Exam 6: Inventories and Cost of Sales

Exam 1: Accounting in Business240 Questions

Exam 2: Analyzing and Recording Transactions197 Questions

Exam 3: Adjusting Accounts and Preparing Financial Statements224 Questions

Exam 4: Completing the Accounting Cycle176 Questions

Exam 5: Accounting for Merchandising Operations198 Questions

Exam 6: Inventories and Cost of Sales198 Questions

Exam 7: Accounting Information Systems176 Questions

Exam 8: Cash and Internal Controls196 Questions

Exam 9: Accounting for Receivables191 Questions

Exam 10: Plant Assets, Natural Resources, and Intangibles223 Questions

Exam 11: Current Liabilities and Payroll Accounting193 Questions

Exam 12: Accounting for Partnerships139 Questions

Exam 13: Accounting for Corporations246 Questions

Exam 14: Long-Term Liabilities198 Questions

Exam 15: Investments and International Operations192 Questions

Exam 16: Reporting the Statement of Cash Flows187 Questions

Exam 17: Analysis of Financial Statements187 Questions

Exam 18: Managerial Accounting Concepts and Principles197 Questions

Exam 19: Job Order Cost Accounting164 Questions

Exam 20: Process Cost Accounting174 Questions

Exam 21: Cost Allocation and Performance Measurement170 Questions

Exam 22: Cost-Volume-Profit Analysis186 Questions

Exam 23: Master Budgets and Planning162 Questions

Exam 24: Flexible Budgets and Standard Costs174 Questions

Exam 25: Capital Budgeting and Managerial Decisions150 Questions

Exam 26: Time Value of Money60 Questions

Select questions type

Fast Auto Parts is an auto parts wholesaler that stocks several major brand names for Complete Auto Parts stores across the country. Complete Auto Parts does not assume responsibility for parts until they are sold to the customer. Identify the consignor and the consignee. Which company should include any unsold goods as part of its inventory?

(Essay)

4.8/5  (36)

(36)

If the _______________ is responsible for paying the freight, ownership of merchandise inventory passes when the goods arrive at their destination.

(Short Answer)

4.9/5 (44)

Jackson Company has sales of $300,000 and cost of goods available for sale of $270,000. If the gross profit ratio is typically 30%, the estimated cost of the ending inventory under the gross profit method would be:

(Multiple Choice)

5.0/5 (35)

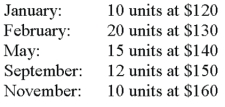

A company had the following purchases during the current year:  On December 31, there were 26 units remaining in ending inventory. These 26 units consisted of 2 from January, 4 from February, 6 from May, 4 from September, and 10 from November. Using the specific identification method, what is the cost of the ending inventory?

On December 31, there were 26 units remaining in ending inventory. These 26 units consisted of 2 from January, 4 from February, 6 from May, 4 from September, and 10 from November. Using the specific identification method, what is the cost of the ending inventory?

(Multiple Choice)

4.9/5 (37)

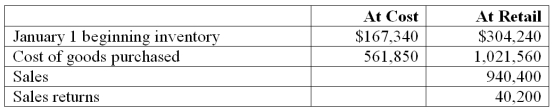

A company uses the retail inventory method and has the following information available concerning its most recent accounting period:  1. Use the retail inventory method to estimate the company's year-end inventory at cost.

2. A year-end physical count at retail prices yields a total inventory of $404,800. Prepare a calculation showing the company's loss from shrinkage at cost and at retail.

1. Use the retail inventory method to estimate the company's year-end inventory at cost.

2. A year-end physical count at retail prices yields a total inventory of $404,800. Prepare a calculation showing the company's loss from shrinkage at cost and at retail.

(Not Answered)

This question doesn't have any answer yet

The costs of goods purchased will vary under the different inventory methods of specific identification, FIFO, LIFO, and weighted average.

(True/False)

4.9/5 (34)

Internal controls that should be applied when a business takes a physical count of inventory should include all of the following except:

(Multiple Choice)

4.9/5 (40)

A company had inventory on November 1 of 5 units at a cost of $20 each. On November 2, they purchased 10 units at $22 each. On November 6 they purchased 6 units at $25 each. On November 8, 8 units were sold for $55 each. Using the LIFO perpetual inventory method, what was the value of the inventory on November 8 after the sale?

(Multiple Choice)

4.9/5 (38)

Goods on consignment are goods that are shipped by the owner, called the ______________, to another party called the _____________________.

(Short Answer)

4.8/5 (32)

All of the following statements regarding U.S. GAAP and IFRS are true except?

(Multiple Choice)

4.9/5 (41)

The inventory valuation method that results in the lowest taxable income in a period of inflation is:

(Multiple Choice)

4.9/5 (35)

The consistency concept prescribes that a company use the same accounting methods period after period, so that financial statements are comparable across periods.

(True/False)

4.9/5 (35)

The assignment of costs to cost of goods sold and inventory using weighted average usually yields different results depending on whether a perpetual or periodic system is used.

(True/False)

4.9/5 (32)

Companies are allowed to use FIFO for financial reporting and LIFO for tax reporting, according to IRS requirements.

(True/False)

4.9/5 (42)

The assignment of costs to the cost of goods sold and to ending inventory using FIFO is the same for both the perpetual and periodic inventory systems.

(True/False)

4.9/5 (43)

To avoid the time-consuming process of taking an inventory each year, most companies use the gross profit method to estimate ending inventory.

(True/False)

4.8/5 (32)

When applying the lower of cost or market method of inventory valuation, market is defined as the _____________________.

(Short Answer)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)