Multiple Choice

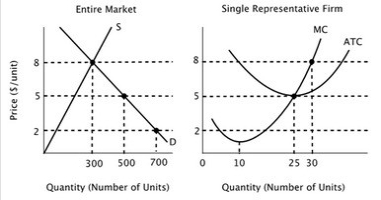

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  In the long run equilibrium in this market:

In the long run equilibrium in this market:

A) price will equal $5, and there will be 20 firms in the industry.

B) price will equal $5, and there will be 10 firms in the industry.

C) price will equal $8, and there will be 20 firms in the industry.

D) price will equal $5 and total output will equal 500 units, but there is not enough information to determine how many firms will be in the industry.

Correct Answer:

Verified

Correct Answer:

Verified

Q89: Suppose the market for coffee is in

Q90: The figure below depicts the short-run market

Q91: The figure below shows the supply and

Q92: If a firm is earning zero economic

Q93: Suppose a small island nation imports sugar

Q95: The fact that price subsidies reduce economic

Q96: A cost-saving innovation in a perfectly competitive

Q97: The figure below shows the supply and

Q98: In a free market economy, the decisions

Q99: Which of the following best describes how