Exam 5: Risk, Return, and the Historical Record

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

The dollar-weighted return is the ________.

Free

(Multiple Choice)

4.7/5  (24)

(24)

Correct Answer: Verified

Verified

D

Which measure of downside risk predicts the worst loss that will be suffered with a given probability?

Free

(Multiple Choice)

4.7/5 (34)

Correct Answer:Verified

C

The reward-to-volatility ratio is given by ________.

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

A

What is the VaR of a $10 million portfolio with normally distributed returns at the 5% VaR? Assume the expected return is 13% and the standard deviation is 20%.

(Multiple Choice)

4.7/5 (30)

You are considering investing $1,000 in a complete portfolio. The complete portfolio is composed of Treasury bills that pay 5% and a risky portfolio, P, constructed with two risky securities, X and Y. The optimal weights of X and Y in P are 60% and 40% respectively. X has an expected rate of return of 14%, and Y has an expected rate of return of 10%. To form a complete portfolio with an expected rate of return of 8%, you should invest approximately ________ in the risky portfolio. This will mean you will also invest approximately ________ and ________ of your complete portfolio in security X and Y, respectively.

(Multiple Choice)

4.7/5 (34)

Consider the following two investment alternatives: First, a risky portfolio that pays a 15% rate of return with a probability of 40% or a 5% rate of return with a probability of 60%. Second, a Treasury bill that pays 6%. The risk premium on the risky investment is ________.

(Multiple Choice)

4.7/5 (25)

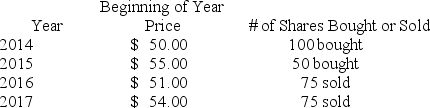

You have the following rates of return for a risky portfolio for several recent years. Assume that the stock pays no dividends.

What is the dollar-weighted return over the entire time period?

What is the dollar-weighted return over the entire time period?

(Multiple Choice)

4.8/5 (35)

If you want to measure the performance of your investment in a fund, including the timing of your purchases and redemptions, you should calculate the ________.

(Multiple Choice)

4.7/5 (31)

You invest $1,000 in a complete portfolio. The complete portfolio is composed of a risky asset with an expected rate of return of 16% and a standard deviation of 20% and a Treasury bill with a rate of return of 6%. The slope of the capital allocation line formed with the risky asset and the risk-free asset is approximately ________.

(Multiple Choice)

4.9/5 (35)

During the 1926-2013 period the geometric mean return on Treasury bonds was ________.

(Multiple Choice)

4.9/5 (34)

Rank the following from highest average historical standard deviation to lowest average historical standard deviation from 1926 to 2017.

I. Small stocks

II. Long-term bonds

III. Large stocks

IV. T-bills

(Multiple Choice)

4.9/5 (39)

The holding-period return on a stock was 32%. Its beginning price was $25, and its cash dividend was $1.50. Its ending price must have been ________.

(Multiple Choice)

4.9/5 (34)

Most studies indicate that investors' risk aversion is in the range ________.

(Multiple Choice)

4.8/5 (32)

During the 1926-2013 period the Sharpe ratio was greatest for which of the following asset classes?

(Multiple Choice)

4.9/5 (37)

The complete portfolio refers to the investment in ________.

(Multiple Choice)

4.8/5 (34)

You have calculated the historical dollar-weighted return, annual geometric average return, and annual arithmetic average return. If you desire to forecast performance for next year, the best forecast will be given by the ________.

(Multiple Choice)

4.9/5 (45)

Which one of the following would be considered a risk-free asset in real terms as opposed to nominal?

(Multiple Choice)

4.8/5 (27)

Historical returns have generally been ________ for stocks of small firms as (than) for stocks of large firms.

(Multiple Choice)

4.9/5 (36)

You are considering investing $1,000 in a complete portfolio. The complete portfolio is composed of Treasury bills that pay 5% and a risky portfolio, P, constructed with two risky securities, X and Y. The optimal weights of X and Y in P are 60% and 40%, respectively. X has an expected rate of return of 14%, and Y has an expected rate of return of 10%. To form a complete portfolio with an expected rate of return of 11%, you should invest ________ of your complete portfolio in Treasury bills.

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)