Exam 5: Elasticity and Its Application

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

Supply is said to be inelastic if the quantity supplied responds substantially to changes in the price and elastic if the quantity supplied responds only slightly to price.

(True/False)

4.8/5  (42)

(42)

Suppose demand is given by the equation:  At what price will total revenue be maximized?

At what price will total revenue be maximized?

(Essay)

4.8/5 (33)

For which of the following goods is the income elasticity of demand likely lowest?

(Multiple Choice)

4.8/5 (29)

Refer to Table 5-12. Between which two quantities listed is demand most elastic?

(Short Answer)

4.8/5 (33)

Cross-price elasticity is used to determine whether goods are inferior or normal goods.

(True/False)

4.8/5 (42)

For a particular good, a 3 percent increase in price causes a 10 percent decrease in quantity demanded. Which of the following statements is most likely applicable to this good?

(Multiple Choice)

4.8/5 (38)

When the price of candy bars is $1.00, the quantity demanded is 500 per day. When the price falls to $0.80, the quantity demanded increases to 600. Given this information and using the midpoint method, we know that the demand for candy bars is

(Multiple Choice)

4.9/5 (40)

The cross-price elasticity of garlic salt and onion salt is -2, which indicates that garlic salt and onion salt are substitutes.

(True/False)

4.9/5 (31)

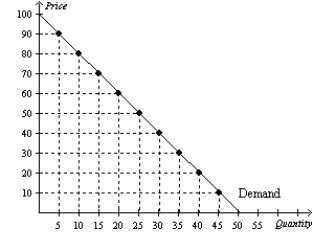

Figure 5-5  -Refer to Figure 5-5. Using the midpoint method, between prices of $50 and $60, price elasticity of demand is about

-Refer to Figure 5-5. Using the midpoint method, between prices of $50 and $60, price elasticity of demand is about

(Multiple Choice)

4.9/5 (36)

When the price of a bracelet was $28 each, the jewelry shop sold 128 per month. When it raised the price to $32 each, it sold 112 per month. Using the midpoint method, the price elasticity of demand for bracelets is

(Multiple Choice)

5.0/5 (33)

The demand for gasoline will respond more to a change in price over a period of five weeks than over a period of five years.

(True/False)

4.9/5 (31)

Suppose that 50 hot dogs are demanded at a particular price. If the price of hot dogs rises from that price by 5 percent, the number of hot dogs demanded falls to 48. Using the midpoint approach to calculate the price elasticity of demand, it follows that the

(Multiple Choice)

4.9/5 (32)

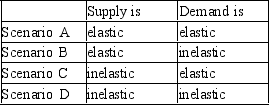

Table 5-11  -Refer to Table 5-11. Which scenario describes the market for oil in the short run?

-Refer to Table 5-11. Which scenario describes the market for oil in the short run?

(Multiple Choice)

4.9/5 (42)

Figure 5-3  -Refer to Figure 5-3. The demand curve representing the demand for a luxury good with several close substitutes is

-Refer to Figure 5-3. The demand curve representing the demand for a luxury good with several close substitutes is

(Multiple Choice)

4.7/5 (33)

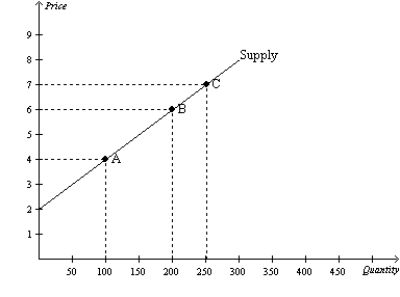

Figure 5-17  -Refer to Figure 5-17. Using the midpoint method, what is the price elasticity of supply between point B and point C?

-Refer to Figure 5-17. Using the midpoint method, what is the price elasticity of supply between point B and point C?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)