Exam 6: Efficient Diversification

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns of A and B is .4. The risk-free rate of return is 5%. The expected return on the optimal risky portfolio is approximately ________. (Hint: Find weights first.)

Free

(Multiple Choice)

4.8/5  (37)

(37)

Correct Answer: Verified

Verified

B

The ________ decision should take precedence over the ________ decision.

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

A

A project has a 60% chance of doubling your investment in 1 year and a 40% chance of losing half your money. What is the standard deviation of this investment?

Free

(Multiple Choice)

4.8/5 (32)

Correct Answer:Verified

D

You are considering adding a new security to your portfolio. To decide whether you should add the security, you need to know the security's:

I. Expected return

II. Standard deviation

III. Correlation with your portfolio

(Multiple Choice)

4.9/5 (34)

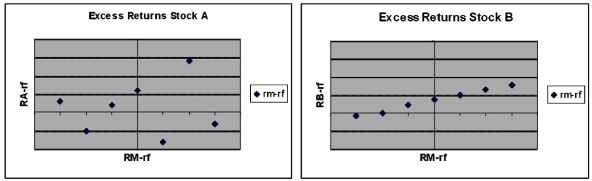

The figures below show plots of monthly excess returns for two stocks plotted against excess returns for a market index.  Which stock is riskier to a nondiversified investor who puts all his money in only one of these stocks?

Which stock is riskier to a nondiversified investor who puts all his money in only one of these stocks?

(Multiple Choice)

4.8/5 (29)

Investing in two assets with a correlation coefficient of -.5 will reduce what kind of risk?

(Multiple Choice)

4.9/5 (40)

The market value weighted-average beta of firms included in the market index will always be ________.

(Multiple Choice)

4.7/5 (29)

Asset A has an expected return of 15% and a reward-to-variability ratio of .4. Asset B has an expected return of 20% and a reward-to-variability ratio of .3. A risk-averse investor would prefer a portfolio using the risk-free asset and ________.

(Multiple Choice)

4.8/5 (39)

Lear Corp. has an expected excess return of 8% next year. Assume Lear's beta is 1.43. If the economy booms and the stock market beats expectations by 5%, what was Lear's actual excess return?

(Multiple Choice)

4.9/5 (35)

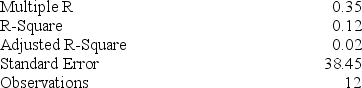

You run a regression for a stock's return on a market index and find the following Excel output:

The beta of this stock is ________.

The beta of this stock is ________.

(Multiple Choice)

4.9/5 (37)

Rational risk-averse investors will always prefer portfolios ________.

(Multiple Choice)

4.7/5 (32)

A portfolio is composed of two stocks, A and B. Stock A has a standard deviation of return of 35%, while stock B has a standard deviation of return of 15%. The correlation coefficient between the returns on A and B is .45. Stock A comprises 40% of the portfolio, while stock B comprises 60% of the portfolio. The standard deviation of the return on this portfolio is ________.

(Multiple Choice)

4.9/5 (30)

Which of the following statements is (are) true regarding time diversification?

I. The standard deviation of the average annual rate of return over several years will be smaller than the 1-year standard deviation.

II. For a longer time horizon, uncertainty compounds over a greater number of years.

III. Time diversification does not reduce risk.

(Multiple Choice)

4.8/5 (38)

Consider two perfectly negatively correlated risky securities, A and B. Security A has an expected rate of return of 16% and a standard deviation of return of 20%. B has an expected rate of return of 10% and a standard deviation of return of 30%. The weight of security B in the minimum-variance portfolio is ________.

(Multiple Choice)

4.7/5 (48)

Semitool Corp. has an expected excess return of 6% for next year. However, for every unexpected 1% change in the market, Semitool's return responds by a factor of 1.2. Suppose it turns out that the economy and the stock market do better than expected by 1.5% and Semitool's products experience more rapid growth than anticipated, pushing up the stock price by another 1%. Based on this information, what was Semitool's actual excess return?

(Multiple Choice)

4.8/5 (44)

On a standard expected return versus standard deviation graph, investors will prefer portfolios that lie to the ________ the current investment opportunity set.

(Multiple Choice)

4.9/5 (38)

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 21% and a standard deviation of return of 39%. Stock B has an expected return of 14% and a standard deviation of return of 20%. The correlation coefficient between the returns of A and B is .4. The risk-free rate of return is 5%. The proportion of the optimal risky portfolio that should be invested in stock B is approximately ________.

(Multiple Choice)

4.7/5 (24)

The term complete portfolio refers to a portfolio consisting of ________.

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)