Exam 12: Set-Off and Extinguishment of Debt

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

AASB 132 "Financial Instruments: Presentation" supports a substance over from approach in the accounting treatment for Insubstance Debt Defeasance (ISDD).

Free

(True/False)

4.7/5  (32)

(32)

Correct Answer: Verified

Verified

False

A legal defeasance may occur as a result of:

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

A

Release from the primary obligation of a debt may theoretically be achieved by:

Free

(Multiple Choice)

4.7/5 (30)

Correct Answer:Verified

E

Businesses may be prepared to incur a loss on the defeasance of debt because:

(Multiple Choice)

4.8/5 (45)

On 1 July 2008, Roos Limited issues $3 million in ten year, 8 per cent annual debentures to Hall Limited. The market required rate of return on the debentures at the time is 12 per cent. On 1 July 2010, Hall Limited decided to forgive the debt owed by Roos Limited, and so cancels the debt. Assuming Roos Limited uses the straight-line method to amortise the debenture discount, what is the journal entry passed in the books of Roos Limited at 1 July 2010?:

(Multiple Choice)

4.9/5 (35)

The definition of a set-off is that an asset is reduced by the amount of a liability and a net liability remains:

(True/False)

4.9/5 (40)

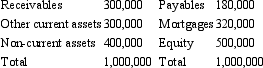

Pete Ltd's statement of financial position is shown below.

The above balances include a receivable from Patricia Ltd for an amount of $100,000 and a payable to Patricia Ltd for $50,000. A debt contract with ABC Bank signed by Pete Ltd requires a debt equity ratio of no more than 50%.

Based on the above information, which course of action will be consistent with positive accounting theory?

The above balances include a receivable from Patricia Ltd for an amount of $100,000 and a payable to Patricia Ltd for $50,000. A debt contract with ABC Bank signed by Pete Ltd requires a debt equity ratio of no more than 50%.

Based on the above information, which course of action will be consistent with positive accounting theory?

(Multiple Choice)

4.9/5 (40)

Debt extinguishment occurs when a liability can no longer be considered a primary obligation for an entity:

(True/False)

4.8/5 (42)

A right of set-off is a debtor's legal right, by contract or otherwise, to settle or otherwise eliminate all or a portion of an amount due to a creditor by applying against that amount an amount due from the creditor.

(True/False)

4.9/5 (36)

The effect of setting off on the gearing ratio of the reporting entity is to:

(Multiple Choice)

4.9/5 (35)

AASB 132 allows for all types of assets and liabilities to be offset as long as the entity intends to settle on a net basis:

(True/False)

4.7/5 (42)

Under the old AASB 1014 the debt-holder(s) may not be aware that a debt defeasance scheme is in place:

(True/False)

4.9/5 (30)

Which of the following instruments satisfy the conditions to offset a financial asset and a financial liability?

(Multiple Choice)

4.7/5 (35)

What is the AASB 132 requirement in relation to debt set-off?

(Multiple Choice)

4.7/5 (34)

Reasons provided in AASB 132 for the required treatment of the set-off of assets and liabilities include:

(Multiple Choice)

4.9/5 (34)

There were two methods of achieving an insubstance debt defeasance in accordance with the former AASB 1014's requirements:

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)