Exam 3: Process Costing and Analysis

Exam 1: Managerial Accounting Concepts and Principles251 Questions

Exam 2: Job Order Costing and Analysis216 Questions

Exam 3: Process Costing and Analysis231 Questions

Exam 4: Activity-Based Costing and Analysis223 Questions

Exam 5: Cost Behavior and Cost-Volume-Profit Analysis248 Questions

Exam 6: Variable Costing and Analysis202 Questions

Exam 7: Master Budgets and Performance Planning215 Questions

Exam 8: Flexible Budgets and Standard Costs221 Questions

Exam 9: Performance Measurement and Responsibility Accounting210 Questions

Exam 10: Relevant Costing for Managerial Decisions145 Questions

Exam 11: Capital Budgeting and Investment Analysis157 Questions

Exam 12: Reporting Cash Flows240 Questions

Exam 13: Analysis of Financial Statements235 Questions

Exam 14: Time Value of Money83 Questions

Exam 15: Lean Principles and Accounting27 Questions

Exam 16: Accounting for Business Transactions251 Questions

Select questions type

Which of the following is not one of the four steps in accounting for production activity and assigning costs during a period under a process cost system?

(Multiple Choice)

5.0/5  (37)

(37)

Following is a partial process cost summary for Mitchell Manufacturing's Canning Department.  If the units completed were transferred to the Labeling Department, what is the appropriate journal entry to transfer the conversion costs?

If the units completed were transferred to the Labeling Department, what is the appropriate journal entry to transfer the conversion costs?

(Multiple Choice)

4.8/5 (45)

Prepare general journal entries to record the following production activities for Oaks Manufacturing.

a. Purchased $82,000 of raw materials on credit.

b. Used $63,500 of direct materials in production.

c. Used $12,800 of indirect materials.

(Essay)

4.9/5 (27)

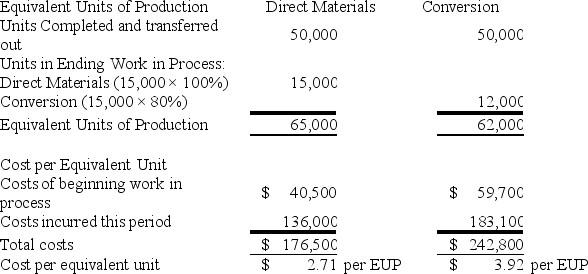

Refer to the following information about the Finishing Department in the Davidson Factory for the month of June. Davidson Factory uses the FIFO method of inventory costing.

Beginning Work in Process inventory:

Physical units…………………………………………... 5,000 units

% complete for materials………………………………. 70%

% complete for labor and overhead……………………. 25%

Materials cost from May……………………………….. $7,350

Labor and overhead cost from May……………………. $3,125

Product started and completed:

Physical units…………………………………………… 40,000 units

Ending Work in Process inventory:

Physical units………………………………………….... 4,000 units

% complete for materials………………………………. 40%

% complete for labor and overhead……………………. 10%

Manufacturing costs for June:

Materials………………………………………………… $96,975

Labor and overhead……………………………………... $79,470

Compute the equivalent cost per unit for direct materials, direct labor and overhead for June.

(Essay)

4.9/5 (33)

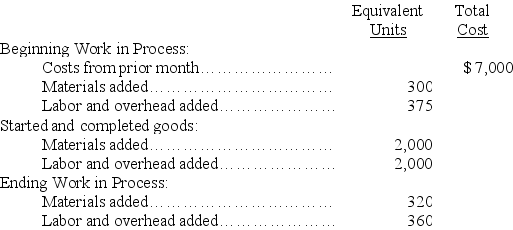

Refer to the following information about the Shaping Department of the Minnesota Factory for the month of August. Minnesota Factory uses the FIFO method of inventory costing.

The cost per equivalent unit of materials is $10.00, and the cost per equivalent unit of labor and overhead is $22.00.Prepare a cost reconciliation for the month of August.

