Exam 25: Consolidation: Intragroup Transactions

Exam 1: The Conceptual Framework of the Iasb30 Questions

Exam 2: Shareholders Equity: Share Capital and Reserves28 Questions

Exam 3: Fair Value Measurement30 Questions

Exam 4: Revenue30 Questions

Exam 5: Provisions, Contingent Liabilities and Contingent Assets30 Questions

Exam 6: Income Taxes28 Questions

Exam 7: Financial Instruments30 Questions

Exam 8: Share-Based Payments28 Questions

Exam 9: Inventories29 Questions

Exam 10: Employee Benefits29 Questions

Exam 11: Property, Plant and Equipment28 Questions

Exam 12: Leases27 Questions

Exam 13: Intangible Assets28 Questions

Exam 14: Business Combinations30 Questions

Exam 15: Impairment of Assets28 Questions

Exam 16: Accounting for Mineral Resources26 Questions

Exam 17: Agriculture26 Questions

Exam 18: Financial Statement Presentation29 Questions

Exam 19: Statement of Cash Flows28 Questions

Exam 20: Earnings Per Share20 Questions

Exam 21: Operating Segments30 Questions

Exam 22: Operating Segments29 Questions

Exam 23: Consolidation: Controlled Entities29 Questions

Exam 24: Consolidation: Wholly Owned Subsidiaries26 Questions

Exam 25: Consolidation: Intragroup Transactions27 Questions

Exam 26: Consolidation: Non-Controlling Interest25 Questions

Exam 27: Consolidation: Other Issues29 Questions

Exam 28: Translation of the Financial Statements of Foreign Entities28 Questions

Exam 29: Associates and Joint Ventures26 Questions

Exam 30: Joint Arrangements26 Questions

Select questions type

A Ltd sold an item of plant to B Ltd on 1 January 20X7 for $25 000. The asset had cost A Ltd $30 000 when acquired on 1 January 20X5. At that time the useful life of the plant was assessed at 6 years. The consolidation elimination entries at 30 June 20X7 in relation to the sale of plant is (rounded to nearest dollar):

Free

(Multiple Choice)

4.8/5  (39)

(39)

Correct Answer: Verified

Verified

C

Janus Limited, a subsidiary entity, sold a non-current asset at a profit to its parent entity. The adjustment necessary on consolidation to reflect the tax effect of this transaction will result in an:

Free

(Multiple Choice)

4.8/5 (34)

Correct Answer:Verified

A

When an entity sells a non-current asset at a profit to another entity within the same group the following adjustment is necessary on consolidation:

Free

(Multiple Choice)

4.7/5 (29)

Correct Answer:Verified

C

A consolidation worksheet adjustment to eliminate the effect of interest revenue and interest expense relating to intragroup advances has the following tax effect:

(Multiple Choice)

4.9/5 (45)

Jameson purchased goods from its subsidiary for $10 000. The goods cost the subsidiary $6000. At reporting date, Jameson still held all of the goods. The company rate of tax is 30%. Which of the following consolidation adjustment entries is correct?

(Multiple Choice)

4.9/5 (41)

A subsidiary entity sold inventory to its parent entity at a profit of $4 000. The goods had originally cost the subsidiary $10 000. At the end of the year all the inventory was still on hand. The adjustment entry to deal with this transaction on consolidation would include the following line item:

(Multiple Choice)

4.9/5 (42)

If a dividend is paid out of profits that are earned after the acquisition date, it is known as:

(Multiple Choice)

4.9/5 (38)

When a subsidiary declares a final dividend payable to a parent who has a 100% interest in the subsidiary the parent recognises a dividend receivable and the subsidiary recognises a dividend payable. In addition to the elimination of these two items on consolidation, the following items must also be eliminated:

(Multiple Choice)

5.0/5 (40)

When eliminating an intragroup service which of the following would appear in the consolidation worksheet entry?

(Multiple Choice)

4.9/5 (39)

A Ltd sold an item of plant to B Ltd on 1 January 20X7 for $25 000. The asset had cost A Ltd $30 000 when acquired on 1 January 20X5. At that time the useful life of the plant was assessed at 6 years. The adjustment necessary on consolidation in relation to the transfer of plant as at 30 June 20X8 will result in:

(Multiple Choice)

4.9/5 (39)

On 16 May 20X4, Z Ltd sold equipment to N Ltd for $50 000, this asset having a carrying amount at time of sale of $40 000. The equipment was regarded by Z Ltd as a depreciable non-current asset, being depreciated at 10% p.a. on cost, whereas N Ltd records the machinery as inventory. The asset was sold by N Ltd before 30 June 20X4. The worksheet entry for the year ended 30 June 20X3 would include the following adjustment:

(Multiple Choice)

4.8/5 (33)

A subsidiary entity sold goods to its parent entity at a profit of $10 000. The goods had originally cost the subsidiary $15 000. At reporting date, the parent still held all of the goods. Which of the following adjustments must be included as part of the consolidation entry to eliminate this transaction?

