Exam 13: Property Transactions: Section 1231 and Recapture

Exam 1: An Introduction to Taxation104 Questions

Exam 2: Determination of Tax138 Questions

Exam 3: Gross Income: Inclusions132 Questions

Exam 4: Gross Income: Exclusions107 Questions

Exam 5: Property Transactions: Capital Gains and Losses133 Questions

Exam 6: Deductions and Losses130 Questions

Exam 7: Itemized Deductions114 Questions

Exam 8: Losses and Bad Debts114 Questions

Exam 9: Employee Expenses and Deferred Compensation135 Questions

Exam 10: Depreciation, Cost Recovery, Amortization, and Depletion93 Questions

Exam 11: Accounting Periods and Methods107 Questions

Exam 12: Property Transactions: Nontaxable Exchanges115 Questions

Exam 13: Property Transactions: Section 1231 and Recapture100 Questions

Exam 14: Special Tax Computation Methods, Tax Credits, and Payment of Tax117 Questions

Exam 15: Tax Research127 Questions

Exam 16: Corporations137 Questions

Exam 17: Partnerships and S Corporations133 Questions

Exam 18: Taxes and Investment Planning81 Questions

Select questions type

An unincorporated business sold two warehouses during the current year. The straight-line depreciation method was used for Building No. 1 and the accelerated method (ACRS)was used for Building No. 2. Information about those buildings is presented below.

Accum. Depreciation

Accum. Depreciation

How much gain from these sales should be reported as section 1231 gain and ordinary income due to depreciation recapture?

How much gain from these sales should be reported as section 1231 gain and ordinary income due to depreciation recapture?

(Essay)

4.8/5  (37)

(37)

Installment sales of depreciable property which result in recaptured income under Secs. 1245 or 1250 require that the recaptured income be recognized in the year of sale.

(True/False)

4.7/5 (33)

All of the following are considered related parties for purposes of Sec. 1239 recapture with the exception of

(Multiple Choice)

4.9/5 (38)

Jesse installed solar panels in front of his office building in 2013. The panels are not attached to the building. After using the solar panels for 13 months, Jesse decided to replace them with a newer model to obtain a greater savings on electricity costs. Jesse sold the old solar panels for an amount greater than his original purchase price. What tax issues should be considered with purchase, use and sale of the original solar panels?

(Essay)

4.7/5 (32)

Section 1250 does not apply to assets sold or exchanged at a loss.

(True/False)

4.8/5 (31)

Cassie owns equipment ($45,000 basis and $30,000 FMV)and a building ($152,000 basis and $158,000 FMV), which are used in Cassie's business. Cassie has used straight-line depreciation for both assets, which were acquired two years ago. Both the equipment and the building are destroyed in a fire, and Cassie collects insurance proceeds equal to the assets' FMV. The tax result to Cassie for this transaction is a

(Multiple Choice)

4.8/5 (29)

Terry has sold equipment used in her business. She acquired the equipment three years ago for $50,000 and has recognized $30,000 of depreciation across the years in use. In order to recognize any Sec. 1231 gain, she must sell the equipment for more than

(Multiple Choice)

4.9/5 (39)

Sec. 1245 applies to gains on the sale of depreciable personal property, but it generally does not apply to depreciable real property.

(True/False)

4.9/5 (39)

Why did Congress establish favorable treatment for 1231 assets?

(Multiple Choice)

4.8/5 (42)

Sarah owned land with a FMV of $150,000 (adjusted basis $135,000)which is investment property (a capital asset). Sarah owned a second tract of land, a 1231 asset, with a FMV of $38,000 (adjusted basis $55,000). Both tracts were acquired in 2000 and condemned by the state this year. The state paid an amount equal to FMV. If there are no other transactions involving capital assets or 1231 assets, what is the amount that Sarah must report on her current year return?

(Essay)

4.8/5 (41)

When a donee disposes of appreciated gift property, the recapture amount for the donee is computed by including the recapture amount attributable to the donor.

(True/False)

4.9/5 (38)

Dinah owned land with a FMV of $130,000 (adjusted basis $120,000)which is investment property (a capital asset). Dinah owned a second tract of land, a 1231 asset, with a FMV of $46,000 (adjusted basis $50,000). Both tracts were acquired in 2001 and condemned by the state this year. The state paid an amount equal to FMV. If there are no other transactions involving capital assets or 1231 assets, Dinah must report on her current year return

(Multiple Choice)

4.8/5 (36)

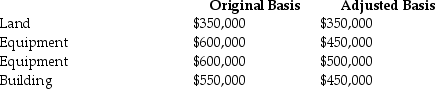

Describe the tax treatment for a noncorporate taxpayer in the 39.6% marginal tax bracket who sells each of the first two assets for $500,000 and each of the second two assets for $750,000. Each asset was purchased in 2010 and is used in a trade or business. There are no other gains and losses and no nonrecaptured Section 1231 losses.

(Essay)

4.8/5 (43)

Section 1231 property will generally have all the following characteristics except

(Multiple Choice)

4.8/5 (35)

The amount recaptured as ordinary income under either Sec. 1245 or Sec. 1250 can never exceed the realized gain.

(True/False)

4.9/5 (36)

In addition to the normal recapture rules of Sec. 1250, corporations which sell depreciable real estate are subject to additional recapture rules of Sec. 291.

(True/False)

4.9/5 (44)

Gifts of appreciated depreciable property may trigger recapture of depreciation or cost-recovery deductions to the donor.

(True/False)

4.9/5 (31)

Frisco Inc., a C corporation, placed a building in service in 2002 and deducted straight-line depreciation under the MACRS system in the normal manner. It sold the building this year for a substantial gain. Because straight-line depreciation was used, Frisco will not need to recognize any ordinary gain.

(True/False)

4.9/5 (28)

If no gain is recognized in a nontaxable like-kind exchange involving Sec. 1245 or Sec. 1250 property, the recapture potential carries over to the replacement property.

(True/False)

4.7/5 (48)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)