shares of common stock. Stoop's annual after-tax interest expense for the bonds was $22,000. Knight did not own any of Stoop's bonds. Stoop reported income of $300,000 for 2013.

What was the amount of Stoop's earnings that should be included in calculating consolidated diluted earnings per share?

(Multiple Choice)

4.8/5 (32)

Allen Co. held 80% of the common stock of Brewer Inc. and 40% of this subsidiary's convertible bonds. The following consolidated financial statements were for 2012 and 2013.  Additional Information:

1. Bonds were issued during 2013 by the parent for cash.

2. Amortization of a database acquired in the original combination amounted to $7,000 per year.

3. A building with a cost of $84,000 but a $42,000 book value was sold by the parent for cash on May 11, 2013.

4. Equipment was purchased by the subsidiary on July 23, 2013, using cash.

5. Late in November 2013, the parent issued common stock for cash.

6. During 2013, the subsidiary paid dividends of $14,000.

Required:

Prepare a consolidated statement of cash flows for this business combination for the year ending December 31, 2013. Either the direct method or the indirect method may be used.

Additional Information:

1. Bonds were issued during 2013 by the parent for cash.

2. Amortization of a database acquired in the original combination amounted to $7,000 per year.

3. A building with a cost of $84,000 but a $42,000 book value was sold by the parent for cash on May 11, 2013.

4. Equipment was purchased by the subsidiary on July 23, 2013, using cash.

5. Late in November 2013, the parent issued common stock for cash.

6. During 2013, the subsidiary paid dividends of $14,000.

Required:

Prepare a consolidated statement of cash flows for this business combination for the year ending December 31, 2013. Either the direct method or the indirect method may be used.

(Essay)

4.9/5 (39)

On January 1, 2013, Bast Co. had a net book value of $2,100,000 as follows:  Fisher Co. acquired all of the outstanding preferred shares for $148,000 and 60% of the common stock for $1,281,000. Fisher believed that one of Bast's buildings, with a twelve-year life, was undervalued on the company's financial records by $70,000.

Required:

What is the amount of goodwill to be recognized from this purchase?

Fisher Co. acquired all of the outstanding preferred shares for $148,000 and 60% of the common stock for $1,281,000. Fisher believed that one of Bast's buildings, with a twelve-year life, was undervalued on the company's financial records by $70,000.

Required:

What is the amount of goodwill to be recognized from this purchase?

(Essay)

4.8/5 (33)

Webb Company owns 90% of Jones Company. The original balances presented for Jones and Webb as of January 1, 2013 are as follows:  Assume Jones issues 20,000 new shares of its common stock for $15 per share. Of this total, Webb acquires 18,000 shares to maintain its 90% interest in Jones.

After acquiring the additional shares, what adjustment is needed for Webb's investment in Jones account?

Assume Jones issues 20,000 new shares of its common stock for $15 per share. Of this total, Webb acquires 18,000 shares to maintain its 90% interest in Jones.

After acquiring the additional shares, what adjustment is needed for Webb's investment in Jones account?

(Multiple Choice)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)