Exam 17: The Statement of Comprehensive Income and Statement of Changes in E

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

An item must be outside the ordinary operations of the business or be of a non-recurring nature to be classified as an extraordinary item under AASB 101:

(True/False)

4.7/5  (36)

(36)

Estimations are frequently made in the income statement in relation to items such as bad debts, inventory obsolescence, an asset's useful life, and the expected pattern of consumption of economic benefits of depreciable assets. The effect of these estimations on the income statement is to:

(Multiple Choice)

4.7/5 (37)

A statement displaying components of profit or loss is referred to in AASB 101 as a(n):

(Multiple Choice)

4.9/5 (44)

Discovery of an error from a prior period corrected retrospectively is an example of an item reportable under other comprehensive income.

(True/False)

4.8/5 (33)

Different measurement models affect the determination of income and expenses. The different measurement models include:

(Multiple Choice)

4.8/5 (34)

Which of the following is not required to be shown on the face of the income statement?

(Multiple Choice)

5.0/5 (36)

If the exercise (strike) price of a call option is greater than the current share price, the option is said to be 'in-the-money':

(True/False)

4.9/5 (39)

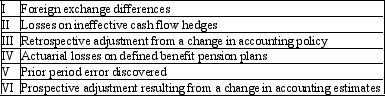

Following are the items of income and expense recognised during the period by Murray LtD.

Which of the following combinations identify all items permitted in AASB 101 "Presentation of Financial Statements" to be presented under other comprehensive income?

Which of the following combinations identify all items permitted in AASB 101 "Presentation of Financial Statements" to be presented under other comprehensive income?

(Multiple Choice)

4.9/5 (39)

Government departments are now required to report in accordance with AAS 29 'Financial reporting by government departments'. The broad effect of the requirements of this standard is to:

(Multiple Choice)

4.8/5 (37)

When selecting a presentation format management must select the one that is:

(Multiple Choice)

4.9/5 (36)

An implication of the fact that traditional financial accounting is based on a model that emphasises property rights is:

(Multiple Choice)

4.8/5 (38)

All adjustments to equity other than those related to transactions with owners in their capacity as owners are disclosed in the Statement of Comprehensive Income (AASB 101):

(True/False)

4.7/5 (35)

The notes to the accounts that relate to income and expense should include:

(Multiple Choice)

4.9/5 (36)

The income statement satisfies the requirements of the Corporations Act 2001 for a 'profit and loss statement':

(True/False)

4.8/5 (34)

If it is found that an error had been made in a prior period.

(Multiple Choice)

4.7/5 (32)

When there is a change made to the useful life of an asset:

(Multiple Choice)

4.8/5 (33)

In establishing the classification of items in the income statement, the size of an item is an appropriate basis for establishing a separate classification (by nature or function) for it:

(True/False)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)