Exam 11: Macroeconomic Equilibrium: Aggregate Demand and Supply

Exam 1: Economics: The World Around You90 Questions

Exam 2: Choice, Opportunity Costs, and Specialization94 Questions

Exam 3: Markets, Demand and Supply, and the Price System97 Questions

Exam 5: The Market System and the Private and Public Sector97 Questions

Exam 4: Elasticity: Demand and Supply126 Questions

Exam 6: National Income Accounting104 Questions

Exam 7: an Introduction to the Foreign Exchange Market and the Balance of Payments90 Questions

Exam 8: Consumer Choice132 Questions

Exam 9: Supply: The Costs of Doing Business106 Questions

Exam 10: Unemployment and Inflation129 Questions

Exam 11: Macroeconomic Equilibrium: Aggregate Demand and Supply122 Questions

Exam 12: Profit Maximization122 Questions

Exam 13: Aggregate Expenditures115 Questions

Exam 14: Perfect Competition135 Questions

Exam 15: Income and Expenditures Equilibrium134 Questions

Exam 16: Monopoly118 Questions

Exam 17: Fiscal Policy93 Questions

Exam 18: Monopolistic Competition and Oligopoly111 Questions

Exam 19: Antitrust and Regulation100 Questions

Exam 10: Money and Banking125 Questions

Exam 21: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 22: Monetary Policy141 Questions

Exam 23: Macroeconomic Policy: Tradeoffs, Expectations, Credibility, and Sources of Business Cycles112 Questions

Exam 24: Resource Markets112 Questions

Exam 25: Macroeconomic Viewpoints: New Keynesian, Monetarist, and New Classical99 Questions

Exam 26: The Labor Market114 Questions

Exam 27: Capital Markets100 Questions

Exam 28: Economic Growth99 Questions

Exam 29: Development Economics104 Questions

Exam 30: the Land Market and Natural Resources55 Questions

Exam 31: Aging, Social Security and Health Care88 Questions

Exam 32: Globalization84 Questions

Exam 33: Elasticity: Demand and Supply126 Questions

Exam 34: Income Distribution, Poverty and Government Policy115 Questions

Exam 35: World Trade Equilibrium112 Questions

Exam 36: Consumer Choice132 Questions

Exam 37: International Trade Restrictions109 Questions

Exam 38: World Trade Equilibrium112 Questions

Exam 39: Exchange Rates and Financial Links Between Countries132 Questions

Exam 40: International Trade Restrictions109 Questions

Exam 41: Supply: the Costs of Doing Business106 Questions

Exam 42: Exchange Rates and Financial Links Between Countries132 Questions

Exam 43: Profit Maximization122 Questions

Exam 44: Perfect Competition135 Questions

Exam 45: Monopoly118 Questions

Exam 46: Monopolistic Competition and Oligopoly111 Questions

Exam 47: Antitrust and Regulation100 Questions

Exam 48: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 49: Resource Markets112 Questions

Exam 50: The Labor Market114 Questions

Exam 51: Capital Markets100 Questions

Exam 52: The Land Market and Natural Resources55 Questions

Exam 53: Aging, Social Security and Health Care87 Questions

Exam 54: Income Distribution, Poverty and Government Policy115 Questions

Exam 55: World Trade Equilibrium112 Questions

Exam 56: International Trade Restrictions109 Questions

Exam 57: Exchange Rates and Financial Links Between Countries132 Questions

Select questions type

In the long run, increased government spending is ineffective in raising equilibrium real GDP.

Free

(True/False)

4.7/5  (33)

(33)

Correct Answer: Verified

Verified

True

Which of the following economic changes will decrease household expenditures?

Free

(Multiple Choice)

4.9/5 (36)

Correct Answer:Verified

E

In the long run, increased consumption spending raises only the price level.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

True

Which of the following would result in a decrease in aggregate demand?

(Multiple Choice)

5.0/5 (41)

Suppose the long-run aggregate supply curve shifts to the right as a consequence of the discovery of more efficient production technologies.Given unchanged aggregate expenditure, this implies a rise in long-run equilibrium output and a decline in the equilibrium price level.

