Exam 12: Managing and Reporting Performance

Exam 1: Management Accounting: Information for Creating Value and Managing Resources52 Questions

Exam 2: Management Accounting: Cost Terms and Concepts73 Questions

Exam 3: Cost Behaviour, Cost Drivers and Cost Estimation78 Questions

Exam 4: Product Costing Systems74 Questions

Exam 5: Process Costing and Operation Costing73 Questions

Exam 6: Service Costing78 Questions

Exam 7: A Closer Look at Overhead Costs85 Questions

Exam 8: Activity-Based Costing78 Questions

Exam 9: Budgeting Systems78 Questions

Exam 10: Standard Costs for Control: Direct Material and Direct Labour91 Questions

Exam 11: Standard Costs for Control: Flexible Budgets and Manufacturing Overhead97 Questions

Exam 12: Managing and Reporting Performance88 Questions

Exam 13: Financial Performance Measures and Incentive Schemes80 Questions

Exam 14: Strategic Performance Measurement Systems73 Questions

Exam 15: Managing Suppliers and Customers76 Questions

Exam 16: Managing Costs and Quality78 Questions

Exam 17: Sustainability and Management Accounting71 Questions

Exam 18: Cost Volume Profit Analysis97 Questions

Exam 19: Information for Decisions: Relevant Costs and Benefits95 Questions

Exam 20: Pricing and Product Mix Decisions95 Questions

Exam 21: Information for Capital Expenditure Decisions108 Questions

Select questions type

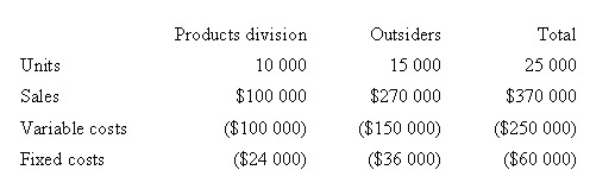

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.00.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.All 25 000 units can be sold at the regular price to outside customers and the Product Division's annual demand declines to 5 000 units.What transfer price would be calculated under the general transfer-pricing formula?

(Multiple Choice)

5.0/5  (42)

(42)

Transfer pricing is a system established internally to facilitate units being set up as profit centres.

(True/False)

4.9/5 (36)

Which of the following is a key problem with the use of market-based transfer prices?

(Multiple Choice)

4.9/5 (39)

Which of the following statements is false,with respect to a negotiated transfer price?

(Multiple Choice)

5.0/5 (32)

Although shared service units are generally established as profit centres it is often acceptable if a zero profit is achieved.

(True/False)

4.8/5 (30)

Which of the following are characteristics of flash reports?

i.Provided daily

ii.Include both financial and non-financial information

iii.Comprehensive and cover the full range of performance criteria

(Multiple Choice)

4.8/5 (39)

Which of the following managers is held accountable for the profit of the subunit?

(Multiple Choice)

4.8/5 (34)

Which of the following are benefits of self-managed work teams?

i.Improved customer service

ii.Increased goal congruence among team members

iii.Increased control by top management over outcomes

(Multiple Choice)

4.9/5 (34)

When managers within the various subunits of an organisation are committed to achieving the goals set by top management,the result is:

(Multiple Choice)

4.9/5 (39)

Business unit reporting shows profit and loss statements for the company as a whole and for:

(Multiple Choice)

4.8/5 (35)

Which of the following statements about the general transfer-pricing rule is/are true?

i.When the producing division has excess capacity,the transfer decision should be based on the outlay cost

ii.When the producing division has no excess capacity,the opportunity cost is the foregone contribution from the lost sale.

iii.If the producing division has excess capacity or the external market is imperfectly competitive,the general rule and the external market price will not yield the same transfer price.

(Multiple Choice)

4.9/5 (40)

The difference between establishing a shared service unit and centralisation shared services include:

i.centralised services are located at corporate headquarters;shared services are located close to internal customers

Ii centralised services are more efficient than shared services

Iii centralised services are evaluated based on service adherence to service level agreements;shared services are evaluated based on budgets and corporate objectives

(Multiple Choice)

4.8/5 (36)

When the transfer price chosen by management charges another department the price that would be charged to outside customers,this type of transfer pricing is called:

(Multiple Choice)

4.8/5 (39)

The budgeted and actual amount of a responsibility centre's key financial results are shown on a:

(Multiple Choice)

4.8/5 (28)

Nova Company has two divisions: OPA Division and LPA Division.The OPA Division manufactures a single product,presently operates at 95 per cent of full capacity (100 000 units)and can sell all 95 000 units produced to outside customers.This product is also a component used in a product made by the LPA Division.OPA's full cost of production is $22.50 per unit,including $4.50 of applied fixed overhead costs.The applied fixed overhead is calculated based upon production of 95 000 units.OPA's management believes that production can be raised to 100 000 units without affecting cost behaviour.OPA's selling price per unit is $30 with a 10 per cent sales commission on outside sales.LPA is presently negotiating the purchase of units from OPA.LPA can purchase a comparable component outside for $29.What is the minimum acceptable transfer price for the first 5000 units from the viewpoint of OPA's management?

(Multiple Choice)

4.9/5 (33)

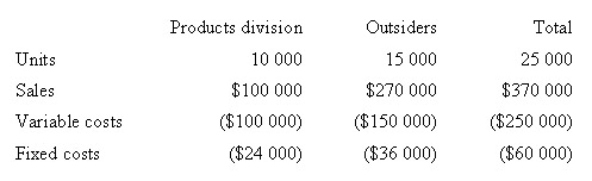

Corporate policy at Weber Pty Ltd requires that all transfers between divisions be recorded at variable cost as a transfer price.Divisional managers have complete autonomy in choosing their sources of customers and suppliers.The Milling Division sells a product called RK2.Forty per cent of the sales of RK2 are to the Products Division,while the remainder of the sales are to outside customers.The manager of the Milling Division is evaluating a special offer from an outside customer for 10 000 units of RK2 at a per unit price of $15.If the special offer were accepted,the Milling Division would be unable to supply those units to the Products Division.The Products Division could purchase those units from another supplier for $17 per unit.Annual capacity for the Milling Division is 25 000 units.The 2008 budget information for the Milling Division,based on full capacity,is presented below.Assume that demand increases for the Milling Division.20 000 units can be sold at the regular price to outside customers and the Products Division's annual demand remains at 10 000 units.What is the transfer price that would be calculated under the general transfer-pricing formula?

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)