Exam 23: Futures, Swaps, and Risk Management

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

Suppose that the risk-free rates in the United States and in the United Kingdom are 4% and 6%, respectively.The spot exchange rate between the dollar and the pound is $1.60/BP.What should the futures price of the pound for a one-year contract be to prevent arbitrage opportunities, ignoring transactions costs?

Free

(Multiple Choice)

5.0/5  (38)

(38)

Correct Answer: Verified

Verified

E

If you sold an S&P 500 Index futures contract at a price of 950 and closed your position when the index futures was 947, you incurred

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

D

Arbitrage proofs in futures market pricing relationships

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

B

Which one of the following stock index futures has a multiplier of 25 euros times the index?

(Multiple Choice)

4.7/5 (36)

Which one of the following stock index futures has a multiplier of $100 times the index value?

(Multiple Choice)

4.7/5 (30)

Hedging one commodity by using a futures contract on another commodity is called

(Multiple Choice)

4.9/5 (35)

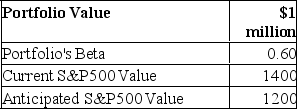

You are given the following information about a portfolio you are to manage.For the long term, you are bullish, but you think the market may fall over the next month.  What is the dollar value of your expected loss?

What is the dollar value of your expected loss?

(Multiple Choice)

4.9/5 (35)

Which one of the following stock index futures has a multiplier of $50 times the index value?

(Multiple Choice)

4.9/5 (33)

Suppose that the risk-free rates in the United States and in Canada are 3% and 5%, respectively.The spot exchange rate between the dollar and the Canadian dollar (C$) is $0.80/C$.What should the futures price of the C$ for a one-year contract be to prevent arbitrage opportunities, ignoring transactions costs.

(Multiple Choice)

4.7/5 (43)

Suppose that the risk-free rates in the United States and in the United Kingdom are 6% and 4%, respectively.The spot exchange rate between the dollar and the pound is $1.60/BP.What should the futures price of the pound for a one-year contract be to prevent arbitrage opportunities, ignoring transactions costs.

(Multiple Choice)

4.9/5 (42)

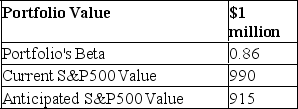

You are given the following information about a portfolio you are to manage.For the long term, you are bullish, but you think the market may fall over the next month.  What is the dollar value of your expected loss?

What is the dollar value of your expected loss?

(Multiple Choice)

4.8/5 (36)

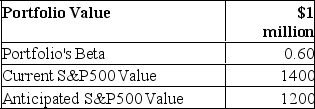

You are given the following information about a portfolio you are to manage.For the long term, you are bullish, but you think the market may fall over the next month.  For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

(Multiple Choice)

4.8/5 (35)

If you purchased one S&P 500 Index futures contract at a price of 1,550 and closed your position when the index futures was 1,547, you incurred

(Multiple Choice)

4.8/5 (39)

Which one of the following stock index futures has a multiplier of 50 Hong Kong dollars times the index?

(Multiple Choice)

4.9/5 (26)

In the equation Profits = a + b * ($/₤ exchange rate), b is a measure of

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)