Exam 28: Translation of the Financial Statements of Foreign Entities

Exam 1: The Conceptual Framework of the Iasb30 Questions

Exam 2: Shareholders Equity: Share Capital and Reserves28 Questions

Exam 3: Fair Value Measurement30 Questions

Exam 4: Revenue30 Questions

Exam 5: Provisions, Contingent Liabilities and Contingent Assets30 Questions

Exam 6: Income Taxes28 Questions

Exam 7: Financial Instruments30 Questions

Exam 8: Share-Based Payments28 Questions

Exam 9: Inventories29 Questions

Exam 10: Employee Benefits29 Questions

Exam 11: Property, Plant and Equipment28 Questions

Exam 12: Leases27 Questions

Exam 13: Intangible Assets28 Questions

Exam 14: Business Combinations30 Questions

Exam 15: Impairment of Assets28 Questions

Exam 16: Accounting for Mineral Resources26 Questions

Exam 17: Agriculture26 Questions

Exam 18: Financial Statement Presentation29 Questions

Exam 19: Statement of Cash Flows28 Questions

Exam 20: Earnings Per Share20 Questions

Exam 21: Operating Segments30 Questions

Exam 22: Operating Segments29 Questions

Exam 23: Consolidation: Controlled Entities29 Questions

Exam 24: Consolidation: Wholly Owned Subsidiaries26 Questions

Exam 25: Consolidation: Intragroup Transactions27 Questions

Exam 26: Consolidation: Non-Controlling Interest25 Questions

Exam 27: Consolidation: Other Issues29 Questions

Exam 28: Translation of the Financial Statements of Foreign Entities28 Questions

Exam 29: Associates and Joint Ventures26 Questions

Exam 30: Joint Arrangements26 Questions

Select questions type

When an entity has an investment in a foreign domiciled entity it is necessary to translate the financial statements of the foreign operation to the currency used by the investor:

Free

(Multiple Choice)

4.8/5  (30)

(30)

Correct Answer: Verified

Verified

C

In order for the financial statements of a foreign operation to be included in the consolidated financial statements of the parent it is necessary to translate the foreign operation's financial statements into:

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

A

When translating foreign currency denominated financial statements into the functional currency, the exchange differences are recognised:

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

A

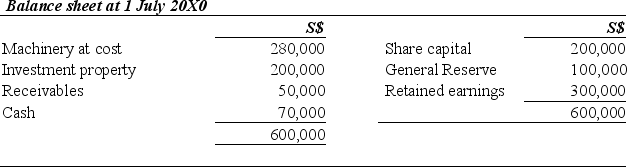

The following information relates to question 3 and 4

Aussie Ltd acquired 100% of Sing Sing Ltd (Sing Sing) on 1 July 20X0. The balance sheet of Sing Sing on that date was as follows:

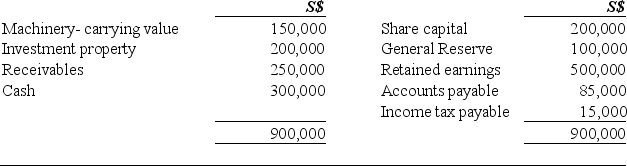

The balance sheet of Sing Sing as at is as follows:

Balance Sheet as at 30 June 20X1

The balance sheet of Sing Sing as at is as follows:

Balance Sheet as at 30 June 20X1

Relevant exchange rates are as follows:

Relevant exchange rates are as follows:

-If the functional currency of Sing Sing is Singapore dollars and the presentation currency is Australian dollars the total assets of S$900,000 would translate into Australian dollars as:

-If the functional currency of Sing Sing is Singapore dollars and the presentation currency is Australian dollars the total assets of S$900,000 would translate into Australian dollars as:

(Multiple Choice)

4.9/5 (36)

The following information relates to question 3 and 4

Aussie Ltd acquired 100% of Sing Sing Ltd (Sing Sing) on 1 July 20X0. The balance sheet of Sing Sing on that date was as follows:

The balance sheet of Sing Sing as at is as follows:

Balance Sheet as at 30 June 20X1

Relevant exchange rates are as follows:

-If the local currency of Sing Sing is Singapore dollars and the functional currency is Australian dollars the total assets of S$900,000 would translate into Australian dollars as:

(Multiple Choice)

4.9/5 (37)

Aussie Ltd has an investment in Yankee Inc. The shares in Yankee were acquired on 15 August 20X4. Yankee uses the revaluation model to account for land & buildings. A building which was acquired by Yankee on 1 April 20X2 was revalued on 15 March 20X9. The exchange rate used to translate the building into the presentation currency at 30 June 20X9 is the rate that applied on:

(Multiple Choice)

4.9/5 (47)

The general rule for translating liabilities denominated in a foreign currency into the functional currency is to:

(Multiple Choice)

4.7/5 (29)

The following information relates to questions 23 to 25

On 1 January 20X3, Claudia Ltd, an Australian company, acquired 80% of the shares of Saskia Ltd, a New Zealand company, for A$2 498 000. At that date the share capital of Saskia was NZ$2 million and the retained earnings were NZ$1 440 000.

