Exam 12: Managing and Reporting Performance

Exam 1: Management Accounting: Information for Creating Value and Managing Resources52 Questions

Exam 2: Management Accounting: Cost Terms and Concepts73 Questions

Exam 3: Cost Behaviour, Cost Drivers and Cost Estimation78 Questions

Exam 4: Product Costing Systems74 Questions

Exam 5: Process Costing and Operation Costing73 Questions

Exam 6: Service Costing78 Questions

Exam 7: A Closer Look at Overhead Costs85 Questions

Exam 8: Activity-Based Costing78 Questions

Exam 9: Budgeting Systems78 Questions

Exam 10: Standard Costs for Control: Direct Material and Direct Labour91 Questions

Exam 11: Standard Costs for Control: Flexible Budgets and Manufacturing Overhead97 Questions

Exam 12: Managing and Reporting Performance88 Questions

Exam 13: Financial Performance Measures and Incentive Schemes80 Questions

Exam 14: Strategic Performance Measurement Systems73 Questions

Exam 15: Managing Suppliers and Customers76 Questions

Exam 16: Managing Costs and Quality78 Questions

Exam 17: Sustainability and Management Accounting71 Questions

Exam 18: Cost Volume Profit Analysis97 Questions

Exam 19: Information for Decisions: Relevant Costs and Benefits95 Questions

Exam 20: Pricing and Product Mix Decisions95 Questions

Exam 21: Information for Capital Expenditure Decisions108 Questions

Select questions type

The data in a performance report helps managers to:

Free

(Multiple Choice)

4.7/5  (43)

(43)

Correct Answer: Verified

Verified

A

When using cost-based transfer prices,actual costs should be used in preference to standard costs.

Free

(True/False)

4.8/5 (26)

Correct Answer:Verified

False

If a manager were responsible for a division's performance and activities,the division would have to be classified as a cost centre.

Free

(True/False)

4.9/5 (46)

Correct Answer:Verified

False

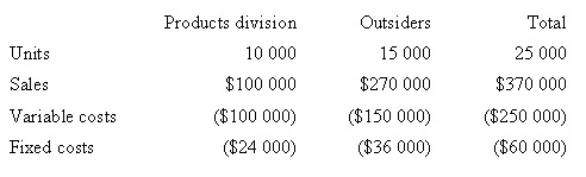

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assuming the Milling Division manager agrees to the special offer,what is the effect of the decision on the gross margin of Weber as a whole?

(Multiple Choice)

4.8/5 (29)

Which of the following statements unambiguously describes the term 'contribution margin'?

(Multiple Choice)

4.8/5 (41)

In a divisional corporate organisation,an ideal inter-divisional transfer price should:

(Multiple Choice)

4.8/5 (36)

Which of the following statements about cost-based transfer prices is/are true?

i.A transfer price set at standard variable cost plus a mark-up provides an incentive for the supplying business to make the transfer

ii.Absorption cost-based transfer prices are good for the company as a whole because all costs are considered.

iii.Transfer prices should be based on standard costs rather than actual costs since the cost of inefficiency should not be passed on.

(Multiple Choice)

4.9/5 (40)

Transfer prices should not be based on absorption costs as this could result in suboptimal decisions by the:

(Multiple Choice)

4.9/5 (28)

Which of the following might you expect to see being used as a performance measure for a profit centre?

(Multiple Choice)

4.8/5 (26)

The costs arising from activities that benefit two or more units are generally referred to as controllable costs.

(True/False)

4.8/5 (38)

Which of the following is a problem with the use of a negotiated transfer price?

(Multiple Choice)

4.9/5 (39)

Fruities Ltd has two divisions,Durian Division and Juice Division.Durian Division has an annual capacity of 10 000 units of durian juice concentrate.Juice Division's annual requirement of durian juice concentrate is 8000 units.Fruities Ltd requires that divisions should purchase inputs internally where available,and uses a cost-plus transfer price policy,where transfer price is set at variable cost plus 25 per cent.Therefore,Durian Division always satisfies the demand of the Juice Division first,before selling the remaining durian concentrate to external suppliers at the market price of $10 per unit.The variable cost of one unit of durian juice concentrate at Durian Division is $6.The external demand for Durian Division's durian juice concentrate is 2000 units.What is the difference in the overall profit of Fruities Ltd under the cost-plus transfer price policy and a market-price transfer price policy?

(Multiple Choice)

4.9/5 (37)

Which of the following managers is held accountable for only the revenue attributed to a subunit?

(Multiple Choice)

5.0/5 (42)

Polly Woodside Maritime Division purchases from an outside supplier for $52 per unit.The company's Shore Division,which has excess capacity,makes and sells the same part for external customers at a variable cost of $38 and a selling price of $58.If Shore Division commences sales to Maritime Division it will (1)use the general rule and (2)be able to reduce the variable cost on internal transfers by $4.If external sales are not affected,Shore Division should establish a transfer price of:

(Multiple Choice)

4.8/5 (32)

When a contribution margin format is used for reporting,expenses are grouped according to the functions (e.g.sales and distribution,financial)carried out by the organisation.

(True/False)

4.9/5 (38)

When a company manager's behaviour is aimed at achieving the goals of an organisation,the company can be confident of goal congruence.

(True/False)

4.9/5 (35)

Hamilton has no excess capacity.If the company wishes to implement the general transfer-pricing rule,the opportunity cost would be equal to:

(Multiple Choice)

4.9/5 (35)

Division A transfers a profitable subassembly to Division B,where it is assembled into a final product.Division A is located in New Zealand,which has a high tax rate.Division B is located in Thailand,which has a low tax rate.Ideally, (1)which type of before tax income should each division report from the transfer and (2)what type of transfer price should be set for the subassembly?

Division A

Division B

Division C

Income

Income

Price

(Multiple Choice)

4.7/5 (36)

Fragrance Pty Ltd has two divisions: the Cologne Division and the Bottle Division.The company is decentralised and each division is evaluated as a profit centre.The Bottle Division produces bottles that can be used by the Cologne Division.The Bottle Division's variable manufacturing cost per unit is $2.00 and shipping costs are $0.10 per unit.The Bottle Division's external sales price is $3.00 per unit.No shipping costs are incurred on sales to the Cologne Division.The Cologne Division can purchase similar bottles in the external market for $2.50.The Bottle Division has sufficient capacity to meet all external market demands in addition to meeting the demands of the Cologne Division.Using the general rule,the minimum transfer price from the Bottle Division to the Cologne Division would be:

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)