Multiple Choice

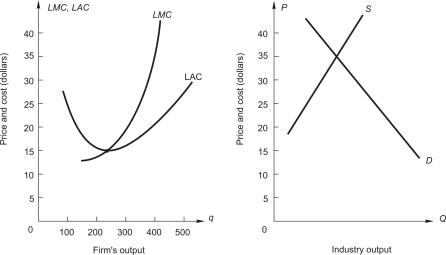

Below,the graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry.The graph on the right shows demand and long-run supply for an increasing-cost industry.  If this were a constant-cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

If this were a constant-cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

A) between $35 and $20

B) $35

C) $20

D) below $20

E) above $35

Correct Answer:

Verified

Correct Answer:

Verified

Q85: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB7882/.jpg" alt=" The graph above

Q86: Below,the graph on the left shows the

Q87: The table below shows a competitive

Q88: In a perfectly competitive market<br>A)a firm must

Q89: Sport Tee Corporation manufactures T-shirts bearing

Q91: Below,the graph on the left shows the

Q92: In long-run competitive equilibrium it is possible

Q93: In a competitive industry the market-determined price

Q94: Consider a competitive industry and a

Q95: In a perfectly competitive industry the market