Exam 25: Macroeconomic Viewpoints: New Keynesian, Monetarist, and New Classical

Exam 1: Economics: The World Around You90 Questions

Exam 2: Choice, Opportunity Costs, and Specialization94 Questions

Exam 3: Markets, Demand and Supply, and the Price System97 Questions

Exam 5: The Market System and the Private and Public Sector97 Questions

Exam 4: Elasticity: Demand and Supply126 Questions

Exam 6: National Income Accounting104 Questions

Exam 7: an Introduction to the Foreign Exchange Market and the Balance of Payments90 Questions

Exam 8: Consumer Choice132 Questions

Exam 9: Supply: The Costs of Doing Business106 Questions

Exam 10: Unemployment and Inflation129 Questions

Exam 11: Macroeconomic Equilibrium: Aggregate Demand and Supply122 Questions

Exam 12: Profit Maximization122 Questions

Exam 13: Aggregate Expenditures115 Questions

Exam 14: Perfect Competition135 Questions

Exam 15: Income and Expenditures Equilibrium134 Questions

Exam 16: Monopoly118 Questions

Exam 17: Fiscal Policy93 Questions

Exam 18: Monopolistic Competition and Oligopoly111 Questions

Exam 19: Antitrust and Regulation100 Questions

Exam 10: Money and Banking125 Questions

Exam 21: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 22: Monetary Policy141 Questions

Exam 23: Macroeconomic Policy: Tradeoffs, Expectations, Credibility, and Sources of Business Cycles112 Questions

Exam 24: Resource Markets112 Questions

Exam 25: Macroeconomic Viewpoints: New Keynesian, Monetarist, and New Classical99 Questions

Exam 26: The Labor Market114 Questions

Exam 27: Capital Markets100 Questions

Exam 28: Economic Growth99 Questions

Exam 29: Development Economics104 Questions

Exam 30: the Land Market and Natural Resources55 Questions

Exam 31: Aging, Social Security and Health Care88 Questions

Exam 32: Globalization84 Questions

Exam 33: Elasticity: Demand and Supply126 Questions

Exam 34: Income Distribution, Poverty and Government Policy115 Questions

Exam 35: World Trade Equilibrium112 Questions

Exam 36: Consumer Choice132 Questions

Exam 37: International Trade Restrictions109 Questions

Exam 38: World Trade Equilibrium112 Questions

Exam 39: Exchange Rates and Financial Links Between Countries132 Questions

Exam 40: International Trade Restrictions109 Questions

Exam 41: Supply: the Costs of Doing Business106 Questions

Exam 42: Exchange Rates and Financial Links Between Countries132 Questions

Exam 43: Profit Maximization122 Questions

Exam 44: Perfect Competition135 Questions

Exam 45: Monopoly118 Questions

Exam 46: Monopolistic Competition and Oligopoly111 Questions

Exam 47: Antitrust and Regulation100 Questions

Exam 48: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 49: Resource Markets112 Questions

Exam 50: The Labor Market114 Questions

Exam 51: Capital Markets100 Questions

Exam 52: The Land Market and Natural Resources55 Questions

Exam 53: Aging, Social Security and Health Care87 Questions

Exam 54: Income Distribution, Poverty and Government Policy115 Questions

Exam 55: World Trade Equilibrium112 Questions

Exam 56: International Trade Restrictions109 Questions

Exam 57: Exchange Rates and Financial Links Between Countries132 Questions

Select questions type

"The dramatic reduction of the money supply during the 1930s was responsible for the Great Depression.The macroeconomy is intrinsically stable if left alone by the prying hand of government.The Federal Reserve Board, instead of tightening money during booms and loosening money during recessions (policies that are ineffective due to time lags), should simply increase the supply of money at a steady rate of 3 to 5 percent per year." This statement reflects which school of thought?

(Multiple Choice)

4.8/5  (41)

(41)

Which of the following schools of thought reject the simple fixed-price model in favor of a model in which the aggregate supply curve is relatively flat at low levels of real GDP and slopes upward as real GDP approaches its potential level?

(Multiple Choice)

4.9/5 (42)

Milton Friedman is widely considered to be the father of monetarism.

(True/False)

4.8/5 (35)

According to the new classical school, an expected increase in government spending is associated with:

(Multiple Choice)

4.9/5 (30)

Which of the following schools of thought stressed on a fixed-price model for macroeconomic equilibrium?

(Multiple Choice)

4.8/5 (37)

The flat region of the aggregate supply curve reflects the Keynesian belief that:

(Multiple Choice)

4.8/5 (38)

The monetarist assumption that monetary policy cannot change long-run equilibrium income is based on the idea that:

(Multiple Choice)

4.8/5 (37)

Which school calls for more information from policymakers so that people can incorporate government plans into their outlook for the future?

(Multiple Choice)

4.8/5 (41)

New classical economics assumes that government has direct control over the equilibrium level of GDP and indirect control over the money supply.

(True/False)

4.9/5 (42)

Traditional Keynesian economics assumes that prices are relatively flexible in response to changes in aggregate expenditures.

(True/False)

4.8/5 (44)

The assumption of wage and price flexibility lead classical economists to conclude that business cycle fluctuations are short-term in nature.

(True/False)

4.9/5 (31)

The economic theory that suggested an alternative to the rising unemployment and inflation that the static Phillips curve analysis could not explain was the:

(Multiple Choice)

4.9/5 (35)

According to the new Keynesian school of thought, fiscal policy is a completely ineffective tool in combating supply-side shocks.

(True/False)

4.8/5 (32)

According to the new classical school, if macroeconomic policy is perfectly expected, then the aggregate supply curve and the Phillips curve must be vertical in both the short run and the long run.

(True/False)

4.9/5 (39)

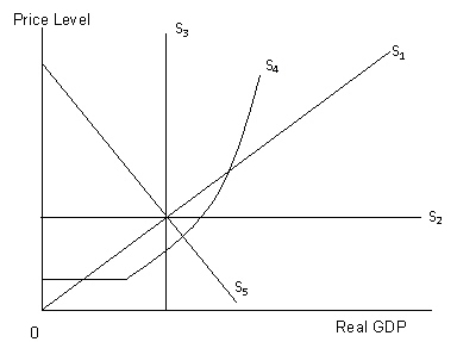

The figure given below shows the supply curves with different slopes. Figure 15.1  Refer to Figure 15.1.Which of the following supply curves represents the supply curve in the simple Keynesian model?

Refer to Figure 15.1.Which of the following supply curves represents the supply curve in the simple Keynesian model?

(Multiple Choice)

4.9/5 (38)

According to the traditional classical school of thought, aggregate supply is vertical both in the short run and in the long run.

(True/False)

4.9/5 (40)

Monetarists believe that discretionary monetary policy, and not discretionary fiscal policy, should be used to correct disequilibrium.

(True/False)

4.8/5 (39)

New classical economists contend that both the short-run and long-run aggregate supply curves are vertical.

(True/False)

4.7/5 (36)

Monetarists argue that government actions, particularly monetary policy, worsens the negative aspects of the business cycle.

(True/False)

4.9/5 (23)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)