Exam 13: Property Transactions: Section 1231 and Recapture

The following gains and losses pertain to Arnold's business assets that qualify as Sec. 1231 property. Arnold does not have any nonrecaptured net Sec. 1231 losses from previous years, and the portion of gain recaptured as ordinary income due to the depreciation recapture provisions has been eliminated.

Describe the specific tax treatment of each of these transactions.

Describe the specific tax treatment of each of these transactions.

The $25,000 casualty loss is an ordinary loss deductible for AGI since casualty losses exceed casualty gains. The condemnation loss is a Sec. 1231 loss of $20,000; the $16,000 gain is a Sec. 1231 gain. Because Sec. 1231 losses exceed Sec. 1231 gains, each is treated as ordinary resulting in a net $4,000 ordinary loss to be added to the $25,000 casualty ordinary loss for a total loss of $29,000.

Melissa acquired oil and gas properties for $600,000. During 2013 she elected to expense the $180,000 of IDC. Total depletion allowed was $50,000. During the current year, Melissa sells the property for $700,000.

a. What is the amount of and nature of her gain using the facts above?

b. What is the amount of and nature of her gain assuming that she sold the property for $850,000?

a. Melissa has realized gain of $150,000 [$700,000 selling price - $550,000 ($600,000 - $50,000)adjusted basis]. All of her gain is ordinary income due to the recapture of $180,000 IDC and $50,000 depletion.

b. Melissa has realized gain of $300,000 [$850,000 selling price - $550,000 ($600,000 - $50,000)adjusted basis]. Her gain is ordinary income to the extent of recapture of $230,000 ($180,000 IDC and $50,000 depletion). The remaining gain of $70,000 is 1231 gain.

If the recognized losses resulting from involuntary conversions arising from casualty or theft exceed the recognized gains from such events (i.e. a net loss from the casualty), all of the involuntary conversions are treated as ordinary gains and losses.

True

A corporation sold a warehouse during the current year. The straight-line depreciation method was used. Information about the building is presented below:  How much gain should the corporation report as section 1231 gain?

How much gain should the corporation report as section 1231 gain?

Pete sells equipment for $15,000 to Marcel, his son. The equipment cost $20,000 and has accumulated depreciation of $12,000. Marcel will use the equipment in his business.

a. What is the amount and character of Pete's gain on the sale?

b. How does your answer change if the sales price is $22,000?

Mark owns an unincorporated business and has $20,000 of Section 1231 gains and $22,000 of Section 1231 losses. He must report a capital loss of $2,000 on his tax return.

A net Sec. 1231 gain is treated as ordinary income to the extent of any nonrecaptured net Sec. 1231 losses for the preceding five years.

Indicate whether each of the following assets are capital assets, Sec. 1231 assets, or ordinary income property (property which, if sold, results in ordinary income). Assume that all of the property is held for more than one year.

a. XYZ Corporation owns land used as an employee parking lot. How is the parking lot classified for tax purposes?

b. Montana Corporation owns land held as an investment. How is the land classified for tax purposes?

c. John, a self-employed electrician, owns an automobile he uses strictly for personal use. How is the automobile classified for tax purposes?

d. Jan, a self-employed contractor, owns a truck she uses exclusively in her trade or business. How is the truck classified for tax purposes?

e. Leslie owns an office building where her accounting practice is located. What is the classification of the building?

f. Yvonne owns a computer for use in her job as a sales representative. She does not use the computer for personal purposes. How is the computer classified for tax purposes?

All of the following statements are true regarding Sec. 1245 are true except

Blair, whose tax rate is 28%, sells one tract of land at a gain of $29,000 and another tract of land at a gain of $11,000. Both tracts of land are Sec. 1231 property. She has never had any other Sec. 1231 transactions. How are the gains taxed?

Pam owns a building used in her trade or business that was placed into service in 2002. The building cost $450,000 and depreciation to date amounts to $200,000. Pam sells the building for $380,000. It is the only asset she sells this year, and she has no nonrecaptured Sec. 1231 losses. What is the amount of recognized gain and the nature of the gain? How will the gain be taxed?

Any gain or loss resulting from the sale or disposition of depreciable property used in trade or business and held one year or less is considered ordinary.

In order to be considered Sec. 1231 property, all of the following livestock must be held for 12 months or more from date of acquisition except

If a taxpayer has gains on Sec. 1231 assets, Secs. 1245 and 1250 must be applied first to determine any amounts recaptured as ordinary income, and any excess gain may then be netted with Sec. 1231 losses for possible long-term capital gain treatment.

Hilton, a single taxpayer in the 28% marginal tax bracket, has $16,000 of nonrecaptured net Sec. 1231 losses, at the beginning of a year in which he had the following transactions:

-Sale of Asset A at a $10,000 1231 gain, all of which is unrecaptured Sec. 1250 gain

-Sale of Asset B at a $13,000 1231 gain

How are the items reported this year and at which rate(s)are the amounts taxed?

Unrecaptured 1250 gain is the amount of long-term capital gain which would be taxed as ordinary income if Sec. 1250 provided for the recapture of all depreciation and not just additional depreciation.

Gains and losses from involuntary conversions of property used in a trade or business generally are classified as capital gains and losses.

The following are gains and losses recognized in 2014 on Ann's business assets that were held for more than one year. The assets qualify as Sec. 1231 property.

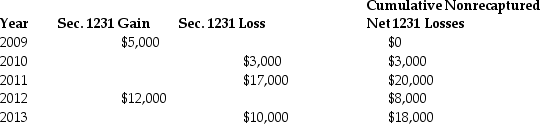

A summary of Ann's net Sec. 1231 gains and losses for the previous five-year period is as follows:

A summary of Ann's net Sec. 1231 gains and losses for the previous five-year period is as follows:

Describe the specific tax treatment of each of the current year transactions.

Describe the specific tax treatment of each of the current year transactions.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)