Exam 13: Property Transactions: Section 1231 and Recapture

Exam 1: An Introduction to Taxation104 Questions

Exam 2: Determination of Tax138 Questions

Exam 3: Gross Income: Inclusions132 Questions

Exam 4: Gross Income: Exclusions107 Questions

Exam 5: Property Transactions: Capital Gains and Losses133 Questions

Exam 6: Deductions and Losses130 Questions

Exam 7: Itemized Deductions114 Questions

Exam 8: Losses and Bad Debts114 Questions

Exam 9: Employee Expenses and Deferred Compensation135 Questions

Exam 10: Depreciation, Cost Recovery, Amortization, and Depletion93 Questions

Exam 11: Accounting Periods and Methods107 Questions

Exam 12: Property Transactions: Nontaxable Exchanges115 Questions

Exam 13: Property Transactions: Section 1231 and Recapture100 Questions

Exam 14: Special Tax Computation Methods, Tax Credits, and Payment of Tax117 Questions

Exam 15: Tax Research127 Questions

Exam 16: Corporations137 Questions

Exam 17: Partnerships and S Corporations133 Questions

Exam 18: Taxes and Investment Planning81 Questions

Select questions type

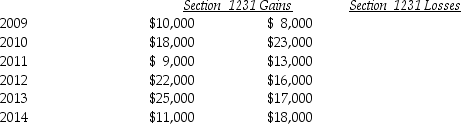

Lucy, a noncorporate taxpayer, experienced the following Section 1231 gains and losses during the years 2009 through 2014. Her first disposition of a Sec. 1231 asset occurred in 2009. Assuming Lucy had no capital gains and losses during that time period, what is the tax treatment in each of the years listed?

(Essay)

4.7/5  (38)

(38)

In 1980, Mr. Lyle purchased a factory building to use in business for $480,000. When Mr. Lyle sells the building for $580,000, he has taken depreciation of $470,000. Straight-line depreciation would have been $400,000. Mr. Lyle must report

(Multiple Choice)

4.8/5 (31)

For noncorporate taxpayers, depreciation recapture is not required on real property placed in service after 1986.

(True/False)

4.7/5 (31)

Emma owns a small building ($120,000 basis and $123,000 FMV)and equipment ($35,000 basis and $22,000 FMV). Both assets were acquired three years ago, are used in Emma's business, and are depreciated using straight-line depreciation. Both are destroyed by fire. Insurance proceeds were equal to their FMVs. Only one other transfer of an asset occurs during the year, and a $3,000 LTCL is recognized. After considering all transactions, the tax result to Emma is a

(Multiple Choice)

4.7/5 (33)

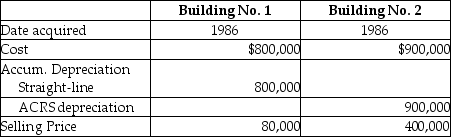

An unincorporated business sold two warehouses during the current year. The straight-line depreciation method was used for the first building and the accelerated method (ACRS)was used for the second building. Information about those buildings is presented below.  How much gain from these sales should be reported as section 1231 gain and ordinary income due to depreciation recapture by the owner of the business?

How much gain from these sales should be reported as section 1231 gain and ordinary income due to depreciation recapture by the owner of the business?

(Multiple Choice)

4.9/5 (36)

Costs of tangible personal business property which are expensed under Sec. 179 are subject to recapture if the property is converted to nonbusiness use before the end of the MACRS recovery period.

(True/False)

4.7/5 (38)

Jeremy has $18,000 of Section 1231 gains and $23,000 of Section 1231 losses. The gains and losses are characterized as

(Multiple Choice)

4.9/5 (28)

Sec. 1245 ordinary income recapture can apply to buildings placed in service prior to 1987.

(True/False)

4.9/5 (31)

During the current year, George recognizes a $30,000 Section 1231 gain on sale of land and a $18,000 Section 1231 loss on the sale of land. Prior to this, George's only Section 1231 item was a $14,000 loss six years ago. George must report a

(Multiple Choice)

5.0/5 (28)

With regard to noncorporate taxpayers, all of the following statements are true regarding Sec. 1250 recapture except

(Multiple Choice)

4.8/5 (39)

Harry owns equipment ($50,000 basis and $38,000 FMV)and a building ($140,000 basis and $156,000 FMV), which are used in his business. Harry uses straight-line depreciation for both assets, which were acquired several years ago. Both the equipment and the building are destroyed in a fire, and Harry collects insurance proceeds equal to the assets' FMV. The tax result to Harry for this transaction is

(Multiple Choice)

4.9/5 (30)

Octet Corporation placed a small storage building in service in 1999. Octet's original cost for the building is $800,000 and the cost recovery deductions are $300,000. This year the building is sold for $1,100,000. The amount and character of the gain are

(Multiple Choice)

4.8/5 (35)

The additional recapture under Sec. 291 is 25% of the difference between the amount that would have been recaptured if the property was Sec. 1245 property and the actual recapture under Sec. 1250.

(True/False)

4.7/5 (39)

Network Corporation purchased $200,000 of five-year equipment on March 24, 2012. They elected to expense $60,000 of the cost under Sec. 179 in effect that year. After depreciating the equipment $28,000 in 2012 and $22,400 in 2013, the equipment was sold for $190,000.

a. What is the amount of the realized gain (or loss)on the sale?

b. How is the gain or loss taxed?

(Essay)

4.8/5 (23)

Sec. 1231 property must satisfy a holding period of more than one year.

(True/False)

4.8/5 (30)

Emily, whose tax rate is 28%, owns an office building which she purchased for $900,000 on March 18 of last year. The building is sold for $950,000 on February 20 of this year when the adjusted basis of the building was $876,000. The tax results to Emily are

(Multiple Choice)

4.8/5 (33)

Jed sells an office building during the current year for $800,000. The building was purchased in 1980 for $350,000. Jed had depreciated the building under an accelerated method, but it is now fully depreciated. Jed has never had any other Sec. 1231 transactions.

a. What is the recognized gain or loss on the sale of the building and the character of the gain?

b. How will the gain be taxed?

(Essay)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)