All the assets and liabilities of Saskia were recorded at fair value except for land, for which the fair value was NZ$200 000 higher than the carrying amount and equipment, for which the fair value was NZ$80 000 higher than the carrying amount. The undervalued equipment had a further 4-year life. The tax rate in New Zealand is 25%.

Exchange rates are as follows:

1 January 20X3 A$1.00 = NZ$1.20

31 December 20X3 A$1.00 = NZ$1.40

Average for the year A$1.00 = NZ$1.30

-The adjustment to the foreign currency translation reserve on 31 December 20X3 relating to the revaluation of the land if the functional currency of Saskia is Australian dollars dollars is:

(Multiple Choice)

4.8/5 (48)

If foreign currency denominated non-monetary items are measured using the fair value method, they must be translated into the functional currency using the:

(Multiple Choice)

4.9/5 (38)

By applying the definition provided in IAS 21 The Effects of Changes in Foreign Exchange Rates, the following items will be regarded as a monetary item:

(Multiple Choice)

4.9/5 (33)

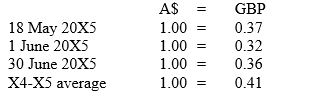

The following information relates to questions 20 to 22

Aussie Ltd has a controlling interest in Pommie Plc. On 1 June 20X5 Pommie sold inventory to Aussie for 10 000 pounds. The inventory was originally acquired by Pommie on 18 May 20X5 for 7000 pounds. The entire amount of inventory was held by Aussie at 30 June 20X5. The Australian tax rate is 30% and the British tax rate is 35%.

Exchange rates are as follows:

-The debit to the deferred tax asset account in relation to the elimination of the intragroup sale (to the nearest whole dollar) is:

-The debit to the deferred tax asset account in relation to the elimination of the intragroup sale (to the nearest whole dollar) is:

(Multiple Choice)

4.8/5 (41)

When translating into the functional currency foreign currency denominated non-monetary items measured using historical cost must be translated using the:

(Multiple Choice)

4.8/5 (36)

A Ltd has an 80% investment in B Inc. A Ltd lent $US500,000 to B Inc on 1 January 20X4. The loan is considered to form part of the net investment in B Inc. The functional currency of A Ltd is Australian dollars and for B Inc is US dollars.

The exchange rate on 1 January 20X4 was $A1.00 = $US0.875 and on 30 June 20X4 was $A1.00 = $US0.750.

The consolidation adjustment to the foreign currency translation reserve at 30 June 20X4 in relation to the loan (to the nearest whole dollar) is:

(Multiple Choice)

4.7/5 (46)

The following information relates to questions 20 to 22

Aussie Ltd has a controlling interest in Pommie Plc. On 1 June 20X5 Pommie sold inventory to Aussie for 10 000 pounds. The inventory was originally acquired by Pommie on 18 May 20X5 for 7000 pounds. The entire amount of inventory was held by Aussie at 30 June 20X5. The Australian tax rate is 30% and the British tax rate is 35%.

Exchange rates are as follows:

-The credit to inventory in relation to the elimination of the intragroup sale (to the nearest whole dollar) is:

(Multiple Choice)

4.9/5 (35)

When translating the revenue and expenses in the statement of profit or loss and other comprehensive income, theoretically each item of revenue and expense should be translated using the spot exchange rate between the:

(Multiple Choice)

4.7/5 (33)

The following information relates to questions 20 to 22

Aussie Ltd has a controlling interest in Pommie Plc. On 1 June 20X5 Pommie sold inventory to Aussie for 10 000 pounds. The inventory was originally acquired by Pommie on 18 May 20X5 for 7000 pounds. The entire amount of inventory was held by Aussie at 30 June 20X5. The Australian tax rate is 30% and the British tax rate is 35%.

Exchange rates are as follows:

-The credit to cost of goods sold to eliminate the intragroup sale (to the nearest whole dollar) is:

(Multiple Choice)

4.9/5 (37)

When translating into the functional currency monetary liabilities are translated using the:

(Multiple Choice)

4.9/5 (40)

The following information relates to questions 23 to 25

On 1 January 20X3, Claudia Ltd, an Australian company, acquired 80% of the shares of Saskia Ltd, a New Zealand company, for A$2 498 000. At that date the share capital of Saskia was NZ$2 million and the retained earnings were NZ$1 440 000.

All the assets and liabilities of Saskia were recorded at fair value except for land, for which the fair value was NZ$200 000 higher than the carrying amount and equipment, for which the fair value was NZ$80 000 higher than the carrying amount. The undervalued equipment had a further 4-year life. The tax rate in New Zealand is 25%.

Exchange rates are as follows:

1 January 20X3 A$1.00 = NZ$1.20

31 December 20X3 A$1.00 = NZ$1.40

Average for the year A$1.00 = NZ$1.30

-The adjustment to the foreign currency translation reserve on 31 December 20X3 relating to the revaluation of the land if the functional currency of Saskia is New Zealand dollars is:

(Multiple Choice)

4.9/5 (41)

Where a change in the functional currency occurs, the translation procedures as outlined in IAS 21 The Effects of Changes in Foreign Exchange Rules, apply:

(Multiple Choice)

4.9/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)