Exam 18: Evaluating Investment Performance

Exam 1: Investments: Background and Issues79 Questions

Exam 2: Asset Classes and Financial Instruments85 Questions

Exam 3: Securities Markets94 Questions

Exam 4: Mutual Funds and Other Investment Companies90 Questions

Exam 5: Risk, Return, and the Historical Record89 Questions

Exam 6: Efficient Diversification89 Questions

Exam 7: Capital Asset Pricing and Arbitrage Pricing Theory89 Questions

Exam 8: The Efficient Market Hypothesis92 Questions

Exam 9: Behavioral Finance and Technical Analysis89 Questions

Exam 10: Bond Prices and Yields96 Questions

Exam 11: Managing Bond Portfolios90 Questions

Exam 12: Macroeconomic and Industry Analysis93 Questions

Exam 13: Equity Valuation94 Questions

Exam 14: Financial Statement Analysis88 Questions

Exam 15: Options Markets91 Questions

Exam 16: Option Valuation90 Questions

Exam 17: Futures Markets and Risk Management92 Questions

Exam 18: Evaluating Investment Performance78 Questions

Exam 19: International Diversification50 Questions

Exam 20: Hedge Funds65 Questions

Exam 21: Taxes, Inflation, and Investment Strategy74 Questions

Exam 22: Investors and the Investment Process86 Questions

Select questions type

Suppose a particular investment earns an arithmetic return of 10% in year 1, 20% in year 2, and 30% in year 3. The geometric average return for the period will be

Free

(Multiple Choice)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

C

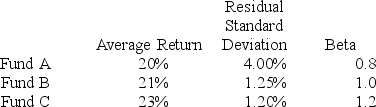

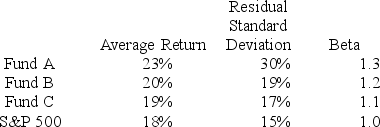

You want to evaluate three mutual funds using the information ratio measure for performance evaluation. The risk-free return during the sample period is 6%, and the average return on the market portfolio is 19%. The average returns, residual standard deviations, and betas for the three funds are given below.

The fund with the highest information ratio measure is

The fund with the highest information ratio measure is

Free

(Multiple Choice)

4.8/5 (28)

Correct Answer:Verified

B

The dollar-weighted return on a portfolio is equivalent to

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

D

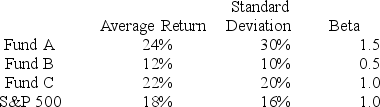

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 6%. The average returns, standard deviations, and betas for the three funds are given below, as are the data for the S&P 500 Index.

The fund with the highest Sharpe measure is

The fund with the highest Sharpe measure is

(Multiple Choice)

4.9/5 (31)

The following data are available relating to the performance of Monarch Stock Fund and the market portfolio:

The risk-free return during the sample period was 4%.

Calculate Treynor's measure of performance for Monarch Stock Fund.

The risk-free return during the sample period was 4%.

Calculate Treynor's measure of performance for Monarch Stock Fund.

(Multiple Choice)

4.8/5 (38)

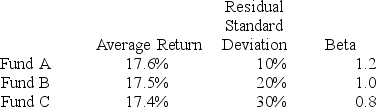

You want to evaluate three mutual funds using the Jensen measure for performance evaluation. The risk-free return during the sample period is 6%, and the average return on the market portfolio is 18%. The average returns, standard deviations, and betas for the three funds are given below.

The fund with the highest Jensen measure is

The fund with the highest Jensen measure is

(Multiple Choice)

4.9/5 (45)

Suppose two portfolios have the same average return and the same standard deviation of returns, but portfolio A has a lower beta than portfolio B. According to the Treynor measure, the performance of portfolio A

(Multiple Choice)

4.7/5 (36)

Studies of style analysis have found that ________ of fund returns can be explained by asset allocation alone.

(Multiple Choice)

4.8/5 (29)

Suppose you own two stocks, A and B. In year 1, stock A earns a 2% return and stock B earns a 9% return. In year 2, stock A earns an 18% return and stock B earns an 11% return. ________ has the higher arithmetic average return.

(Multiple Choice)

4.8/5 (36)

The Sharpe, Treynor, and Jensen portfolio performance measures are derived from the CAPM,

(Multiple Choice)

4.8/5 (25)

The following data are available relating to the performance of Seminole Fund and the market portfolio:

The risk-free return during the sample period was 6%.

Calculate the M2 measure for the Seminole Fund.

The risk-free return during the sample period was 6%.

Calculate the M2 measure for the Seminole Fund.

(Multiple Choice)

4.9/5 (40)

Hedge funds

I. are appropriate as a sole investment vehicle for an investor.

II. should only be added to an already well-diversified portfolio.

III. pose performance-evaluation issues due to nonlinear factor exposures.

IV. have down-market betas that are typically larger than up-market betas.

V. have symmetrical betas.

(Multiple Choice)

4.9/5 (29)

The following data are available relating to the performance of Wildcat Fund and the market portfolio:

The risk-free return during the sample period was 7%.

What is the information ratio measure of performance evaluation for Wildcat Fund?

The risk-free return during the sample period was 7%.

What is the information ratio measure of performance evaluation for Wildcat Fund?

(Multiple Choice)

4.8/5 (33)

Suppose you purchase 100 shares of GM stock at the beginning of year 1 and purchase another 100 shares at the end of year 1. You sell all 200 shares at the end of year 2. Assume that the price of GM stock is $50 at the beginning of year 1, $55 at the end of year 1, and $65 at the end of year 2. Assume no dividends were paid on GM stock. Your dollar-weighted return on the stock will be ________ your time-weighted return on the stock.

(Multiple Choice)

4.9/5 (31)

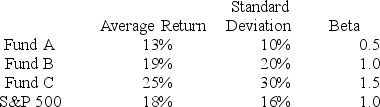

You want to evaluate three mutual funds using the Treynor measure for performance evaluation. The risk-free return during the sample period is 6%. The average returns, standard deviations, and betas for the three funds are given below, in addition to information regarding the S&P 500 Index.

The fund with the highest Treynor measure is

The fund with the highest Treynor measure is

(Multiple Choice)

4.8/5 (39)

Mutual funds show ________ evidence of serial correlation, and hedge funds show ________ evidence of serial correlation.

(Multiple Choice)

4.9/5 (34)

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 5%. The average returns, standard deviations, and betas for the three funds are given below, as are the data for the S&P 500 Index.

The investment with the highest Sharpe measure is

The investment with the highest Sharpe measure is

(Multiple Choice)

4.9/5 (34)

In a particular year, Razorback Mutual Fund earned a return of 1% by making the following investments in asset classes:

The return on a bogey portfolio was 2%, calculated from the following information.

The return on a bogey portfolio was 2%, calculated from the following information.

The total excess return on the Razorback Fund's managed portfolio was

The total excess return on the Razorback Fund's managed portfolio was

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)