Exam 7: Inventory

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

AASB 102 requires that inventory is valued at:

Free

(Multiple Choice)

4.8/5  (35)

(35)

Correct Answer: Verified

Verified

C

AASB 102 requires that fixed manufacturing costs be excluded from the cost of inventories, as they cannot be allocated accurately:

Free

(True/False)

4.9/5 (37)

Correct Answer:Verified

False

The periodic inventory system operates by:

Free

(Multiple Choice)

4.8/5 (44)

Correct Answer:Verified

B

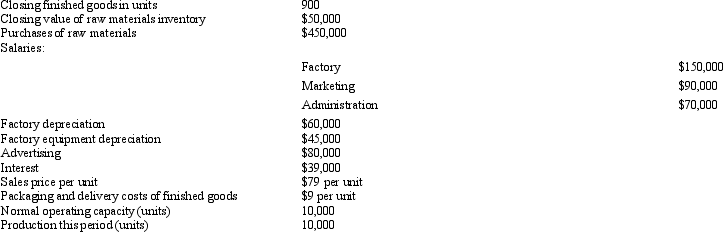

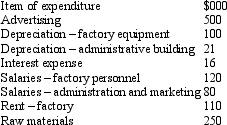

Balmoral Ltd commenced business on 1 July 2003. The company manufactures bookcases. Summary data for Balmoral's first full year of operations are:

Packaging and delivery are essential to be able to sell the product. What total value should be attributed to finished goods inventory in the financial statements in accordance with AASB 102?

Packaging and delivery are essential to be able to sell the product. What total value should be attributed to finished goods inventory in the financial statements in accordance with AASB 102?

(Multiple Choice)

4.9/5 (40)

Toey Ltd has provided the following information about the total production cost and estimates of realisable value of three lines of shoes they produce within the same class of inventory:

Packaging and freight are necessary in order to be able to sell the shoes. What is the value of the inventory in accordance with AASB 102?

Packaging and freight are necessary in order to be able to sell the shoes. What is the value of the inventory in accordance with AASB 102?

(Multiple Choice)

5.0/5 (41)

AASB 102 requires among others disclosure of which information:

(Multiple Choice)

5.0/5 (51)

AASB 102 "Inventories" applies to biological assets related to agricultural activity.

(True/False)

4.8/5 (46)

David Gordon is an accountant for Bronte Ltd. At the end of the year he realised that ending inventory was overstated but the purchases account was recorded correctly. What is the effect of above error in the income statement and balance sheet (inventory) accounts of Bronte Ltd?

(Short Answer)

4.8/5 (38)

The inventory record of Palm Springs Ltd. shows 1,000 surf boards on stock that cost $50 each. During the last stock take, the accountant noted 100 old style surf boards with net realisable amount of $15. What journal entry would be required of Palm Springs to comply with AASB 102?

(Multiple Choice)

4.8/5 (40)

In periods where production costs or purchase prices of inventory items do not change, it does not matter which inventory method is adopted as this would generate the same value for cost of goods sold and ending inventory.

(True/False)

4.9/5 (40)

A company engaged in buying and selling equity securities should consider this asset as inventory and should be accounted for in accordance with AASB 102.

(True/False)

4.7/5 (40)

Reversal of a previous inventory write down is not advocated in AASB 102.

(True/False)

4.9/5 (40)

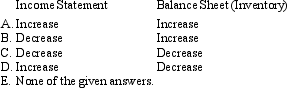

Digitoll Ltd produces a range of computer accessories. One product is a web-cam, a miniature digital camera with the capacity to be linked to a computer. The following are the summary costs for the web-cam for the period ended 31 December 2002:

The production level this period was normal at 10,000 units. What is the cost per unit (rounded to the nearest cent) in accordance with AASB 102 requirements?

The production level this period was normal at 10,000 units. What is the cost per unit (rounded to the nearest cent) in accordance with AASB 102 requirements?

(Multiple Choice)

4.7/5 (37)

AASB 102 applies to all inventories including work in progress under construction contracts:

(True/False)

4.8/5 (37)

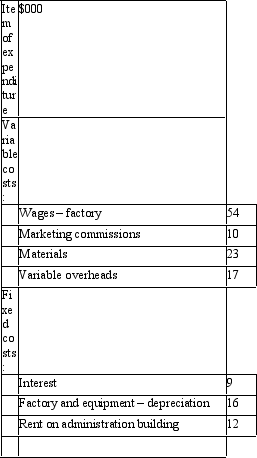

Big Games for Big Kids sell a variety of gaming consoles and games. It has presented you with the following information for the sales of a new product, Angel's Hat 2, for the three months from November to January. They began November with 50 units on hand valued at $1,500. In the lead up to Christmas each unit sold for $90 but in the post Christmas sales in January this price was reduced to $50.

Big Games for Big Kids use the periodic system to record inventory. A physical stock take reveals 30 units on hand at the end of January. What is the cost of sales and value of ending inventory using the FIFO cost-flow assumption?

Big Games for Big Kids use the periodic system to record inventory. A physical stock take reveals 30 units on hand at the end of January. What is the cost of sales and value of ending inventory using the FIFO cost-flow assumption?

(Multiple Choice)

4.8/5 (37)

The following information relates to the total production costs and estimates of realisable value for a line of water pistols produced by Splash Happy Co LtD.

Packaging and transport costs are necessarily incurred in order to be able to sell the inventory. What is the value of the inventory in accordance with AASB 102?

Packaging and transport costs are necessarily incurred in order to be able to sell the inventory. What is the value of the inventory in accordance with AASB 102?

(Multiple Choice)

4.9/5 (40)

Handy Ltd produces a line of brooms. The summary cost information for brooms for the year ended 30 June 2002 is:

The level of output for the period was the normal level of production of 290,000 units. What is the cost per broom (rounded to the nearest cent) in accordance with AASB 102 requirements?

The level of output for the period was the normal level of production of 290,000 units. What is the cost per broom (rounded to the nearest cent) in accordance with AASB 102 requirements?

(Multiple Choice)

4.9/5 (29)

Which of the following is not a definition in AASB 102 on inventories:

(Multiple Choice)

4.9/5 (38)

The only difference between the old AASB 1019 and the new AASB 102 is that the 'international' standards allow inventory to be valued using LIFO:

(True/False)

4.7/5 (25)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)