Exam 8: Segment and Interim Reporting

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information115 Questions

Exam 3: Consolidations-Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements - Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flo115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income118 Questions

Exam 8: Segment and Interim Reporting113 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations82 Questions

Exam 14: Partnerships: Formation and Operations88 Questions

Exam 15: Partnerships: Termination and Liquidation70 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments46 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

What is the appropriate treatment in an interim financial report for inventory that has cost below market value?

(Multiple Choice)

4.9/5  (40)

(40)

Which of the following is reported for interim financial reports using the integral approach?

(Multiple Choice)

4.8/5 (41)

Cement Company, Inc. began the first quarter with 1,000 units of inventory costing $25 per unit. During the first quarter, 3,000 units were purchased at a cost of $40 per unit, and sales of 3,400 units at $65 per units were made. During the second quarter, the company expects to replace the units of beginning inventory sold at a cost of $45 per unit. Cement Company uses the LIFO method to account for inventory.

-What is the correct journal entry to record cost of goods sold at the end of the first quarter? A) Inventory 8,000 Cost of Goods Sold 8,000 B) Inventory 8,000 Excess of replacement cost over historical cost of LIFO liquidation 8,000 C) Cost of goods sold 138,000 Inventory 130,000 Excess of replacement cost over historical cost of LIFO liquidation 8,000 D) Cost of goods sold 130,000 Excess of replacement cost over historical cost of LIFO liquidation 8,000 Inventory 138,000 E) No journal entry is required

(Multiple Choice)

4.9/5 (44)

Which of the following is reported for interim financial reports using the discrete approach?

(Multiple Choice)

4.8/5 (35)

Which of the following are required to be disclosed in interim reports?

(Multiple Choice)

4.9/5 (45)

How should seasonal revenues be reported in an interim financial statement?

(Multiple Choice)

4.9/5 (37)

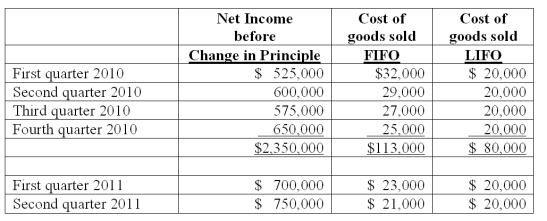

Harrison Company, Inc. began operations on January 1, 2010, and applied the LIFO method for inventory valuation. On June 10, 2011, Harrison adopted the FIFO method of accounting for inventory. Additional information is as follows:  The LIFO method was applied during the first quarter of 2011 and the FIFO method was applied during the second quarter of 2011 in computing income, above. Harrison's effective income tax rate is 40 percent. Harrison has 500,000 shares of common stock outstanding at all times.

-Compute the after-tax effect of Harrison's change in inventory method.

The LIFO method was applied during the first quarter of 2011 and the FIFO method was applied during the second quarter of 2011 in computing income, above. Harrison's effective income tax rate is 40 percent. Harrison has 500,000 shares of common stock outstanding at all times.

-Compute the after-tax effect of Harrison's change in inventory method.

(Essay)

4.9/5 (43)

Gregor, Inc., uses the LIFO cost-flow assumption to value inventory. Inventory for Gregor on January 1, 2011 was 100 units at a LIFO cost of $25 per unit. During the first quarter of 2011, 200 units were purchased costing an average of $40 per unit, and sales of 265 units at a retail price of $50 per unit were made.

-Assuming Gregor does not expect to replace the units of beginning inventory sold, what is the amount of cost of goods sold for the quarter ended March 31, 2011?

(Short Answer)

4.9/5 (35)

Describe the test to determine whether a sufficient number of operating segments are disclosed.

