Exam 23: Single Period Binomial Heath Jarrow Morton Model

Exam 1: Derivatives and Risk Management16 Questions

Exam 2: Interest Rates15 Questions

Exam 3: Stocks19 Questions

Exam 4: Forwards and Futures15 Questions

Exam 5: Options18 Questions

Exam 6: Arbitrage and Trading12 Questions

Exam 7: Financial Engineering and Swaps15 Questions

Exam 8: Forwards and Futures Markets17 Questions

Exam 9: Futures Trading14 Questions

Exam 10: Futures Regulations20 Questions

Exam 11: The Cost of Carry Model15 Questions

Exam 12: The Extended Cost-Of-Carry Model20 Questions

Exam 13: Futures Hedging13 Questions

Exam 14: Options Markets and Trading19 Questions

Exam 15: Option Trading Strategies16 Questions

Exam 16: Option Relations21 Questions

Exam 17: Single-Period Binomial Model21 Questions

Exam 18: Multiperiod Binomial Model26 Questions

Exam 19: The Black-Scholes-Merton Model23 Questions

Exam 20: Using the Black-Scholes-Merton Model17 Questions

Exam 21: Yields and Forward Rates17 Questions

Exam 22: Interest Rate Swaps20 Questions

Exam 23: Single Period Binomial Heath Jarrow Morton Model23 Questions

Exam 24: Multiperiod Binomial Heath Jarrow Morton Model20 Questions

Exam 25: The Heath Jarrow Morton Libor Model23 Questions

Exam 26: Risk-Management Models18 Questions

Select questions type

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

Use the fact that the pseudo-probability of default at time zero is (1/ 2)to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

(Multiple Choice)

4.8/5  (40)

(40)

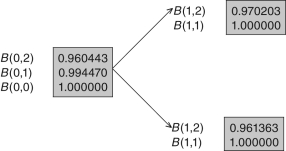

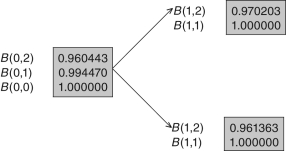

Use the following tree to answer the questions that follow.  -What are the forward rates f (0,1),f (0,0)?

-What are the forward rates f (0,1),f (0,0)?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)