Exam 27: The Theory of Active Portfolio Management

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

The ____________ model allows the private views of the portfolio manager to be incorporated with market data in the optimization procedure.

(Multiple Choice)

4.7/5  (35)

(35)

If you begin with a ______ and obtain additional data from an experiment, you can form a ______.

(Multiple Choice)

4.9/5 (44)

To improve future analyst forecasts using the statistical properties of past forecasts, a regression model can be fitted to past forecasts.The intercept of the regression is a __________ coefficient, and the regression beta represents a __________ coefficient.

(Multiple Choice)

4.8/5 (31)

Consider the Treynor-Black model.The alpha of an active portfolio is 1%.The expected return on the market index is 16%.The variance of the return on the market portfolio is 4%.The nonsystematic variance of the active portfolio is 1%.The risk-free rate of return is 8%.The beta of the active portfolio is 1.05.The optimal proportion to invest in the active portfolio is

(Multiple Choice)

4.9/5 (33)

Even low-quality forecasts have proven to be valuable because R-squares of only ____________ in regressions of analysts' forecasts can be used to substantially improve portfolio performance.

(Multiple Choice)

4.8/5 (37)

The beta of an active portfolio is 1.45.The standard deviation of the returns on the market index is 22%.The nonsystematic variance of the active portfolio is 3%.The standard deviation of the returns on the active portfolio is

(Multiple Choice)

4.7/5 (33)

Consider the Treynor-Black model.The alpha of an active portfolio is 1%.The expected return on the market index is 11%.The variance of return on the market portfolio is 6%.The nonsystematic variance of the active portfolio is 2%.The risk-free rate of return is 4%.The beta of the active portfolio is 1.1.The optimal proportion to invest in the active portfolio is

(Multiple Choice)

4.9/5 (25)

Consider the Treynor-Black model.The alpha of an active portfolio is 3%.The expected return on the market index is 10%.The variance of the return on the market portfolio is 4%.The nonsystematic variance of the active portfolio is 2%.The risk-free rate of return is 3%.The beta of the active portfolio is 1.15.The optimal proportion to invest in the active portfolio is

(Multiple Choice)

4.9/5 (38)

Kane, Marcus, and Trippi (1999) show that the annualized fee that investors should be willing to pay for active management, over and above the fee charged by a passive index fund, does not depend on I) the investor's coefficient of risk aversion.

II. the value of the at-the-money call option on the market portfolio.

III. the value of the out-of-the-money call option on the market portfolio.

IV. the precision of the security analyst.

V. the distribution of the squared information ratio in the universe of securities.

(Multiple Choice)

5.0/5 (41)

____________ can be used to measure forecast quality and guide in the proper adjustment of forecasts.

(Multiple Choice)

4.8/5 (29)

The beta of an active portfolio is 1.36.The standard deviation of the returns on the market index is 22%.The nonsystematic variance of the active portfolio is 1.2%.The standard deviation of the returns on the active portfolio is

(Multiple Choice)

4.7/5 (36)

There appears to be a role for a theory of active portfolio management because

(Multiple Choice)

4.9/5 (40)

Which of the following are not true regarding the Treynor-Black model?

(Multiple Choice)

4.8/5 (31)

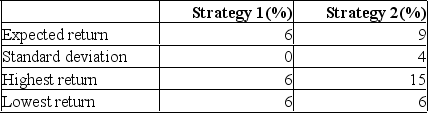

Consider these two investment strategies:  Strategy __________ is the dominant strategy because __________.

Strategy __________ is the dominant strategy because __________.

(Multiple Choice)

4.7/5 (31)

The beta of an active portfolio is 1.20.The standard deviation of the returns on the market index is 20%.The nonsystematic variance of the active portfolio is 1%.The standard deviation of the returns on the active portfolio is

(Multiple Choice)

4.9/5 (40)

Consider the Treynor-Black model.The alpha of an active portfolio is 3%.The expected return on the market index is 18%.The standard deviation of the return on the market portfolio is 25%.The nonsystematic standard deviation of the active portfolio is 15%.The risk-free rate of return is 6%.The beta of the active portfolio is 1.2.The optimal proportion to invest in the active portfolio is

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)