Exam 22: Consolidation: Other Issues

Exam 1: Nature and Regulation of Companies50 Questions

Exam 2: Financing Company Operations48 Questions

Exam 3: Company Operations49 Questions

Exam 4: Fundamental Concepts of Corporate Governance50 Questions

Exam 5: Fair Value Measurement50 Questions

Exam 6: Accounting for Company Income Tax18 Questions

Exam 7: Financial Instruments20 Questions

Exam 8: Foreign Currency Transactions and Forward Exchange Contracts20 Questions

Exam 9: Property, Plant and Equipment47 Questions

Exam 10: Leases18 Questions

Exam 11: Intangible Assets50 Questions

Exam 12: Business Combinations49 Questions

Exam 13: Impairment of Assets49 Questions

Exam 14: Disclosure: Legal Requirements and Accounting Polices50 Questions

Exam 15: Disclosure: Presentation of Financial Statements50 Questions

Exam 16: Disclosure: Statement of Cash Flows18 Questions

Exam 17: Disclosure: Translation of Financial Statements Into a Presentation Currency29 Questions

Exam 18: Consolidation: Controlled Entities49 Questions

Exam 19: Consolidation: Wholly Owned Subsidiaries47 Questions

Exam 20: Consolidation: Intragroup Transactions47 Questions

Exam 21: Consolidation: Non-Controlling Interest50 Questions

Exam 22: Consolidation: Other Issues48 Questions

Exam 23: Associates and Joint Ventures48 Questions

Exam 24: Investments in Joint Arrangements23 Questions

Exam 25: Insolvency and Liquidation46 Questions

Select questions type

Consider the following economic entity structure:

The direct non-controlling interest (DNCI)and indirect non-controlling interest (INCI)are as follows.

The direct non-controlling interest (DNCI)and indirect non-controlling interest (INCI)are as follows.

Free

(Short Answer)

4.9/5  (27)

(27)

Correct Answer: Verified

Verified

A

The NCI share of equity is calculated on the recorded equity of the subsidiary.

Free

(True/False)

5.0/5 (32)

Correct Answer:Verified

False

When a parent acquires an additional interest in a subsidiary,the change in ownership interest in account for as an adjustment against goodwill.

Free

(True/False)

4.8/5 (32)

Correct Answer:Verified

False

The process of consolidation is not affected by the fact that acquisitions of subsidiaries may be non-sequential.

(True/False)

4.8/5 (31)

Alpha Limited acquired shares in Bravo Limited.At the time of this acquisition Bravo Limited already held shares in Charlie Limited.This form of acquisition of an indirect ownership interest,by Alpha Limited in Charlie Limited,is known as a/an:

(Multiple Choice)

4.8/5 (38)

In a group that has a multiple subsidiary structure,the direct non-controlling interest is entitled to:

(Multiple Choice)

4.9/5 (34)

When calculating the direct non-controlling interest share of equity,consolidation adjustments are needed to:

(Multiple Choice)

4.9/5 (29)

The calculation of the direct NCI share of equity is the same as that for the indirect NCI share of equity.

(True/False)

4.9/5 (40)

Reciprocal shareholdings exist when a parent and a subsidiary own shares in each other.

(True/False)

4.8/5 (35)

Which of the following can result in a loss of control by a parent over a subsidiary?

(Multiple Choice)

4.8/5 (29)

In a multiple subsidiary structure,the direct non-controlling interest is entitled to a proportionate share of:

(Multiple Choice)

4.8/5 (38)

Caloundra Limited has an 85% ownership interest in Minchinton Limited.Minchinton Limited has a 55% ownership interest in Moreton Limited.As a result of these ownership interests,there is a direct ownership interest in Moreton Limited amounting to:

(Multiple Choice)

4.9/5 (29)

The indirect NCI is entitled to a share of all movements in reserve accounts.

(True/False)

4.8/5 (37)

In a multiple subsidiary structure,the indirect non-controlling interest is entitled to a proportionate share of:

(Multiple Choice)

4.7/5 (31)

The direct NCI receives a proportionate share of both pre and post-acquisition equity of the subsidiary.

(True/False)

4.9/5 (43)

In non-sequential acquisitions,one of the assets of the acquired subsidiary for which the carrying amount may differ from fair value is its investments in its subsidiaries.

(True/False)

4.9/5 (27)

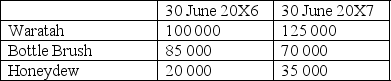

Waratah Ltd acquired a 60% ownership interest in Bottle Brush Ltd on 30 June 20X5.On the same day,Bottle Brush Ltd acquired a 70% ownership interest in Honeydew Ltd.

The following interentity transactions have taken place between the entities in the group during the years ended 30 June 20X6 and 30 June 20X7.

On 1 July 20X5 Bottle Brush sold an item of plant to Honeydew for a profit of $20 000.The remaining useful life of the plant at the date of transfer was 4 years.

On 1 September 20X5,Honeydew paid a dividend of $70 000 from profits earned since 30 June 20X5.

Waratah lent $50 000 to Bottle Brush on 1 January 20X6.Interest charged on the loan for the year ended 30 June 20X6 was $2000 and for the year ended 30 June 20X7 was $4000.

On 31 May 20X6 Waratah sold inventory to Honeydew for $15 000.Profit earned on the sale was $5000.Honeydew sold the inventory to external parties on 1 August 20X6.

Details of profits earned by entities within the group for the years ended 30 June 20X6 and 30 June 20X7 are:

The tax rate is 30%.

The NCI share of profit in Bottle Brush for the year ended 30 June 20X6 is:

The tax rate is 30%.

The NCI share of profit in Bottle Brush for the year ended 30 June 20X6 is:

(Multiple Choice)

4.7/5 (33)

Consider the following economic entity structure.

60%

The indirect NCI in B Ltd is the same group of shareholders as the:

60%

The indirect NCI in B Ltd is the same group of shareholders as the:

(Multiple Choice)

4.9/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)