(Essay)

4.9/5 (41)

According to International Financial Reporting Standards (IFRS), all of the following are part of minimum components of interim financial reporting except:

(Multiple Choice)

4.9/5 (37)

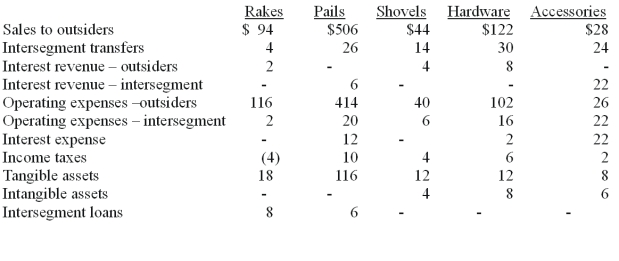

Dean Hardware, Inc. is comprised of five operating segments. Information about each of these segments is as follows (in thousands; Intersegment loans are receivables):  -What is the total amount of revenues in applying the revenue test?

-What is the total amount of revenues in applying the revenue test?

(Multiple Choice)

4.8/5 (34)

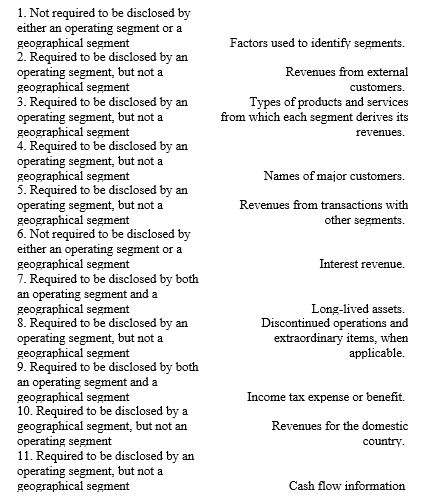

Which one of the following items must be disclosed for all reportable operating segments in the notes to financial statements?

(I) Revenue from external customers.

(II) Total Segment Assets

(III) Revenues from foreign customers, identified by country.

(Multiple Choice)

4.8/5 (43)

Which of the following is not true for an operating segment according to U.S. GAAP?

(Multiple Choice)

4.7/5 (35)

For each of the following situations, select the best answer concerning segment disclosures of reportable segments.

(Essay)

4.8/5 (39)

Which of the following is not a required disclosure in an interim financial report?

(Multiple Choice)

4.7/5 (36)

What two disclosure guidelines for operating segment information are designed to ensure the consistency of data reported from year to year?

(Essay)

4.9/5 (33)

According to U.S. GAAP, what general information about an operating segment needs to be disclosed?

(Essay)

4.8/5 (32)

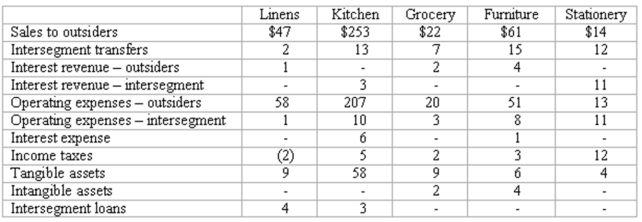

Blanton Corporation is comprised of five operating segments. Information about each of these segments is as follows (in thousands):  Required:

(a) Which operating segments are reportable under the revenue test?

(b) What is the total amount of revenues in applying the revenues test?

(c) Which operating segments are reportable under the profit or loss test?

(d) In applying the profit or loss test, what is the minimum amount an operating segment must have in order to meet the profit or loss test for a reportable segment?

(e) Which operating segments are reportable under the asset test?

(f) In applying the asset test, what is the minimum amount an operating segment must have in order to meet the asset test for a reportable segment?

(g) Which operating segments are reportable?

(h) According to the test results for reportable segments, is there a sufficient number of reported segments or should any additional segments also be disclosed? Explain the reason for your conclusion.

Required:

(a) Which operating segments are reportable under the revenue test?

(b) What is the total amount of revenues in applying the revenues test?

(c) Which operating segments are reportable under the profit or loss test?

(d) In applying the profit or loss test, what is the minimum amount an operating segment must have in order to meet the profit or loss test for a reportable segment?

(e) Which operating segments are reportable under the asset test?

(f) In applying the asset test, what is the minimum amount an operating segment must have in order to meet the asset test for a reportable segment?

(g) Which operating segments are reportable?

(h) According to the test results for reportable segments, is there a sufficient number of reported segments or should any additional segments also be disclosed? Explain the reason for your conclusion.

(Essay)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)