Exam 25: Macroeconomic Viewpoints: New Keynesian, Monetarist, and New Classical

Exam 1: Economics: The World Around You90 Questions

Exam 2: Choice, Opportunity Costs, and Specialization94 Questions

Exam 3: Markets, Demand and Supply, and the Price System97 Questions

Exam 5: The Market System and the Private and Public Sector97 Questions

Exam 4: Elasticity: Demand and Supply126 Questions

Exam 6: National Income Accounting104 Questions

Exam 7: an Introduction to the Foreign Exchange Market and the Balance of Payments90 Questions

Exam 8: Consumer Choice132 Questions

Exam 9: Supply: The Costs of Doing Business106 Questions

Exam 10: Unemployment and Inflation129 Questions

Exam 11: Macroeconomic Equilibrium: Aggregate Demand and Supply122 Questions

Exam 12: Profit Maximization122 Questions

Exam 13: Aggregate Expenditures115 Questions

Exam 14: Perfect Competition135 Questions

Exam 15: Income and Expenditures Equilibrium134 Questions

Exam 16: Monopoly118 Questions

Exam 17: Fiscal Policy93 Questions

Exam 18: Monopolistic Competition and Oligopoly111 Questions

Exam 19: Antitrust and Regulation100 Questions

Exam 10: Money and Banking125 Questions

Exam 21: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 22: Monetary Policy141 Questions

Exam 23: Macroeconomic Policy: Tradeoffs, Expectations, Credibility, and Sources of Business Cycles112 Questions

Exam 24: Resource Markets112 Questions

Exam 25: Macroeconomic Viewpoints: New Keynesian, Monetarist, and New Classical99 Questions

Exam 26: The Labor Market114 Questions

Exam 27: Capital Markets100 Questions

Exam 28: Economic Growth99 Questions

Exam 29: Development Economics104 Questions

Exam 30: the Land Market and Natural Resources55 Questions

Exam 31: Aging, Social Security and Health Care88 Questions

Exam 32: Globalization84 Questions

Exam 33: Elasticity: Demand and Supply126 Questions

Exam 34: Income Distribution, Poverty and Government Policy115 Questions

Exam 35: World Trade Equilibrium112 Questions

Exam 36: Consumer Choice132 Questions

Exam 37: International Trade Restrictions109 Questions

Exam 38: World Trade Equilibrium112 Questions

Exam 39: Exchange Rates and Financial Links Between Countries132 Questions

Exam 40: International Trade Restrictions109 Questions

Exam 41: Supply: the Costs of Doing Business106 Questions

Exam 42: Exchange Rates and Financial Links Between Countries132 Questions

Exam 43: Profit Maximization122 Questions

Exam 44: Perfect Competition135 Questions

Exam 45: Monopoly118 Questions

Exam 46: Monopolistic Competition and Oligopoly111 Questions

Exam 47: Antitrust and Regulation100 Questions

Exam 48: Market Failures, Government Failures, and Rent Seeking121 Questions

Exam 49: Resource Markets112 Questions

Exam 50: The Labor Market114 Questions

Exam 51: Capital Markets100 Questions

Exam 52: The Land Market and Natural Resources55 Questions

Exam 53: Aging, Social Security and Health Care87 Questions

Exam 54: Income Distribution, Poverty and Government Policy115 Questions

Exam 55: World Trade Equilibrium112 Questions

Exam 56: International Trade Restrictions109 Questions

Exam 57: Exchange Rates and Financial Links Between Countries132 Questions

Select questions type

The primary difference between new Keynesian economics and traditional Keynesian economics is that the former is more realistic about international trade, whereas the latter stresses the importance of inward oriented strategies.

(True/False)

4.8/5  (41)

(41)

Which of the following economic theories became popular in the 1930s in response to the shortcomings of existing theories of the Great Depression?

(Multiple Choice)

4.8/5 (28)

_____ have faith in the free market (price)system that leads them to favor minimal government intervention.

(Multiple Choice)

4.9/5 (41)

Which of the following macroeconomic schools of thought had dominated the economics profession from the 1940s through the 1960s?

(Multiple Choice)

4.8/5 (42)

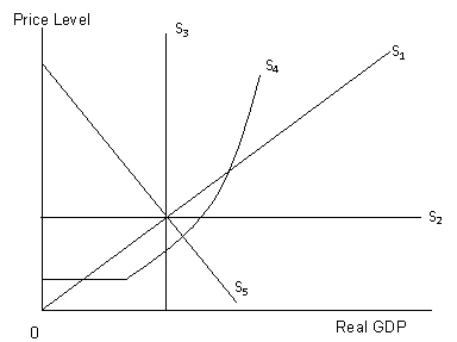

The figure given below shows the supply curves with different slopes. Figure 15.1  Refer to Figure 15.1.Which of the following supply curves represents the supply curve described by the modern Keynesians?

Refer to Figure 15.1.Which of the following supply curves represents the supply curve described by the modern Keynesians?

(Multiple Choice)

4.9/5 (45)

Which of the following school of thought believes that the major source of the macroeconomic problems are the disequilibria in the private labor and goods market?

(Multiple Choice)

4.9/5 (34)

An economist from which school of thought would most likely accept the following- "The wide acceptance and practice of activist government fiscal policy."

(Multiple Choice)

4.7/5 (37)

Monetarists believe that changes in monetary policy would have:

(Multiple Choice)

4.9/5 (37)

New classical economists contend that an unexpected increase in the money supply will:

(Multiple Choice)

4.8/5 (34)

In case of classical model, increase in aggregate expenditure would:

(Multiple Choice)

4.8/5 (42)

An economist from which school of thought would be most likely to say the following- "An increase in government expenditure will only increase inflation, because the aggregate supply curve is vertical."

(Multiple Choice)

4.8/5 (32)

A by-product of the acceptance of the Keynesian school was the wide approval and practice of activist fiscal policy around the world.

(True/False)

4.8/5 (36)

Which of the following schools of thought emphasize the role of money supply in determining equilibrium real GDP and price level?

(Multiple Choice)

4.7/5 (35)

Monetaristsargue that the long-run Phillips curve is negatively sloped.

(True/False)

4.7/5 (37)

Reaction lag is the term used to express the fact that some time passes before changes in the money supply are properly translated into changes in real GDP.

(True/False)

4.9/5 (44)

According to new classical school of economics, the aggregate supply curve is:

(Multiple Choice)

4.8/5 (42)

The main reason why the traditional classical school ceased to be widely accepted was that:

(Multiple Choice)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)