Exam 5: Consolidated Financial Statements - Intra-Entity Asset Transactions

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information115 Questions

Exam 3: Consolidations-Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements - Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flo115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income118 Questions

Exam 8: Segment and Interim Reporting113 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations82 Questions

Exam 14: Partnerships: Formation and Operations88 Questions

Exam 15: Partnerships: Termination and Liquidation70 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments46 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012, respectively. Parker sold the land it purchased from Stark in 2010 for $92,000 in 2012.

-Which of the following will be included in a consolidation entry for 2010?

(Multiple Choice)

4.8/5  (39)

(39)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends: 2010 2011 2012 Net income \ 100,000 \ 120,000 \ 130,000 Dividends 40,000 50,000 60,000

-Compute the amortization of gain through a depreciation adjustment for 2012 for consolidation purposes.

(Multiple Choice)

4.7/5 (34)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends: 2010 2011 2012 Net income \ 100,000 \ 120,000 \ 130,000 Dividends 40,000 50,000 60,000

-Compute Wilson's share of income from Simon for consolidation for 2011.

(Multiple Choice)

4.7/5 (38)

Yoderly Co., a wholly owned subsidiary of Nelson Corp., sold goods to Nelson near the end of 2011. The goods had cost Yoderly $105,000 and the selling price was $140,000. Nelson had not sold any of the goods by the end of the year.

Required:

Prepare Consolidation Entry TI and Consolidation Entry G that are required for 2011.

(Essay)

4.8/5 (37)

Dalton Corp. owned 70% of the outstanding common stock of Shrugs Inc. On January 1, 2009, Dalton acquired a building with a ten-year life for $420,000. No salvage value was anticipated and the building was to be depreciated on the straight-line basis. On January 1, 2011, Dalton sold this building to Shrugs for $392,000. At that time, the building had a remaining life of eight years but still no expected salvage value. In preparing financial statements for 2011, how does this transfer affect the calculation of Dalton's share of consolidated net income?

(Multiple Choice)

4.9/5 (40)

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

-In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate the intra-entity transfer of inventory?

(Multiple Choice)

4.9/5 (38)

On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins, Inc., transferred equipment with a 10-year life (six of which remain with no salvage value) to Collins in exchange for $84,000 cash. At the date of transfer, Smeder's records carried the equipment at a cost of $120,000 less accumulated depreciation of $48,000. Straight-line depreciation is used. Smeder reported net income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income effects of the intra-entity transfer are attributed to the seller for consolidation purposes.

-What is the net effect on consolidated net income in 2010 due to the equipment transfer?

(Multiple Choice)

4.7/5 (35)

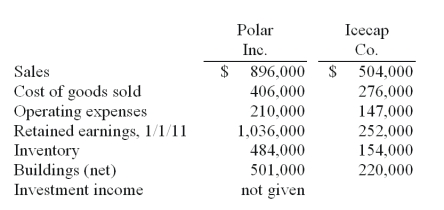

Several years ago Polar Inc. acquired an 80% interest in Icecap Co. The book values of Icecap's asset and liability accounts at that time were considered to be equal to their fair values. Polar's acquisition value corresponded to the underlying book value of Icecap so that no allocations or goodwill resulted from the transaction.

The following selected account balances were from the individual financial records of these two companies as of December 31, 2011:  -Assume that Polar sold inventory to Icecap at a markup equal to 25% of cost. Intra-entity transfers were $130,000 in 2010 and $165,000 in 2011. Of this inventory, $39,000 of the 2010 transfers were retained and then sold by Icecap in 2011 while $55,000 of the 2011 transfers were held until 2012.

Required:

For the consolidated financial statements for 2011, determine the balances that would appear for the following accounts: (1) Cost of Goods Sold, (2) Inventory, and (3) Noncontrolling Interest in Subsidiary's Net Income.

-Assume that Polar sold inventory to Icecap at a markup equal to 25% of cost. Intra-entity transfers were $130,000 in 2010 and $165,000 in 2011. Of this inventory, $39,000 of the 2010 transfers were retained and then sold by Icecap in 2011 while $55,000 of the 2011 transfers were held until 2012.

Required:

For the consolidated financial statements for 2011, determine the balances that would appear for the following accounts: (1) Cost of Goods Sold, (2) Inventory, and (3) Noncontrolling Interest in Subsidiary's Net Income.

(Essay)

4.7/5 (39)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends: 2010 2011 2012 Net income \ 100,000 \ 120,000 \ 130,000 Dividends 40,000 50,000 60,000

-Compute Wilson's share of income from Simon for consolidation for 2010.