(Multiple Choice)

4.9/5 (37)

If an entity sells a non-current asset at a profit to another entity within the same group the following consolidation adjustment is necessary to reflect the tax effect:

(Multiple Choice)

4.8/5 (40)

A subsidiary entity sold inventory to its parent entity at a profit of $8 000. The goods had originally cost the subsidiary $20 000. At the end of the year all the inventory was still on hand. The adjustment entry to deal with this transaction on consolidation would include the following line item:

(Multiple Choice)

4.8/5 (33)

A Ltd sold an item of plant to B Ltd on 1 January 20X7 for $25 000. The asset had cost A Ltd $30 000 when acquired on 1 January 20X5. At that time the useful life of the plant was assessed at 6 years. The adjustment necessary on consolidation to reflect the tax effect of the depreciation adjustment for the year ended 30 June 20X7 will result in an increase in:

(Multiple Choice)

4.7/5 (32)

During the year ended 30 June 20X7 a subsidiary entity sold inventory to its parent entity at a profit of $8 000. The goods had originally cost the subsidiary $20 000. At the end of 30 June 20X7 all the inventory was still on hand. Ignoring tax effects, the adjustment entry to deal with this transaction on consolidation during the year ended 30 June 20X8 would include the following line item:

(Multiple Choice)

4.8/5 (30)

The test indicating that an intragroup business transaction has been realised is:

(Multiple Choice)

4.8/5 (32)

A parent entity group sold a depreciable non-current asset to a subsidiary entity for $2800. The asset originally cost $3000 and at the date of sale accumulated depreciation was $500. The amount of the unrealised gain on sale to be eliminated is:

(Multiple Choice)

4.9/5 (41)

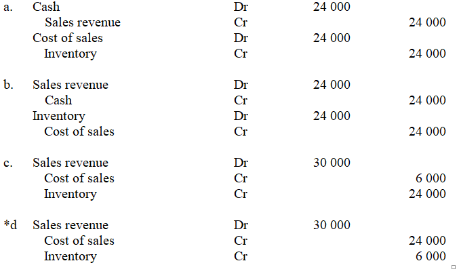

In May 20X7, a parent entity sold inventory to a subsidiary entity for $30 000. The inventory had previously cost the parent entity $24 000. The entire inventory is still held by the subsidiary at reporting date, 30 June 20X7. Ignoring tax effects, the adjustment entry in the consolidation worksheet at reporting date is:

(Essay)

4.8/5 (36)

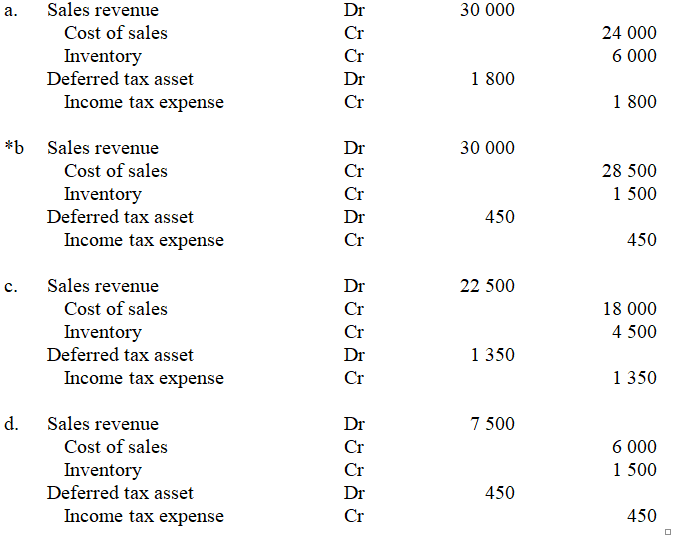

A subsidiary entity sold inventory to a parent entity for $30 000. The inventory had previously cost the subsidiary entity $24 000. By reporting date the parent entity had sold 75% of the inventory to a party outside the group. The company tax rate is 30%. The adjustment entry in the consolidation worksheet at reporting date is:

(Essay)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)