(True/False)

4.9/5 (30)

Other things equal, an increase in aggregate supply will cause:

(Multiple Choice)

4.9/5 (34)

Assuming a fixed exchange rate, a decrease in U.S.prices relative to European prices will:

(Multiple Choice)

4.8/5 (39)

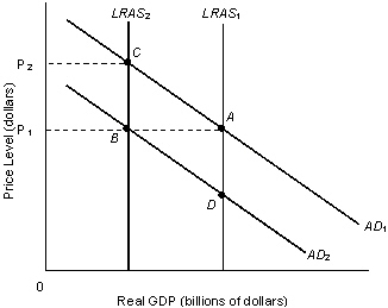

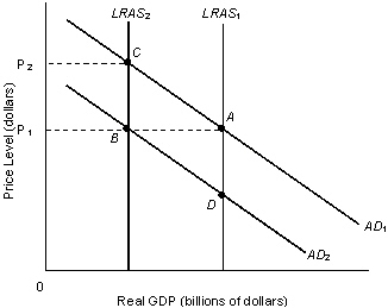

The figure given below represents the long-run equilibrium in the aggregate demand and aggregate supply model. Figure 8.2  Refer to Figure 8.2.The combination of rising prices and falling output is known as stagflation.This phenomenon is represented by which of the following shifts?

Refer to Figure 8.2.The combination of rising prices and falling output is known as stagflation.This phenomenon is represented by which of the following shifts?

(Multiple Choice)

4.7/5 (40)

The figure given below represents the long-run equilibrium in the aggregate demand and aggregate supply model. Figure 8.2  Refer to Figure 8.2.A movement from equilibrium point A to equilibrium point B would be the result of a(n):

Refer to Figure 8.2.A movement from equilibrium point A to equilibrium point B would be the result of a(n):

(Multiple Choice)

4.7/5 (36)

If a large number of laborers shift from fixed-wage contracts to wages that depend on the cost of living adjustments, the long-run aggregate supply curve for the economy will become relatively steeper.

(True/False)

4.9/5 (39)

Assume that the AD curve is held constant and short-run aggregate supply decreases.The result is a(n):

(Multiple Choice)

4.8/5 (31)

When the foreign price level falls, domestic goods become more expensive relative to foreign goods, causing domestic net exports and aggregate demand to fall.

(True/False)

4.9/5 (46)

What happens to aggregate supply when production costs adjust completely to price increases?

(Multiple Choice)

4.9/5 (44)

The aggregate quantity of goods and services produced will decrease at every price level when resource price rises.

(True/False)

4.7/5 (36)

The long-run aggregate supply of an economy at the potential level of real GDP is graphically represented by:

(Multiple Choice)

4.7/5 (38)

Lower interest rates on business loans usually result in a(n):

(Multiple Choice)

4.8/5 (43)

Which of the following is not held constant in the short run when determining the aggregate supply curve?

(Multiple Choice)

4.9/5 (36)

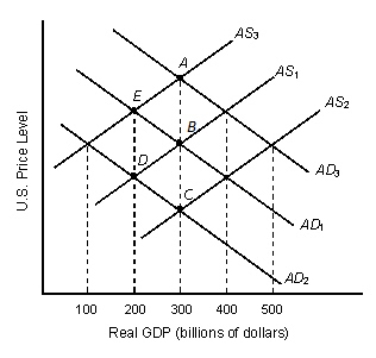

The figure given below represents the equilibrium real GDP and price level in the aggregate demand and aggregate supply model. Figure 8.3  Refer to Figure 8.3.If AS1 and AD1 represent the initial aggregate demand and supply in the economy, the long-run equilibrium real GDP will be _____ billion.

Refer to Figure 8.3.If AS1 and AD1 represent the initial aggregate demand and supply in the economy, the long-run equilibrium real GDP will be _____ billion.

(Multiple Choice)

4.8/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)