(Multiple Choice)

4.8/5 (34)

Edgar Co. acquired 60% of Stendall Co. on January 1, 2011. During 2011, Edgar made several sales of inventory to Stendall. The cost and selling price of the goods were $140,000 and $200,000, respectively. Stendall still owned one-fourth of the goods at the end of 2011. Consolidated cost of goods sold for 2011 was $2,140,000 because of a consolidating adjustment for intra-entity sales less the entire profit remaining in Stendall's ending inventory.

-How would consolidated cost of goods sold have differed if the inventory transfers had been for the same amount and cost, but from Stendall to Edgar?

(Multiple Choice)

4.7/5 (35)

McGraw Corp. owned all of the voting common stock of both Ritter Co. and Lawler Co. During 2011, Ritter sold inventory to Lawler. The goods had cost Ritter $65,000, and they were sold to Lawler for $100,000. At the end of 2011, Lawler still held 30% of the inventory.

Required:

How should the sale between Lawler and Ritter be accounted for in a consolidation worksheet? Show worksheet entries to support your answer.

(Essay)

4.8/5 (32)

Wilson owned equipment with an estimated life of 10 years when it was acquired for an original cost of $80,000. The equipment had a book value of $50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company, bought the equipment from Wilson for $68,250 and for depreciation purposes used the estimated remaining life as of that date. The following data are available pertaining to Simon's income and dividends: 2010 2011 2012 Net income \ 100,000 \ 120,000 \ 130,000 Dividends 40,000 50,000 60,000

-Compute Wilson's share of income from Simon for consolidation for 2012.

(Multiple Choice)

5.0/5 (33)

Walsh Company sells inventory to its subsidiary, Fisher Company, at a profit during 2010. One-third of the inventory is sold by Walsh uses the equity method to account for its investment in Fisher.

-In the consolidation worksheet for 2010, which of the following choices would be a debit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

(Multiple Choice)

4.7/5 (48)

For consolidation purposes, what amount would be debited to January 1 retained earnings for the 2012 consolidation worksheet entry with regard to the unrealized gross profit of the 2011 intra-entity transfer of merchandise?

(Multiple Choice)

4.7/5 (45)

Strickland Company sells inventory to its parent, Carter Company, at a profit during 2010. One-third of the inventory is sold by Carter in 2010.

-In the consolidation worksheet for 2010, which of the following choices would be a credit entry to eliminate unrealized intra-entity gross profit with regard to the 2010 intra-entity sales?

(Multiple Choice)

4.9/5 (37)

The reported sales did not include any intra-entity sales. In addition to the reported amounts, there were intra-entity sales from Pot to Skillet in the amount of $140,000. There were no sales from Skillet to Pot. Intra-entity sales had the same markup as sales to outsiders. Skillet still had 40% of the intra-entity sales as inventory at the end of 2011. What are consolidated sales and cost of goods sold for 2011?

(Multiple Choice)

4.8/5 (35)

For each of the following situations (1 - 10), select the correct entry (A - E) that would be required on a consolidation worksheet.

(Essay)

4.7/5 (37)

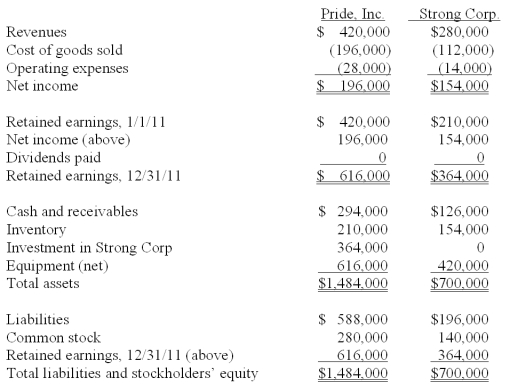

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows:  During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

-What is the consolidated total for inventory at December 31, 2011?

During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

-What is the consolidated total for inventory at December 31, 2011?

(Multiple Choice)

4.9/5 (39)

On January 1, 2011, Pride, Inc. acquired 80% of the outstanding voting common stock of Strong Corp. for $364,000. There is no active market for Strong's stock. Of this payment, $28,000 was allocated to equipment (with a five-year life) that had been undervalued on Strong's books by $35,000. Any remaining excess was attributable to goodwill which has not been impaired.

As of December 31, 2011, before preparing the consolidated worksheet, the financial statements appeared as follows: During 2011, Pride bought inventory for $112,000 and sold it to Strong for $140,000. Only half of this purchase had been paid for by Strong by the end of the year. 60% of these goods were still in the company's possession on December 31.

-What is the total of consolidated cost of goods sold?

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)