Multiple Choice

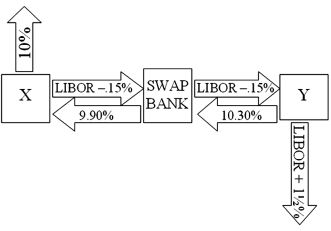

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown below:  A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 9.90%. Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%.

A swap bank proposes the following interest only swap: X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 9.90%. Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30% and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR - 0.15%.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

A) The swap bank will lose money on the deal.

B) The swap bank will earn 40 basis points per year on $10,000,000 = $40,000 per year.

C) The swap bank will break even.

D) None of the above

Correct Answer:

Verified

Correct Answer:

Verified

Q48: Consider the borrowing rates for Parties A

Q50: Come up with a swap (exchange of

Q51: The term interest rate swap<br>A)refers to a

Q52: Pricing a currency swap after inception involves<br>A)finding

Q54: Suppose that you are a swap bank

Q56: FOR YOUR SWAP (the one you have

Q57: Devise a direct swap for A and

Q58: The size of the swap market is<br>A)measured

Q82: Which combination of the following represent the

Q100: You are the debt manager for a