The cost per equivalent unit of materials is $10.00, and the cost per equivalent unit of labor and overhead is $22.00.Prepare a cost reconciliation for the month of August.

(Essay)

4.9/5 (42)

A company uses the FIFO method for inventory costing. At the beginning of a period, the production department had 20,000 units in beginning Work in Process inventory which were 40% complete; the department completed and transferred 165,000 units. At the end of the period, 22,000 units were in the ending Work in Process inventory and are 75% complete. Compute the number of equivalent units produced by the department.

(Multiple Choice)

4.8/5 (43)

In the same time period, it is possible that a production department can produce 1,000 equivalent finished units with respect to direct materials and 800 equivalent finished units with respect to direct labor.

(True/False)

4.8/5 (32)

If the predetermined overhead allocation rate is 250% of direct labor cost and the Finishing Department's direct labor cost for the reporting period is $20,000, the following entry would record the allocation of overhead to the products processed in this department:

(True/False)

4.8/5 (41)

Conversion cost per equivalent unit is the combined cost of direct materials, direct labor, and factory overhead per equivalent unit.

(True/False)

4.9/5 (38)

During April, the production department of a process operations system completed and transferred to finished goods 18,000 units that were in process at the beginning of April and 90,000 units that were started and completed in April. April's beginning inventory units were 100% complete with respect to materials and 40% complete with respect to labor. At the end of April, 30,000 additional units were in process in the production department and were 100% complete with respect to materials and 60% complete with respect to labor. The beginning inventory included materials cost of $107,000 and the production department incurred direct materials cost of $329,000 during the month. Compute the direct materials cost per equivalent unit for the department using the weighted-average method.

(Multiple Choice)

4.8/5 (40)

Since the process cost summary describes the activities of a production department for a specified reporting period, it does not present information about any costs incurred in prior periods.

(True/False)

4.8/5 (37)

The third step in accounting for production activity in a period, before assigning and reconciling costs, is to compute the ________.

(Short Answer)

4.8/5 (41)

What is a hybrid costing system? When is a hybrid costing system appropriate for a manufacturer?

(Essay)

4.8/5 (36)

The cost of units transferred from Work in Process Inventory to Finished Goods Inventory is called the cost of goods manufactured.

(True/False)

4.8/5 (36)

In a process costing system costs are only measured upon completion of each job.

(True/False)

4.8/5 (34)

If Department C uses $10,000 of direct materials and Department D uses $15,000 of direct materials, the following journal entry would be recorded by the process costing system:

(True/False)

4.8/5 (43)

At the beginning of the recent period, there were 900 units of product in a department, 35% completed. These units were finished and an additional 5,000 units were started and completed during the period. 800 units were still in process at the end of the period, 25% completed. Using the weighted average method, the equivalent units produced by the department were:

(Multiple Choice)

4.8/5 (31)

Sparky Corporation uses the FIFO method of process costing. The following information is available for February in its Molding Department: Units:

Beginning Inventory: 25,000 units, 100% complete as to materials and 55% complete as to conversion.

Units started and completed: 110,000.

Units completed and transferred out: 135,000.

Ending Inventory: 30,000 units, 100% complete as to materials and 30% complete as to conversion.

Costs:

Costs in beginning Work in Process - Direct Materials: $43,000.

Costs in beginning Work in Process - Conversion: $48,850.

Costs incurred in February - Direct Materials: $287,000.

Costs incurred in February - Conversion: $599,150.

Calculate the cost per equivalent unit of conversion.

(Multiple Choice)

4.9/5 (35)

In a process costing system, the entry to record cost of materials assigned to a production department requires a debit to the Work in Process Inventory account for that department and a credit to the Raw Materials Inventory account.

(True/False)

4.9/5 (29)

Dazzle, Inc. produces beads for jewelry making use. The following information summarizes production operations for June. The journal entry to record June production activities for goods transferred from production to finished goods is:

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)