Exam 4: Coordinating Smart Choices: Demand and Supply

Exam 1: Whats in Economics for You Scarcity, Opportunity Cost, Trade, and Models215 Questions

Exam 2: Making Smart Choices: the Law of Demand159 Questions

Exam 3: Show Me the Money: the Law of Supply159 Questions

Exam 4: Coordinating Smart Choices: Demand and Supply226 Questions

Exam 5: Are Your Smart Choices Smart for All Macroeconomics and Microeconomics185 Questions

Exam 6: Up Around the Circular Flow: Gdp, Economic Growth, and Business Cycles277 Questions

Exam 7: Costs of Not Working and Living: Unemployment and Inflation255 Questions

Exam 8: Skating to Where the Puck Is Going: Aggregate Supply and Aggregate Demand304 Questions

Exam 9: Money Is for Lunatics: Demanders and Suppliers of Money227 Questions

Exam 10: Trading Dollars for Dollars Exchange Rates and Payments With the Rest of the World245 Questions

Exam 11: Steering Blindly Monetary Policy and the Bank of Canada217 Questions

Exam 12: Spending Others Money: Fiscal Policy, Deficits, and National Debt237 Questions

Exam 13: Are Sweatshops All Bad Globalization and Trade Policy205 Questions

Select questions type

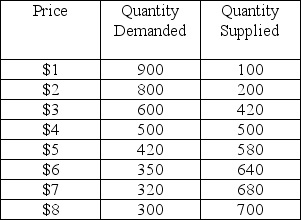

Figure 4.2.1

Market Demand and Supply for Pet Rocks

-Look at Figure 4.2.1. There is a shortage if the price is

-Look at Figure 4.2.1. There is a shortage if the price is

(Multiple Choice)

4.7/5  (31)

(31)

Businesses adjust prices more frequently than they adjust quantities.

(True/False)

4.9/5 (33)

Without property rights there would be no incentive to produce and sell products.

(True/False)

4.8/5 (22)

When a market is in equilibrium, businesses that are not willing to supply products or services at the market-clearing price have not made a smart choice.

(True/False)

4.9/5 (36)

Prices are the outcome of a market process of competing bids and offers.

(True/False)

4.8/5 (32)

If buyers expect the price of gasoline will be higher in the future, the price of gasoline today ________ and the quantity supplied today ________.

(Multiple Choice)

4.8/5 (38)

Producer surplus is the area under the marginal benefit curve but above the market price.

(True/False)

4.8/5 (31)

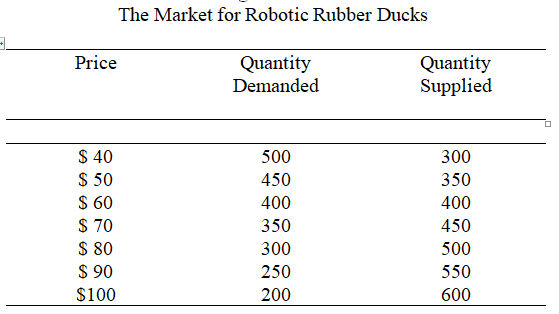

Table 4.2.2.

-Look at Table 4.2.2. Consumers learn that the rubber ducks wear out batteries quickly. As a result, demand decreases by 100 rubber ducks at each price. At the same time, input prices rise and supply decreases by 100 rubber ducks at each price. The new equilibrium price is $________ and the new equilibrium quantity is ________ rubber ducks.

Table 4.2.2.

-Look at Table 4.2.2. Consumers learn that the rubber ducks wear out batteries quickly. As a result, demand decreases by 100 rubber ducks at each price. At the same time, input prices rise and supply decreases by 100 rubber ducks at each price. The new equilibrium price is $________ and the new equilibrium quantity is ________ rubber ducks.

(Multiple Choice)

4.8/5 (44)

If the price of gasoline rises, the price of automobiles should also rise because gasoline and automobiles are complementary products.

(True/False)

4.7/5 (29)

Shortages create incentives for businesses to make quantity adjustments even when prices don't change.

(True/False)

4.8/5 (37)

If enrollment at your school decreases even though tuition fees fall, it is likely that

(Multiple Choice)

4.9/5 (32)

If the price of gasoline rises, the price of automobiles should fall because gasoline and automobiles are complementary products.

(True/False)

4.8/5 (32)

When the price is too low, shortages cause the price to fall further.

(True/False)

4.7/5 (37)

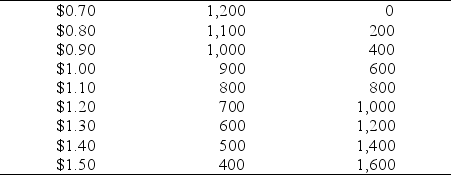

Figure 4.3.1

Market for Espresso Shots

-Look at Table 4.3.1. Drought destroys many coffee plants, causing half of the espresso businesses to go out of business. This change is a

-Look at Table 4.3.1. Drought destroys many coffee plants, causing half of the espresso businesses to go out of business. This change is a

(Multiple Choice)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)