Exam 12: Set-Off and Extinguishment of Debt

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, Plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory60 Questions

Exam 8: Accounting for Intangibles63 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease66 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes65 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures60 Questions

Exam 27: Earnings Per Share62 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues Ii: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues Iii: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions59 Questions

Exam 36: Translation of the Accounts of Foreign Operations42 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

In relation to applying an amount due from a third party in a "set-off" situation, AASB 132 notes:

(Multiple Choice)

4.7/5  (44)

(44)

Pump It Up Ltd owes Under Ground Oil $170 000 and Under Ground Oil owes Pump It Up Ltd $350 000. Pump It Up Ltd's financial position before these amounts are set-off is:

What is the debt/equity ratio for Pump It Up Ltd before and after set-off?

What is the debt/equity ratio for Pump It Up Ltd before and after set-off?

(Multiple Choice)

4.9/5 (38)

AASB 132 only allows assets and liabilities to be offset against one another if a legally recognised right to set-off exists for these items:

(True/False)

4.7/5 (39)

Insubstance debt defeasance was defined in the former AASB 1014 as:

(Multiple Choice)

5.0/5 (42)

A right of set-off may still be applied in the case of Insubstance Debt Defeasance (ISDD) if the entity intends to settle on a net basis, or to realise the asset and settle the liability simultaneously.

(True/False)

4.9/5 (43)

The term defeasance means the setting off of one thing against another:

(True/False)

4.9/5 (38)

Cartoons and Co's balance sheet is shown below.

Assuming a right to set-off exist with Ink Drawings Ltd, the balance sheet after set-off will be:

Assuming a right to set-off exist with Ink Drawings Ltd, the balance sheet after set-off will be:

(Multiple Choice)

4.8/5 (27)

One of the requirements for setting off in AASB 132 is the intention to offset. Which of the following statements about the "intention to set off" is correct?

(Multiple Choice)

4.8/5 (31)

A futures contract is an example of a financial instrument where the net amount of a financial asset and a financial liability may be presented in the statement of financial position.

(True/False)

4.8/5 (46)

The former AASB 1014 required that if a trust was established to assume the responsibility for a debt in an insubstance debt defeasance, that trust must:

(Multiple Choice)

4.8/5 (36)

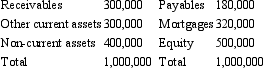

Claudia Ltd's statement of financial position is shown below.

The above balances include a receivable from Jeremy Ltd for an amount of $100,000 and a payable to Jeremy Ltd for $50,000. A debt contract with ABC Bank signed by Claudia Ltd requires a debt equity ratio of no more than 50%.

Assuming a right to set-off exists with Jeremy Ltd, what is the debt to equity ratio of Claudia Ltd?

The above balances include a receivable from Jeremy Ltd for an amount of $100,000 and a payable to Jeremy Ltd for $50,000. A debt contract with ABC Bank signed by Claudia Ltd requires a debt equity ratio of no more than 50%.

Assuming a right to set-off exists with Jeremy Ltd, what is the debt to equity ratio of Claudia Ltd?

(Multiple Choice)

4.9/5 (41)

Legal defeasance is not addressed in AASB 132 and will no longer be used in Australia.

(True/False)

4.8/5 (32)

Which of the following is not one of the advantages that were previously available when the insubstance defeasance of debt was allowable?

(Multiple Choice)

4.9/5 (37)

A debt cannot be considered extinguished, and therefore removed from the balance sheet, unless:

(Multiple Choice)

4.9/5 (39)

Release from the primary obligation for a debt may be achieved by replacement by another debt:

(True/False)

4.7/5 (36)

In a set-off, the gearing ratio of the entity is usually increased.

(True/False)

4.8/5 (39)

The "Offsetting" in AASB 132 "Financial Instruments: Presentation" is similar to "derecognition" in AASB 139.

(True/False)

4.9/5 (35)

Insubstance debt defeasance refers to an arrangement where assets are placed in trust, meaning that the creditor has now been paid in full:

(True/False)

4.8/5 (42)

Insubstance debt defeasance is no longer allowed under AASB 132:

(Multiple Choice)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)