Exam 6: Revaluation and Impairment Testing of Non-Current Assets

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Under AASB 116 when an asset is revalued and the gross method is used, accumulated depreciation:

Free

(Multiple Choice)

4.9/5  (37)

(37)

Correct Answer: Verified

Verified

D

A machine purchased by White Ltd had a cost of $670,000 and an accumulated depreciation balance of $120,000 at 30 June 2002. Its fair value is assessed at this time, with its first revaluation as $450,000. What is/are the appropriate journal entry(ies) to record the revaluation?

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

D

The concept of conservatism requires that if a class of non-current assets is revalued a revaluation decrement should be treated as an expense of the period, whereas a revaluation increment should be treated as an increase in a reserve:

Free

(True/False)

4.9/5 (34)

Correct Answer:Verified

True

Where management's bonuses are tied to profit-based performance measures management may have an incentive not to revalue assets because:

(Multiple Choice)

4.9/5 (43)

The revaluation model is a tool used by managers to reduce political costs.

(True/False)

4.7/5 (34)

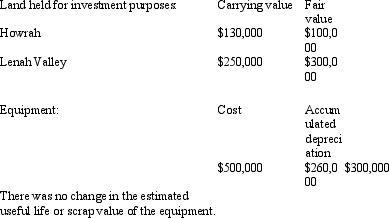

Hendersons Ltd has just begun to revalue its plant and equipment. The following information about the items included in this class of non-current assets shows their carrying value, and most recent revaluation.

What is/are the appropriate journal entry(ies) to record the revaluations?

What is/are the appropriate journal entry(ies) to record the revaluations?

(Multiple Choice)

4.9/5 (36)

Pigeon Ltd purchased land for $750,000 6 years ago. It was revalued on 31 December 2002 to $600,000. A subsequent revaluation on 31 December 2004 found the market value to be $900,000 due to a change in council zoning for the area. What are the journal entries required to record the revaluations on 31 December 2002 and 31 December 2004?

(Multiple Choice)

4.8/5 (38)

If an asset's carrying amount is impaired, AASB 116 requires all assets in the same class to be revalued.

(True/False)

4.9/5 (34)

Once an entity elects to value a class of assets using fair value it can switch back to cost basis measurement as long as there is justifiable reason:

(True/False)

4.8/5 (38)

Stairway Ltd is undertaking its regular review of the fair value of its assets. It has discovered the following material changes:

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

(Multiple Choice)

4.9/5 (29)

Staples Ltd has invested in two parcels of land that are treated as belonging to the same class of assets. The first parcel of land was purchased for $500,000 and has been valued this period at $650,000. The second parcel of land has a carrying value of $340,000 and has been valued this period at $100,000. What is the appropriate journal entry to record the revaluations?

(Multiple Choice)

5.0/5 (45)

Under AASB 116 when an asset is revalued and the net method is used, accumulated depreciation:

(Multiple Choice)

4.8/5 (37)

Research using the Positive Accounting Theory approach investigated public trust deeds and found that in relation to revaluations they:

(Multiple Choice)

4.8/5 (31)

Brown, Izan and Loh (1992) found that revaluations are more likely to take place:

(Multiple Choice)

4.7/5 (37)

Once a class of non-current assets has been revalued, AASB 116 requires that:

(Multiple Choice)

4.9/5 (36)

Which of the following statements is a valid reason to select cost model over the revaluation model?

(Multiple Choice)

4.8/5 (38)

Smith & Jones Ltd owns equipment that was purchased for $56,000 and has accumulated depreciation of $14,000. The following market value information was gathered about the equipment:

The equipment has a remaining useful life to the entity of 10 years. What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

The equipment has a remaining useful life to the entity of 10 years. What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

(Multiple Choice)

4.8/5 (35)

AASB 116 requires that revaluation increments and decrements must be offset recorded directly to equity and not be recorded as a gain or loss:

(True/False)

4.8/5 (39)

Where there are debt covenants in place to restrict the level of debt to assets then management may be motivated to:

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)