Exam 25: Segment Reporting

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

In the situation where an entity has invested in segments that are diverse:

(Multiple Choice)

4.9/5  (30)

(30)

Situations in which aggregated data may be sufficient to evaluate the performance of an entity include:

(Multiple Choice)

4.9/5 (35)

Information about operating segments that do not meet any of the quantitative thresholds:

(Multiple Choice)

4.9/5 (34)

AASB 8 requires a number of reconciliations to be presented, including:

(Multiple Choice)

4.8/5 (43)

An important argument for providing segmental information in the financial reports is:

(Multiple Choice)

4.8/5 (34)

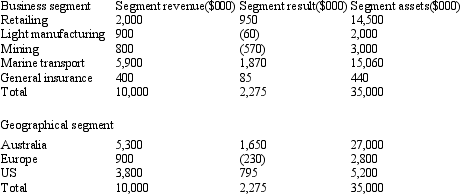

The following segment information is presented for Hobbitt LtD.

There are no inter-segment sales. Which segments are reportable according to the guidelines provided in AASB 114?

There are no inter-segment sales. Which segments are reportable according to the guidelines provided in AASB 114?

(Multiple Choice)

4.7/5 (32)

AASB 8 specifies guidelines regarding whether or not a segment is reportable. These guidelines are known as the 10 per cent rules. All three rules are required to be met in order to establish a reportable segment:

(True/False)

4.8/5 (41)

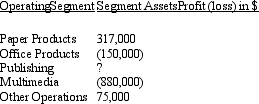

Consider the following list of operating segments and segment results for the current reporting period relating to Legolas Ltd, and answer the question below.

What is the minimum loss (rounded to the nearest $1,000) that the Publishing segment could have made for that segment to be considered a reportable segment according to AASB 8?

What is the minimum loss (rounded to the nearest $1,000) that the Publishing segment could have made for that segment to be considered a reportable segment according to AASB 8?

(Multiple Choice)

4.8/5 (34)

Consider the following list of operating segments and segment assets for the current reporting period relating to Arwen Ltd, and answer the question below.

What is the minimum asset amount rounded to the nearest $1,000) that the Fast Food segment should have for that segment to be considered a reportable segment according to AASB 8?

What is the minimum asset amount rounded to the nearest $1,000) that the Fast Food segment should have for that segment to be considered a reportable segment according to AASB 8?

(Multiple Choice)

4.8/5 (26)

The guidelines to determine that a segment is reportable in accordance with AASB 8 "Operating Segments" includes:

(Multiple Choice)

4.8/5 (32)

AASB 8 specifies that a geographical segment cannot include more than two countries:

(True/False)

5.0/5 (37)

Examples of liabilities not considered liabilities of a manufacturing segment by AASB 114 include:

(Multiple Choice)

4.9/5 (39)

AASB 8 requires reconciliation of reported segments' amounts to the entity's reported amount for which of the following items?

(Multiple Choice)

4.8/5 (37)

AASB 8 does not require disclosure of a reportable segment if a segment is mainly transacting with related parties.

(True/False)

4.8/5 (43)

Segment information may be useful to investors who wish to use ethical guidelines about which industries or countries they invest in:

(True/False)

4.8/5 (38)

AASB 8 bans the disclosure of segments that do not pass the "10 per cent test".

(True/False)

4.8/5 (38)

Two or more operating segments may be aggregated into a single operating segment if aggregation is consistent with the core principle of AASB 8, or the segments have similar economic characteristics, or the segments are similar in the nature of the products and services.

(True/False)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)