Exam 35: Accounting for Foreign Currency Transactions

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

The effect of an increase in the exchange rate for Australian dollars relative to other major world currencies would include:

Free

(Multiple Choice)

4.9/5  (41)

(41)

Correct Answer: Verified

Verified

C

Management may exercise its judgement to determine the functional currency that most faithfully represents the economic effects of the underlying transactions, events and conditions.

Free

(True/False)

4.9/5 (39)

Correct Answer:Verified

False

Examples of monetary items that may be denominated in foreign currencies include:

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

B

Issues in relation to foreign currency arise when a reporting entity based in Australia has transactions with an overseas entity and the transaction is denominated in Australian currency:

(True/False)

4.8/5 (31)

A foreign currency transaction shall be recorded on initial recognition in the:

(Multiple Choice)

4.9/5 (27)

The purpose of 'hedge accounting' is to recognise the offsetting effects on profit or loss of changes in the nominal values of the financial instrument and the hedging instrument:

(True/False)

4.9/5 (37)

Apart from some limited exceptions, AASB 121 requires that exchange differences on monetary items shall be:

(Multiple Choice)

5.0/5 (37)

AASB 123 Borrowing Costs defines a qualifying asset as an asset that:

(Multiple Choice)

4.8/5 (38)

On 1 May 2005 Harry's Plastics Ltd acquires goods from a supplier in the US. The goods are shipped f.o.b. from America on 1 May 2005. The cost of the goods is US$1,500,000. The amount has not been paid at period end, 30 June 2005. Exchange rates are as follows:

Harry's Plastics Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole $A)?

Harry's Plastics Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole $A)?

(Multiple Choice)

4.9/5 (42)

Monetary items are units of currency held and assets and liabilities to be received or paid in a fixed or determinable number of units of currency.

(True/False)

4.8/5 (40)

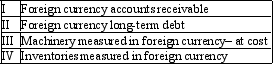

The following items are in the financial statements of Pirie Ltd as at 30 June 2012.

Which of the following combinations identify all items required to be translated at spot rate on 30 June 2012 as prescribed in AASB 112 "The effects of changes in foreign exchange rates"?

Which of the following combinations identify all items required to be translated at spot rate on 30 June 2012 as prescribed in AASB 112 "The effects of changes in foreign exchange rates"?

(Multiple Choice)

4.7/5 (36)

The effect of a fall in the exchange rate for Australian dollars relative to other major world currencies would include:

(Multiple Choice)

4.8/5 (40)

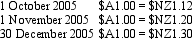

Emu Exports Ltd sold products to a New Zealand company. The sales contract was denominated in $NZ. On 1 October 2005, $NZ500,000 worth of products were sold with the terms f.o.b. shipping point and payment due 30 December 2005. A forward-exchange contract in which the bank agrees to purchase $NZ300,000 from Emu Exports on 30 December 2005 is entered into on 1 November 2005. The forward-exchange rate is $A1 = $NZ1.25. Other exchange rates are as follows:

What are the journal entries to record the above transactions from 1 October through to 30 December 2005 in accordance with AASB 121 (rounded to the nearest whole $A)?

What are the journal entries to record the above transactions from 1 October through to 30 December 2005 in accordance with AASB 121 (rounded to the nearest whole $A)?

(Multiple Choice)

4.9/5 (38)

On 1 July 2005 Jarrets Ltd borrows £500,000 from a British bank at an interest rate of 8 per cent, repayable in pounds sterling (£) and with interest due on 30 June each year. The term of the loan is 3 years. On the same date Fitners Ltd borrows $A1 million from an Australian bank at an interest rate of 10 per cent. The term of the loan is 3 years. Jarrets and Fitners decide to swap their interest and principal obligations on 1 July 2005. Exchange rate information is as follows:

Both Jarrets and Fitners are Australian companies. What are the journal entries to record the swap for the period ended 30 June 2006 in Fitners Ltd's books (rounded to the nearest whole $A)?

Both Jarrets and Fitners are Australian companies. What are the journal entries to record the swap for the period ended 30 June 2006 in Fitners Ltd's books (rounded to the nearest whole $A)?

(Multiple Choice)

4.8/5 (33)

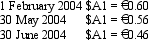

On 1 February 2004, Morinda Ltd completes a binding agreement to purchase a hydraulic lift from a manufacturer located in Germany. The cost of the equipment is €150,000. The construction of the lift is completed on 30 May 2004, and it is considered to be a qualifying asset according to AASB 123. The amount owing has not been paid by reporting date 30 June 2004. The following is information about the exchange rates:

What entries are required to record the transaction and subsequent events in accordance with AASB 121 (rounded to the nearest whole $A)?

What entries are required to record the transaction and subsequent events in accordance with AASB 121 (rounded to the nearest whole $A)?

(Multiple Choice)

4.9/5 (37)

Which of the following items is within the scope of AASB 112 "The effects of changes in foreign exchange rates"?

(Multiple Choice)

4.8/5 (34)

AASB 121 requires that the initial recognition of a foreign currency transaction be:

(Multiple Choice)

4.8/5 (34)

On 1 May 2005 Harriet's Importers Ltd acquires goods from a supplier in Britain. The goods are shipped f.o.b. from England on 1 May 2005. The cost of the goods is £200,000. The amount has not been paid at period end, 30 June 2005. Exchange rates are as follows:

Harriet's Importers Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole $A)?

Harriet's Importers Ltd uses a perpetual inventory system.

What entries are required at transaction date and reporting date (rounded to the nearest whole $A)?

(Multiple Choice)

5.0/5 (24)

It seems pointless to distinguish between different types of hedges, as the accounting treatment is the same for all hedging - i.e., all changes in fair values of hedging instruments are recognised in profit or loss

(True/False)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)