Exam 23: Consolidation: Controlled Entities

Exam 1: The Conceptual Framework of the Iasb30 Questions

Exam 2: Shareholders Equity: Share Capital and Reserves28 Questions

Exam 3: Fair Value Measurement30 Questions

Exam 4: Revenue30 Questions

Exam 5: Provisions, Contingent Liabilities and Contingent Assets30 Questions

Exam 6: Income Taxes28 Questions

Exam 7: Financial Instruments30 Questions

Exam 8: Share-Based Payments28 Questions

Exam 9: Inventories29 Questions

Exam 10: Employee Benefits29 Questions

Exam 11: Property, Plant and Equipment28 Questions

Exam 12: Leases27 Questions

Exam 13: Intangible Assets28 Questions

Exam 14: Business Combinations30 Questions

Exam 15: Impairment of Assets28 Questions

Exam 16: Accounting for Mineral Resources26 Questions

Exam 17: Agriculture26 Questions

Exam 18: Financial Statement Presentation29 Questions

Exam 19: Statement of Cash Flows28 Questions

Exam 20: Earnings Per Share20 Questions

Exam 21: Operating Segments30 Questions

Exam 22: Operating Segments29 Questions

Exam 23: Consolidation: Controlled Entities29 Questions

Exam 24: Consolidation: Wholly Owned Subsidiaries26 Questions

Exam 25: Consolidation: Intragroup Transactions27 Questions

Exam 26: Consolidation: Non-Controlling Interest25 Questions

Exam 27: Consolidation: Other Issues29 Questions

Exam 28: Translation of the Financial Statements of Foreign Entities28 Questions

Exam 29: Associates and Joint Ventures26 Questions

Exam 30: Joint Arrangements26 Questions

Select questions type

The key criterion for the consolidation of the separate financial statements of entities is:

Free

(Multiple Choice)

4.8/5  (39)

(39)

Correct Answer: Verified

Verified

B

The entity that is represented by a single set of consolidated financial statements known as a consolidated financial report, is:

Free

(Multiple Choice)

4.9/5 (44)

Correct Answer:Verified

A

Which is not one of the three elements of control?

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

B

Two entities A Limited and B Limited together form a third entity, C Limited. C Limited acquires A Limited and B Limited. In this situation, IFRS 3 Business Combinations adjudges that:

(Multiple Choice)

4.8/5 (38)

Truong Limited acquired 60% of the shares of Quang Limited through the Australian Securities Exchange. The share acquisition cost Truong Limited $500 000. As a result of the share acquisition, Truong Limited gained control over Quang Limited. In its accounting records, Truong will recognise:

(Multiple Choice)

4.8/5 (37)

A single set of financial statements, that combines the separate sets of financial statements for a number of entities, which are managed as a single economic entity, is known as:

(Multiple Choice)

4.8/5 (41)

In a consolidated group of entities, control over the subsidiaries in the group:

(Multiple Choice)

4.8/5 (36)

According to IFRS 10 Consolidated Financial Statements, which of the following factors indicate the existence of control?

I. Possessing existing rights that give the current ability to direct the relevant activities.

II. Shared power in the governance of financial and operating policies of another entity so as to obtain benefits.

III. The power to govern the operating policies of an entity so as to obtain benefits.

IV. Ownership of more than 50% of the voting power in the subsidiary.

(Multiple Choice)

4.8/5 (37)

According to IFRS 12 Disclosure of Interests in Other Parties, parent entities are required to disclose:

I. Summarised financial information about each subsidiary.

II. A list of significant investments in subsidiaries.

III. If the subsidiary is not wholly owned, the names of all other members.

IV. The country of incorporation of subsidiaries.

(Multiple Choice)

4.9/5 (41)

Which of the following is correct in relation to rights in the context of control?

(Multiple Choice)

4.9/5 (28)

The process of aggregating individual sets of financial statements to produce consolidated financial statements requires:

(Multiple Choice)

4.9/5 (40)

A Ltd is a listed public company and has an 80% controlling interest in B Pty Ltd. B Pty Ltd is the parent of C Pty Ltd. In which of the following situations will B Pty Ltd not be required to prepare consolidated financial statements?

(Multiple Choice)

4.8/5 (37)

A group of entities comprised of A Limited (parent entity), B Limited (subsidiary entity) and C Limited (subsidiary entity) have the following Accounts Receivable balances:

A Limited $12 000

B Limited $15 000

C Limited $10 000

The consolidated financial statements show the following amount as the consolidated Accounts Receivable balance:

(Multiple Choice)

4.8/5 (42)

The main characteristic of a structured entity according to IFRS 12 is that:

(Multiple Choice)

4.8/5 (40)

When one entity controls the business operations of another entity, the business combination results in the following type of relationship:

(Multiple Choice)

4.7/5 (44)

Control is automatically presumed to exist where the parent either directly or indirectly through subsidiaries owns:

(Multiple Choice)

4.8/5 (44)

In a situation where a controlling entity has delegated control to another entity, the parent is presumed to be:

(Multiple Choice)

4.9/5 (37)

For one entity to control another entity, the percentage of share ownership held by the controlling entity:

(Multiple Choice)

4.7/5 (35)

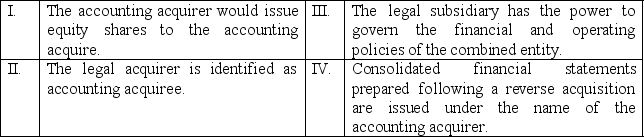

Which of the following statements applies to reverse acquisitions?

Tin accou acquirer is identified as accounting acquiree.ontrolling entity;

Other assets (in the case where equity instruments

Tin accou acquirer is identified as accounting acquiree.ontrolling entity;

Other assets (in the case where equity instruments

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)