Exam 27: The Theory of Active Portfolio Management

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

Consider the Treynor-Black model.The alpha of an active portfolio is 2%.The expected return on the market index is 16%.The variance of return on the market portfolio is 4%.The nonsystematic variance of the active portfolio is 1%.The risk-free rate of return is 8%.The beta of the active portfolio is 1.The optimal proportion to invest in the active portfolio is

Free

(Multiple Choice)

5.0/5  (25)

(25)

Correct Answer: Verified

Verified

D

The Treynor-Black model requires estimates of

Free

(Multiple Choice)

4.9/5 (36)

Correct Answer:Verified

B

To determine the optimal risky portfolio in the Treynor-Black model, macroeconomic forecasts are used for the _________, and composite forecasts are used for the __________.

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

A

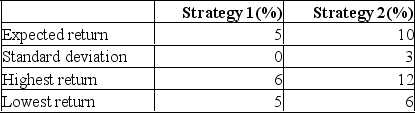

Consider these two investment strategies:  Strategy __________ is the dominant strategy because __________.

Strategy __________ is the dominant strategy because __________.

(Multiple Choice)

4.9/5 (29)

Consider the Treynor-Black model.The alpha of an active portfolio is 2%.The expected return on the market index is 12%.The variance of the return on the market portfolio is 4%.The nonsystematic variance of the active portfolio is 2%.The risk-free rate of return is 3%.The beta of the active portfolio is 1.15.The optimal proportion to invest in the active portfolio is

(Multiple Choice)

4.8/5 (34)

A manager who uses the mean-variance theory to construct an optimal portfolio will satisfy

(Multiple Choice)

4.9/5 (30)

According to the Treynor-Black model, the weight of a security in the active portfolio depends on the ratio of __________ to __________.

(Multiple Choice)

4.7/5 (37)

Kane, Marcus, and Trippi (1999) show that the annualized fee that investors should be willing to pay for active management, over and above the fee charged by a passive index fund, depends on I) the investor's coefficient of risk aversion.

II. the value of the at-the-money call option on the market portfolio.

III. the value of the out-of-the-money call option on the market portfolio.

IV. the precision of the security analyst.

V. the distribution of the squared information ratio in the universe of securities.

(Multiple Choice)

4.8/5 (34)

Ideally, clients would like to invest with the portfolio manager who has

(Multiple Choice)

4.8/5 (36)

The Black-Litterman model is geared toward ____________ while the Treynor-Black model is geared toward ____________.

(Multiple Choice)

4.7/5 (35)

The Treynor-Black model is a model that shows how an investment manager can use security analysis and statistics to construct

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)